At its core, the difference is simple: building a home gives you ultimate customisation and a brand-new final product. On the other hand, buying an existing home offers speed and convenience, placing you in an established neighbourhood much faster. Your choice really boils down to whether you prioritise a perfectly personalised design or a quicker move-in day.

The Great Australian Dream at a Modern Crossroads

Choosing whether to build a new home or buy an established one is easily one of the biggest financial and emotional decisions you’ll ever face. It’s the classic Aussie dream, but seen through the lens of today's complex property market where things like cost, time, and your own personal effort carry serious weight. This isn't just about picking a floor plan; it's about making sure your property journey aligns with your life right now, and where you see yourself in the future.

This guide is here to dig deeper than a simple pros and cons list. We'll break down the real trade-offs you'll be making in the "build vs buy" debate to help you navigate this major choice with confidence. First, let's start with a high-level look at how they stack up.

Building vs Buying at a Glance

This table gives you a quick snapshot of the fundamental differences between creating a home from the ground up and purchasing one that's already standing.

| Factor | Building a Home | Buying an Existing Home |

|---|---|---|

| Customisation | You have complete control over the layout, design, and every finish. It's tailored to your exact lifestyle. | What you see is what you get. Changes mean renovating, which adds more time and money after you've bought. |

| Timeline | A much longer process. Expect it to take 12-24 months from buying land to getting the keys, with delays always possible. | Significantly faster. You can be in your new home within 2-6 months from starting your search to settlement. |

| Initial Condition | Brand new. Comes with modern features, better energy efficiency, and a builder's warranty. No surprise repairs. | Can be anything from move-in ready to needing immediate work. Older systems might need urgent and costly upgrades. |

| Location | Usually limited to new estates on the fringes of established areas like Mandurah. | Far greater choice of established neighbourhoods with mature trees, existing amenities, and sought-after school zones. |

Think of this as your starting point. Each path has its clear benefits, but also its own set of challenges you'll need to be prepared for.

Before you can decide whether to build a new home or buy an existing one, you’ve got to get a handle on the market you’re walking into. Right now, the Australian property landscape is under some serious pressure, and it all comes down to a major housing supply crisis. This isn't just a catchy headline; it's the core market force shaping everything from the cost of an established home to the availability of a block of land.

This imbalance has created a fiercely competitive environment for everyone. If you’re looking to buy, you’ll find more people fighting for the same limited properties, which naturally pushes prices up and forces you to make decisions faster. If you’re dreaming of building, you’ll be up against stiff competition for residential lots, which are getting harder to find and more expensive, especially in sought-after spots.

The Supply and Demand Squeeze

At its heart, the issue is a simple numbers game: our population is growing much faster than we're building new homes. This gap between the number of people needing a roof over their head and the actual number of dwellings available is what’s driving the market’s current behaviour.

The stats really paint a stark picture of this national challenge. In the financial year ending 2025, Australia's population shot up by an estimated 436,300 people. In that same period, we only managed to build 173,800 new homes. That leaves a staggering shortfall of 262,500 dwellings in just one year, putting immense strain on the whole system. You can dig into more of this data on Australia’s housing supply on the IPA website.

Key Takeaway: This isn't just a fleeting trend. The ongoing supply shortage means that whether you build or buy, you'll face unique pressures tied to scarcity and competition. A well-thought-out strategy has never been more important.

Understanding this backdrop is crucial because it ripples through the entire property ecosystem. When demand completely outstrips supply, a few knock-on effects become obvious, and they directly influence whether building or buying makes more sense for you.

How This Affects Your Decision

This housing crisis doesn't hit both options in the same way. It throws up different challenges and advantages for each path, which you'll need to weigh against your own situation, budget, and timeline.

Here’s a look at the direct consequences:

- For Buyers: The biggest headache is competition. A well-priced home in a good area will almost certainly get multiple offers, sparking bidding wars and a fast-paced, often stressful, buying process. You might find you have to compromise on your wish list just to get your foot in the door.

- For Builders: The main hurdles are the cost and availability of land and materials. The price of residential lots has soared, and supply chain headaches can still cause delays and drive up construction costs. On top of that, finding a good, reliable builder who actually has availability can be a real challenge in itself.

Ultimately, the current market just magnifies the classic trade-offs of building versus buying. The convenience of an established home is now tempered by intense competition. And the dream of a custom new build is offset by rising costs and the real possibility of delays. Your decision will really come down to which set of challenges you feel better equipped to take on.

A Detailed Financial Analysis of Building vs Buying

When it comes down to it, the choice between building a new home and buying an existing one is almost always driven by the numbers. But it’s never as simple as comparing the price tag of an established home to a builder’s quote. The real cost is a tangled mix of upfront expenses, sneaky hidden fees, and financial commitments that stretch out over the long term.

Getting a handle on these numbers is the only way to figure out which path truly fits your budget and avoids a massive financial headache later on.

Let's move past the obvious prices and dig into the full financial picture of each option. By comparing every potential cost, from buying the land to post-move-in renovations, you can make a decision you're actually confident in.

The Upfront Costs of Buying an Existing Home

When you're looking at established homes, the purchase price is just the starting line. A bunch of other significant costs pop up that can quickly inflate your initial outlay if you're not ready for them.

While these costs are mostly predictable, they still manage to catch plenty of buyers by surprise. The main ones you need to budget for are:

- Stamp Duty: A hefty government tax calculated on the property's total value.

- Inspection Fees: Absolutely essential for building and pest inspections to see what problems might be lurking.

- Legal and Conveyancing Fees: The costs for a professional to handle the legal transfer of ownership.

- Lender's Mortgage Insurance (LMI): You'll likely need to pay this if your deposit is less than 20% of the purchase price.

It’s also easy to forget about the money needed for immediate updates or renovations to make the place feel like yours. These are just some of the 10 hidden costs of buying a house that can throw a spanner in your financial plans.

The Layered Expenses of Building a New Home

Building from scratch is a whole different ball game financially. Instead of one big transaction, you’re managing a project with multiple stages, each with its own set of bills and the very real potential to go over budget.

Right from the get-go, the financial hurdles are different. They include:

- Land Purchase: Your first major investment is just securing a block to build on.

- Site Preparation Costs: This covers everything from soil tests and clearing the block to excavation and levelling – costs that can vary dramatically.

- Design and Approval Fees: You'll need to pay for architectural plans and council permits before any dirt is even moved.

- Construction Loan Interest: You pay interest on the money you draw down during the build, a cost that climbs as the project moves forward.

One part of a build budget that is absolutely non-negotiable is a contingency fund. You need to set aside 10-20% of the total construction cost. This is your safety net for when material prices jump up or unexpected site issues pop up.

A Side-by-Side Financial Breakdown

To really get your head around the financial differences, nothing beats a direct comparison. The table below lays out the typical costs for both building and buying, giving you a clearer idea of where your money is actually going.

Financial Breakdown: Building a New Home vs Buying an Existing One

| Cost Component | Building a Home (Example) | Buying an Existing Home (Example) |

|---|---|---|

| Primary Cost | Land Purchase & Construction Contract | Property Purchase Price |

| Government Fees | Stamp Duty on Land Only | Stamp Duty on Full Property Value |

| Initial Set-Up | Site works, design fees, permits | Building & pest inspection fees |

| Financing Costs | Construction loan interest, fees | Standard home loan fees, LMI |

| Contingency | Essential (10-20% of build cost) | Optional (for immediate repairs) |

| Post-Handover | Landscaping, driveways, fencing | Renovation & furnishing budget |

As you can see, one of the biggest financial game-changers is stamp duty. When you build, you generally only pay stamp duty on the value of the land. This can lead to massive savings compared to paying it on the full price of an established home.

On top of that, government incentives like the First Home Owner Grant often lean towards new builds, which could give you another financial leg-up. It's crucial to factor these details into your sums before making a final call.

Comparing Timelines from Dream to Doorstep

Beyond the dollars and cents, your most precious asset is time. The path from imagining your new home to finally holding the keys looks wildly different depending on whether you build or buy. For many, this timeline is the make-or-break factor.

Opting for an existing home is, without a doubt, the faster route. It’s a well-trodden path with clear steps, making it perfect if you're on a deadline, like a job relocation or an expiring lease. From your first online search to settlement day, you're typically looking at a timeframe of two to six months.

This tighter schedule is a massive plus for anyone who values speed and certainty over a fully customised build.

The Quicker Path: Buying an Established Home

The buying process is built for efficiency. While it can feel like a whirlwind, each stage moves you closer to the finish line—think of it as a sprint, not a marathon.

Here’s a rough breakdown of what that journey looks like:

- Property Search (1-3 months): This is the most flexible part. How long it takes really depends on the market and how specific your wish list is.

- Making an Offer and Negotiation (1-2 weeks): Found 'the one'? Things tend to move very quickly from here.

- Inspections and Finance Approval (2-4 weeks): Once your offer is accepted, it's time for building and pest inspections while your lender gives your loan the final tick of approval.

- Settlement (4-8 weeks): This is the final legal step where ownership is officially transferred. It’s the last major hurdle before you can pop the champagne and move in. You can learn more about how long settlement takes in our detailed guide.

The Marathon: Building Your Dream Home

Building a home, on the other hand, is a long-haul project demanding a serious amount of patience and oversight. The timeline is not only longer but also far more vulnerable to delays that are completely out of your hands. From buying the land to the final handover, a realistic timeframe is anywhere from 12 to 24 months.

And that clock starts ticking long before a single shovel hits the dirt. The pre-construction phase alone can eat up several months as you jump through a series of complex hoops.

These initial steps usually involve:

- Land Acquisition: First, you have to find and purchase the right block of land.

- Design Process: Then comes the creative part, working with an architect or builder to get your floor plans just right.

- Council Approvals: Finally, your plans are submitted to the local council for building permits, a notoriously lengthy and bureaucratic process.

Once construction finally kicks off, you're still not in the clear. You’re at the mercy of things like bad weather, which can pause work for days, and supply chain issues, which can hold up essential materials.

"The hidden effort in building isn't just the time on a calendar; it's the mental load. You're making hundreds of decisions, from tapware to tile grout, over many months. With buying, the 'hidden effort' is often more physical—like stripping old wallpaper or ripping up carpets to make it your own after you move in."

At the end of the day, your choice comes down to your personal situation. If you need a roof over your head soon and prefer a predictable process, buying is the clear winner. But if you have the time and patience to see a major project through, the reward of a home built just for you might be worth every moment of the wait.

Customisation vs Convenience: Which Fits Your Lifestyle?

The whole debate between building a new home versus buying an existing one really comes down to one big question: are you after complete customisation, or is immediate convenience more your style? This decision goes way beyond just the look of the place; it dictates your day-to-day life, shapes your budget, and determines how much personal effort you're going to need to put in. Figuring out which side of that fence you sit on is the key to a choice you’ll be happy with for years.

For some people, the idea of creating a home that’s a perfect reflection of their family is a dream come true. For others, the thought of making endless decisions is a total nightmare, and the appeal of moving straight into an established community is much stronger. Let's walk through what these two different paths actually look like.

The Path of Total Control: Building Your Vision

When you decide to build, you're essentially choosing to be the author of your own living space. Every single detail, from how the house sits on the block to catch the morning sun to the exact style of tapware in the ensuite, is a decision you get to make. This is the main reason people head down the construction path.

Think of a growing family with young kids. Their top priority might be a big, open-plan living area where they can cook dinner while keeping an eye on the little ones. They could design a dedicated mudroom for school bags and footy boots, add extra storage in the garage, and create a floor plan that puts the parents' retreat well away from the noisy kids' bedrooms. Building allows them to design specific solutions for their everyday problems.

Building a home means you aren't just buying a property; you're crafting a solution. Every power point, window, and wall is placed to serve your unique lifestyle, creating a level of functionality that's almost impossible to find off-the-shelf.

But all that freedom comes with a price—your time and mental energy. The sheer number of choices can lead to decision fatigue. It's a real thing, where the constant need to pick and choose becomes genuinely stressful and exhausting.

The Drawbacks of Unlimited Choice

While customisation is the biggest drawcard, it also brings some serious challenges you need to be ready for:

- Project Management: You effectively become the project manager. This means coordinating with builders, architects, and suppliers, a role that needs constant communication and a sharp eye for detail.

- Budget Creep: Every "small upgrade" adds up. The temptation to go for the higher-end finishes can easily blow your budget out of the water, so you need serious discipline.

- Abstract to Reality: It's tough to truly visualise a finished home from 2D floor plans. What looks perfect on paper might not feel right once you're standing in it, and by then, changes are either ridiculously expensive or simply not possible.

This path is best for those who have a crystal-clear vision and the patience to see a long-term project through. It requires a hands-on approach and the resilience to handle the inevitable bumps in the road that come with any construction job.

The Path of Immediate Gratification: Buying a Home

On the flip side, buying an existing home offers the massive advantage of convenience. The property is real and tangible—you can walk through the rooms, get a feel for the space, and see exactly what you’re getting before you sign on the dotted line. This certainty removes a lot of the stress and guesswork that comes with building.

Take a professional couple who've just landed new jobs in Mandurah and need to move quickly. Their priority is a smooth, fast transition. They can view a dozen homes over a single weekend, pick one in a suburb close to work with established cafes and parks, and potentially move in within a couple of months. For them, time is everything, making an established home the only sensible option.

This convenience, however, almost always means making compromises. The layout might not be perfect, the kitchen could be a bit dated, or the overall style might not be to your taste. You're inheriting a property with a history, which can include both lovely character features and hidden issues like old plumbing or poor insulation. While you can always renovate, that adds another layer of cost and hassle after you've already bought the place, and some fundamental things, like a bad floor plan, can be very difficult and costly to fix.

Ultimately, the choice between customisation and convenience is a deeply personal one. You have to take a good, honest look at your priorities, your tolerance for stress, your financial situation, and—most importantly—where you are in life right now.

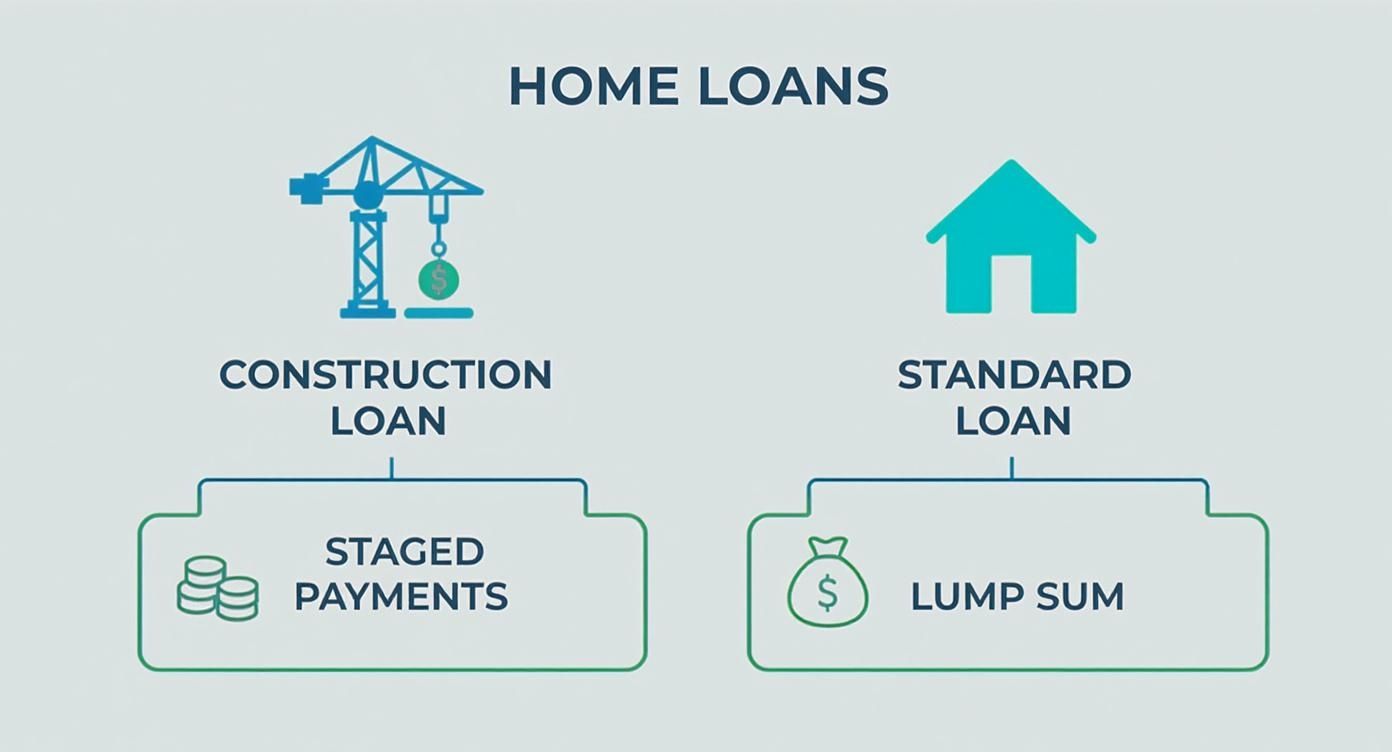

How to Secure Financing for Your Property

Let's be clear: the path to getting your finance approved looks completely different when you’re building a new home versus buying an established one. Financing an existing house is pretty straightforward, but a new build requires a special kind of loan called a construction loan. Getting your head around this is the first, most important step before you even think about talking to a broker.

With a standard home loan, the lender hands over a lump sum at settlement, and you start making repayments. Simple. A construction loan, on the other hand, is paid out in stages. Your lender releases funds directly to your builder as they hit specific milestones—think slab down, roof on, and so on.

Navigating Loan Requirements

It’s no surprise lenders look at these two loan types differently; the risk for them isn't the same. When you apply for a regular mortgage, the bank is lending against a solid, existing house. With a construction loan, they’re financing a property that is, for now, just a set of plans on paper, which means they’re going to be a lot more thorough.

You'll find the paperwork and deposit requirements vary quite a bit:

- For Buying: Lenders are mostly interested in your income, your credit history, and the property's valuation. A 20% deposit is the magic number to avoid paying Lender's Mortgage Insurance (LMI).

- For Building: You'll need to hand over a fixed-price building contract, council-approved plans, and all the specs. Lenders will also put your builder's reputation and finances under the microscope. Your deposit is usually calculated on the combined value of the land and the proposed build.

One thing lenders absolutely will not budge on for a construction loan is a solid contingency fund. You need to prove you have an extra 10-20% of the total build cost set aside for unexpected surprises. In this market, it’s a non-negotiable that shows you can see the project through to the end, even if costs blow out.

Preparing for Lender Scrutiny

Right now, lenders are being extra cautious. They’ll comb through your fixed-price building contract to make sure it’s airtight, with very little room for price hikes. A meticulously prepared application is your best friend here.

Taking the time to understand the mortgage process gives you a real advantage. Getting home loan pre-approval is a brilliant first move because it tells you exactly what you can borrow before you start falling in love with properties or blocks of land. It gives you the clarity to know what you can genuinely afford, whether you build or buy.

Ultimately, a sharp application, a healthy deposit, and that all-important contingency fund will give any lender the confidence they need to say yes, no matter which path you take.

Making the Right Choice for Your Situation

So, build or buy? Honestly, there’s no single "right" answer. The best path for you comes down to what you value most—your priorities, your finances, and where you are in life. It's a classic tug-of-war between the creative freedom of a blank slate and the move-in-ready convenience of an established home.

By now, you've seen the trade-offs. If having total control over the design, layout, and finishes is your dream, and you're keen on the latest energy-efficient features, building is probably your best bet. This path is perfect for those who have a specific vision and aren't in a mad rush to move.

On the other hand, if you need a place to live sooner rather than later, love the charm of an established neighbourhood, and don't mind the idea of a few renovations down the track, then buying an existing home makes a lot more sense. This is the go-to option for anyone who puts speed, location, and the certainty of a finished product first.

Visualising Your Path Forward

A huge piece of the puzzle is figuring out the money side of things. Construction loans and standard home loans are two very different beasts. The decision tree below gives you a clear picture of how the financing works depending on whether you choose to build or buy.

As you can see, a construction loan pays out in stages as your build hits key milestones. A standard mortgage, however, is a straightforward lump-sum payment when the property officially becomes yours at settlement.

Making a Confident Decision

At the end of the day, the right choice is the one that fits your life. There's no universally better option—just the one that works for your family, your budget, and your long-term plans.

Final Takeaway: Don't let the market rush you. Take the time to honestly assess your financial readiness, timeline flexibility, and tolerance for stress. The right decision is the one that brings you peace of mind, not just a set of keys.

Whether you're dreaming of a custom-designed sanctuary or hunting for a move-in-ready home in a community you already love, the perfect property is out there. Trust your gut, do your homework, and choose the path that feels right for you.

Navigating the Mandurah property market requires local expertise and a clear strategy. If you're ready to take the next step, whether building or buying, David Beshay Real Estate can provide the expert guidance and market insights you need. Start your property journey today.