A rent-to-buy scheme is a unique way to get onto the property ladder, almost like putting a house on lay-by. It lets you rent a home for a specific period with the exclusive option to buy it later, and the best part is it often helps you build a deposit through your regular rental payments.

How a Rent to Buy Scheme Really Works

For a lot of aspiring homeowners, the biggest hurdle is saving a deposit while juggling high rent. Rent-to-buy schemes are designed to bridge that exact gap, blending a normal rental agreement with a powerful option to purchase down the track.

Think of it as having two separate but connected agreements.

First, you sign a standard tenancy agreement, just like any other rental property. At the same time, you'll sign a second document called an option to purchase agreement. This is the game-changer: it gives you the exclusive right—but not the obligation—to buy the home at a pre-agreed price within a set timeframe, usually between three to five years.

The Two Core Components

The real magic of this setup is in its dual structure:

- Building a Deposit: A portion of your monthly rent, often called ‘rent credits’, is set aside by the seller. When you decide to buy, this accumulated amount is put towards your deposit.

- Locking in the Price: The option agreement fixes the purchase price today. If the property market in places like Mandurah goes up over the next few years, you still get to buy at the original, lower price, which can create instant equity for you.

A rent-to-buy scheme essentially lets you ‘try before you buy’. You get to live in the home, get a feel for the neighbourhood, and make sure it’s the right fit before you commit to the purchase.

Why These Schemes Are Gaining Traction

Let's be honest, affordability pressures across Australia are making it tougher than ever to buy a home. It's no surprise that alternative paths to homeownership are getting more attention. With the average Australian now needing about 10.6 years to save a home deposit, many people are looking for creative solutions. The rising cost of living and soaring rents make traditional saving methods a real challenge for many families. You can get a deeper look at the current housing situation in the 2025 State of the Housing System report.

The legal side of these agreements is critical for protecting everyone involved. To get your head around the foundational legal document used when you finally purchase a property, check out our detailed guide on what is a contract of sale. Understanding this document is vital before you jump into any property transaction.

Navigating the Rent to Buy Journey Step by Step

So, how does a rent-to-buy scheme actually work in practice? While it might sound a bit complicated at first glance, the process is quite structured. Let's break down the journey from browsing properties to finally getting the keys, showing you how it all comes together.

The first hurdle is actually finding a property offered on a rent-to-buy basis. You won’t see these splashed all over the major real estate websites, so you often need to connect with specialist providers or developers in Mandurah who facilitate these kinds of arrangements. It’s a two-part challenge: finding a home you love and a seller with fair terms.

Securing the Agreement

Once you’ve found the right place, it’s time to make it official. This isn’t just a single contract; you’ll be signing two separate but connected legal documents. First is a standard tenancy agreement for the rental phase. The second, and most important, is the option to purchase agreement. This is the key document that locks in your exclusive right to buy the property down the track.

It’s absolutely critical to get independent legal advice before you sign anything. A good solicitor will go through both contracts with a fine-tooth comb to protect your interests, check the terms are fair, and ensure there aren’t any hidden surprises that could jeopardise your option fee.

Your legal advisor will double-check all the crucial details, such as:

- The locked-in purchase price and how it was calculated.

- The length of the option period (usually 3-5 years).

- The exact amount of your non-refundable option fee.

- How much of your rent will be credited towards your deposit (your 'rent credits').

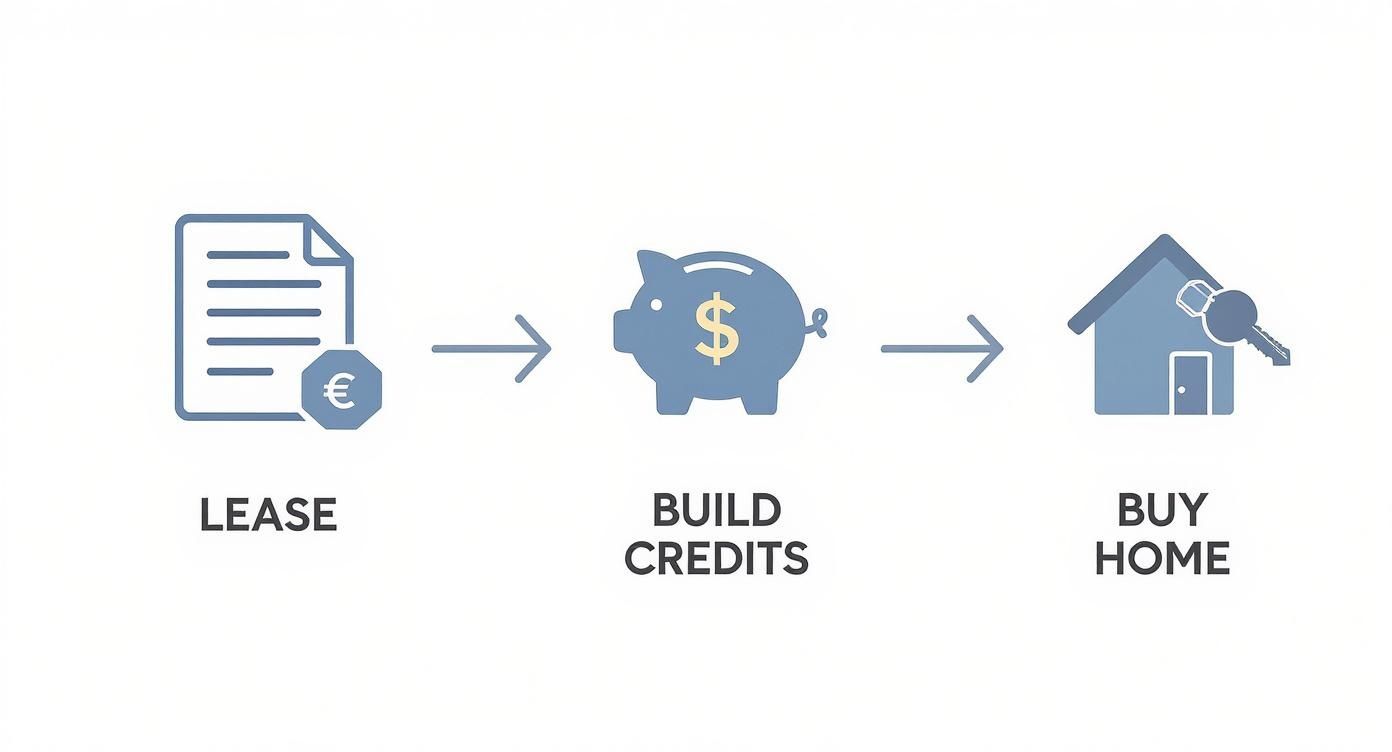

This infographic provides a great visual summary of the process, showing how you move from leasing, to building up your credits, and finally to owning the home.

As you can see, each stage builds on the last, turning your time as a renter into a clear pathway to homeownership.

To give you an even clearer picture, here’s a simple table outlining the main phases of the journey.

Phases of a Rent to Buy Scheme

This table breaks down what happens at each stage, what you need to do, and what the outcome is.

| Phase | Your Key Actions | Primary Outcome |

|---|---|---|

| 1. Agreement Phase | Find a property, get legal advice, sign the tenancy and option to purchase agreements, and pay the option fee. | Your right to purchase the property at a fixed price within a set timeframe is legally secured. |

| 2. Tenancy & Saving Phase | Live in the home, pay rent on time every month, maintain the property, and work on improving your credit score and savings. | You build up your rent credits, strengthen your financial profile, and prepare to qualify for a home loan. |

| 3. Purchase Phase | Notify the seller of your intent to buy, apply for and secure a mortgage, and complete the settlement process. | You use your option fee and rent credits as a deposit, finalise the purchase, and become the official homeowner. |

Think of it as a roadmap where each stop gets you closer to your final destination: owning your own home.

Living and Saving

During the tenancy period, your main jobs are simple but vital: pay your rent on time and look after the property as per your agreement. Each on-time payment not only keeps you in good standing but also adds to the deposit you’re steadily building. This is your golden opportunity to get your finances in top shape.

Use this time to actively clean up your credit history, pay down any other debts, and save extra cash for those final settlement costs. Your mission is to make yourself the perfect mortgage applicant when it’s time to buy.

Exercising Your Option to Buy

As you approach the end of your option period, it’s time for the final move. You'll need to formally tell the seller you want to buy and, most importantly, secure a home loan. The rent credits you've saved up, combined with your initial option fee, will form a substantial part of your deposit.

Getting that mortgage approval is the final piece of the puzzle. It’s a great idea to understand what lenders are looking for well ahead of time. Exploring the process of getting a home loan pre-approval early on can give you a massive head start. Once your finance is approved, the rest of the sale proceeds just like a standard property purchase, and you’ll officially become the homeowner.

Weighing the Real Pros and Cons

A rent-to-buy scheme can look like a golden ticket to homeownership, but it's a path you need to walk with your eyes wide open. It’s crucial to understand both the incredible opportunities and the serious potential pitfalls before you even think about signing on the dotted line.

This isn’t your standard rental agreement with a nice little bonus at the end; it's a serious financial strategy. While it's designed to help you leap over that massive deposit hurdle, it demands real diligence and a crystal-clear understanding of what you’re getting into.

The Clear Advantages of a Rent to Buy Scheme

One of the biggest wins here is locking in today’s purchase price. In a hot property market like Mandurah has been experiencing, this alone can be a massive financial advantage. You’re essentially shielding yourself from future price hikes while you get your savings in order.

On top of that, this setup cleverly turns your rent payments into a future asset. Instead of that money simply disappearing into your landlord's bank account each month, a slice of it is actively building towards your home deposit. It’s a kind of forced savings plan that can work wonders if you find it hard to put cash aside.

Here are a few other key upsides:

- Time to Improve Finances: The rental period, which is typically 3-5 years, gives you a set timeline to sort out your finances. It’s your chance to polish up your credit score, tackle any outstanding debts, and generally make yourself a more attractive applicant for a home loan.

- Try Before You Buy: This is a rare opportunity. You get to actually live in the house and the neighbourhood before you commit to buying it. It’s the ultimate test drive, helping you avoid any nasty surprises or buyer's remorse down the track.

- Security of Tenure: Unlike a typical 12-month lease, you get the stability of a long-term agreement. This provides a secure home for your family while you’re on the path to ownership.

Confronting the Potential Disadvantages

Now for the other side of the coin. The risks are very real and can hit you hard financially if things don't go according to plan. The most significant danger is losing your upfront option fee. We’re often talking thousands of dollars here, and it's non-refundable.

If you can't get a mortgage approved at the end of the agreement for any reason—maybe you lost your job, had a bad credit event, or the banks simply tightened their lending rules—you will almost certainly lose that entire fee and any rent credits you've built up.

It’s also important to know that the rent you pay in these schemes is almost always higher than the local market rate. This extra amount, or premium, covers the portion going towards your deposit and compensates the seller for the risk they're taking. You have to be comfortable paying this higher rate for the entire length of the agreement.

The market itself can also turn against you. If property values in Mandurah happen to drop below the price you’ve locked in, you could be legally stuck paying more for the home than it’s currently worth. That would put you in a negative equity situation from day one.

Rent to Buy Scheme Advantages vs Disadvantages

Thinking it through requires a direct, honest comparison. Here’s a simple table to help you lay out the two sides of the argument.

| Potential Advantages | Potential Disadvantages |

|---|---|

| Lock in a Purchase Price to beat market rises. | Loss of Option Fee if the purchase doesn't proceed. |

| Build a Deposit through your monthly rent payments. | Pay Higher Rent than the standard market rate. |

| Enjoy a 'Try Before You Buy' living experience. | Market Value Could Drop below your agreed price. |

| Secure a Fixed Timeframe to improve your credit history. | Strict Contract Terms can be unforgiving if breached. |

Ultimately, a rent-to-buy scheme is best for disciplined people who are confident they can become 'mortgage-ready' within the agreed timeframe. It's a calculated risk, no doubt, but one that can pay off big time if you do your homework and get solid legal advice before putting pen to paper.

Qualifying for Support and Government Programs

While a rent-to-buy agreement is ultimately a private arrangement between you and the property owner, it doesn’t exist in a vacuum. It's important to see it as part of a bigger picture that includes various government initiatives aimed at making housing more affordable. Understanding both what the private providers are looking for and what public support is available is the key to making this pathway work for you.

Think of rent-to-buy providers as vetting you for your future potential as a homeowner. They’re not just looking for a tenant; they’re looking for someone who has a genuine and credible plan to one day own the property.

What Providers Look For

This isn't just about proving you can pay rent on time. It's about showing you're on track to become a successful mortgage applicant down the line.

- Consistent Income: You’ll need to demonstrate a stable income that can comfortably cover the (often slightly higher) rent payments and your other living expenses without financial stress.

- A Clear Path to a Mortgage: Providers want to see you have a realistic strategy. This means you’re actively working on improving your credit score and have a plan for saving the funds needed to secure a home loan when the time comes.

- Ability to Pay an Option Fee: This upfront, non-refundable payment shows you have some savings behind you and are serious about the commitment. It typically ranges from 2% to 5% of the agreed-upon purchase price.

These criteria are there for a good reason—they help ensure the scheme is a genuine stepping stone to ownership, not just a long-term rental arrangement built on false hope.

Connecting to Government Housing Initiatives

Beyond these private schemes, it's worth noting that the Australian Government is rolling out programs that can either supplement or provide an alternative to a traditional rent-to-buy agreement. These initiatives are a direct response to the immense pressure facing both renters and aspiring buyers.

The key thing to remember is that government support and private rent-to-buy schemes are chasing the same goal: to bridge the gap between renting and owning for people who feel locked out of the traditional property market.

For instance, the government has significantly increased its focus on making homeownership more accessible. The 2025–26 Budget set aside roughly $800 million for the Help to Buy program, a shared equity scheme designed to assist around 40,000 households. An initiative like this can be a game-changer, reducing the deposit you need and the size of your mortgage by offering an equity contribution of up to 40%.

At the same time, measures like increasing Commonwealth Rent Assistance are designed to ease the weekly rental burden, which in turn can make it easier for you to save. You can dig into the details of these government housing initiatives on the official budget website.

These programs create a really supportive ecosystem. While a rent-to-buy scheme helps you build your deposit through your rental payments, a government program like Help to Buy could be that final piece of the puzzle you need to get your mortgage approved and complete the purchase. By looking into both avenues, you open up more potential pathways to finally owning your own home right here in Mandurah.

How Market Trends Impact Your Agreement

A rent-to-buy scheme doesn't exist in a vacuum; it's directly plugged into the ebbs and flows of the wider property market. Getting your head around these economic forces is absolutely critical because they can either turbocharge your agreement into a brilliant financial win or expose you to some serious risk. Honestly, timing and market awareness are just as important as the fine print in the contract itself.

Let's play this out. Imagine you lock in a purchase price of $500,000 today. If, over the next three years, the Mandurah market absolutely booms and the home's value shoots up to $570,000, your agreement is a massive success. You get to buy at the original, lower price, which means you walk into $70,000 of instant equity the moment you settle. This is the dream scenario every person entering a rent-to-buy scheme is hoping for.

The Risk of a Falling Market

But, and this is a big but, the market can swing the other way. This is where the main risk of these agreements lies.

If property values drop and that same $500,000 home is only worth $460,000 when your option to buy comes up, you're stuck between a rock and a hard place. You’re either contractually obliged to pay the higher, pre-agreed price, or you have to walk away, kissing your option fee and all those accumulated rent credits goodbye.

A falling market can put you in a position of negative equity from day one, where your mortgage would be bigger than the home's actual market value. This is a crucial risk to weigh up before signing anything.

This is exactly why staying informed about what's happening locally is so important. Keeping an eye on expert analysis, like the latest Perth property market forecast, helps you make a more calculated decision based on current trends and what the experts are predicting. It’s all about assessing whether the odds are stacked in your favour.

Rental Trends and Scheme Eligibility

It’s not just about sale prices, either. Broader economic trends also affect how many of these schemes are even available. As rental prices keep climbing, the idea of turning that 'dead money' into a future home deposit becomes more and more appealing for aspiring buyers. This pressure has actually pushed both government and private companies to get more creative with pathways to homeownership.

Recent market analysis shows a huge jump in eligibility for these kinds of alternative ownership models across Australia. For example, a whopping 93.7% of unit markets now fall under the price caps for programs like the Help to Buy scheme. When you combine that with steady rental growth, you can see why rent-to-buy and shared equity models are becoming more common, offering a genuine leg-up for people struggling with affordability.

Got Questions About Rent to Buy? We've Got Answers

Stepping into a rent to buy scheme is a big move, and it naturally brings up a lot of "what if" scenarios. This path to owning a home has its own set of rules and risks, so it's smart to tackle the big questions head-on.

Let's clear the air with some straightforward answers to the most common queries we hear from aspiring homeowners right here in Mandurah. Getting these details sorted from the start gives you the clarity you need to decide if this is the right strategy for you.

What Happens If I Can't Get a Home Loan at the End?

This is, without a doubt, the single biggest risk you need to be aware of. If your option period runs out and you can't get a mortgage approved, you'll almost certainly lose your entire upfront option fee and any extra rent credits you've paid.

That money stays with the seller, the agreement is terminated, and you'll have to move out. This is exactly why the rental period is so critical – you have to use that time to actively improve your credit score and build up your savings. Chatting with a mortgage broker right at the beginning is a non-negotiable step to make sure your homeownership goal is actually realistic.

Who's on the Hook for Repairs and Maintenance?

This can vary, so you need it spelled out crystal clear in your contract. In a lot of agreements, the tenant-buyer (that's you) will handle the minor day-to-day repairs and general upkeep, pretty much like a homeowner would. The seller might stay responsible for major structural problems, like issues with the roof or foundations.

Be careful, though. Some less-than-ideal contracts might try to push all repair responsibilities onto you. Before you sign anything, get a solicitor to go over this clause with a fine-tooth comb. You need to know exactly what you'll be financially liable for.

"A well-drafted contract is your best protection. It should leave no ambiguity around financial responsibilities for maintenance, clearly defining what falls to the tenant-buyer and what remains with the seller."

Understanding these obligations is crucial for budgeting properly throughout your tenancy.

Can the Seller Just Back Out of the Deal?

Nope, not if you have a legally solid 'option to purchase' and you've held up your end of the bargain. The 'option' is your exclusive right to buy, not theirs. As long as you've paid your rent on time and looked after the place as agreed, the seller is contractually locked in to sell you the home at the agreed-upon price.

They can't simply change their mind or sell it to someone else for a higher price. The catch is, if you break the terms of your lease, you could lose your option. That would free the seller from their obligation, which just goes to show how important it is to stick to the agreement.

Is This the Same as a Shared Equity Scheme?

Good question, but no – they are two completely different ways to get into a home.

- Rent to Buy: You're a tenant first, with the future right to buy 100% of the property. You don't actually own any part of the home during the rental phase.

- Shared Equity: You are a homeowner from day one. You take out a mortgage for your share (say, 60%), while another party (like the government in some schemes) owns the rest.

With shared equity, you're building equity straight away but you also share any future capital growth. In a rent to buy arrangement, you're working towards owning the whole thing yourself, down the track.

Navigating the Mandurah property market requires local expertise and a clear strategy. If you're considering buying or selling, David Beshay Real Estate can provide the personalised guidance you need to make informed decisions and achieve your property goals. Get your free property appraisal today!