Getting a home loan pre-approval is the critical first move that takes you from a casual window shopper to a serious property contender. Think of it as a conditional thumbs-up from a lender, telling you exactly how much they’re prepared to lend. This gives you a clear budget and serious negotiating power before you even set foot in an open home. In a competitive market, this is your strategic advantage.

Why Pre-Approval Is Your Secret Weapon in Property Hunting

Jumping into the property market without a pre-approval is like going grocery shopping without a list or a wallet—you’ll probably waste a lot of time and end up frustrated. Securing this conditional green light from a lender is the smartest thing you can do. It instantly elevates your status in the eyes of real estate agents and sellers.

Instead of guessing what you can afford, a pre-approval gives you a firm, realistic budget. This laser focus saves you the heartache of falling for a home that's just out of reach and makes sure every property you inspect is a genuine possibility.

Building Credibility and Confidence

Having your financing conditionally sorted gives you a massive confidence boost. You can walk into an auction or make an offer knowing your exact limit, which gets rid of the stressful guesswork that trips up so many unprepared buyers. Agents take pre-approved buyers far more seriously because it proves you’ve done your homework and are ready to go.

Here's a real-world scenario for you: a young couple in Mandurah went to an auction with their pre-approval letter in hand. When the bidding got intense, they could confidently place their final offer because they knew their financing was sorted. Another bidder, still waiting to hear from their bank, had to pull out and lost their dream home. The difference wasn't about who wanted it more; it was about who was better prepared.

A pre-approval isn't just a piece of paper; it’s a statement that you are a serious, qualified buyer ready to make a move. It completely shifts the power dynamic in your favour during negotiations.

This proactive approach is definitely catching on. The home loan pre-approval process in Australia has seen a big jump in popularity. In fact, data from one of the major banks showed that conditional pre-approval applications shot up by 12% in the first eight months of the year. This trend shows that more and more buyers are realising the clarity and confidence it brings to their property search. You can read more about these home loan trends on CommBank's newsroom.

Pre Approval vs Full Approval at a Glance

It's easy to get confused between a pre-approval and the final, unconditional loan approval. While they're both key steps, they serve very different purposes. Here's a quick breakdown to clear things up.

| Feature | Conditional Pre Approval | Full (Unconditional) Approval |

|---|---|---|

| Purpose | To estimate your borrowing capacity and show you're a serious buyer. | The final, binding confirmation of your loan for a specific property. |

| Timing | Before you start seriously house hunting or make an offer. | After you've made an offer and the bank has valued the property. |

| Commitment | A conditional offer from the lender, not a guarantee. | A legally binding commitment from the lender to provide the funds. |

| Property Specific? | No, it's based on your financial situation only. | Yes, it's tied to a specific property that meets the lender's criteria. |

| Key Benefit | Gives you confidence, a clear budget, and negotiating power. | Allows the property sale to proceed to settlement. |

Essentially, the pre-approval gets you in the game, but the full approval is what lets you cross the finish line.

The Clear Advantages of Being Prepared

The benefits of getting pre-approved are real and they kick in straight away. You’re not just getting a number; you're gaining a powerful strategic edge.

- Set a Realistic Budget: You'll know exactly how much you can spend, which lets you filter your property search and avoid wasting time.

- Boost Negotiating Power: Sellers and agents see your offers as far more credible. They're often more willing to negotiate with someone who is ready to buy.

- Speed Up the Process: With most of your financial checks already done, the final loan approval is much quicker once you find the right place.

- Identify Issues Early: The process can flag any potential red flags in your financial profile, giving you a chance to fix them before they become a deal-breaker.

Getting Your Financial Story Straight

When you're chasing a home loan pre-approval, you’re not just submitting paperwork; you're telling your financial story. Lenders need a clear, compelling narrative that proves you’re a reliable borrower they can trust. Every document, from your payslips to your bank statements, adds a chapter to that story, painting a picture of your income, stability, and saving habits.

Think of it like applying for a job. Your application is your financial CV, and the lender is the hiring manager. They want to see a solid track record of good decisions and consistency. Getting your documents organised from the get-go is the best way to make a strong first impression.

The Essential Document Checklist

Lenders need to see the full picture of your financial life. Having all your paperwork ready not only makes the home loan pre approval process faster but also shows you're organised and serious about buying. While the exact list can vary a little between lenders, you'll almost always need to provide these:

- Proof of Income: Your two most recent payslips plus your latest PAYG payment summary (often called a group certificate). This confirms your current, consistent earnings.

- Employment History: A summary of your employment for the last two or three years. Lenders love to see stability, making a steady job history a huge tick in their book.

- Bank Statements: You’ll need three to six months of statements for every transaction and savings account you hold. Lenders will be looking closely at your spending habits and, crucially, your genuine savings.

- Identification: The standard 100 points of ID, like your driver's licence and passport.

- Details of Other Debts: Pull together statements for any credit cards, personal loans, car loans, or HECS/HELP debt. This helps them get a complete picture of your financial commitments.

- Information on Assets: Got other assets, like shares or an investment property? Provide evidence for those, too.

Special Considerations for Self-Employed Applicants

If you run your own business, your financial story is naturally a bit more complex. Without regular payslips, lenders need more comprehensive proof that your income is stable enough to handle a mortgage. You'll need to dig a bit deeper and usually provide:

- Tax Returns: The last two years of your personal and business tax returns.

- Financial Statements: Your profit and loss statements and balance sheets for the same two-year period.

- Notice of Assessment: The Notice of Assessment from the Australian Taxation Office (ATO) for the last two years.

This extra documentation is essential to show that your business is healthy and your income is reliable enough to service a home loan.

Here’s a pro tip: Scan and save all these documents into clearly labelled digital folders before you even start an application. It can literally shave days off the approval process. It also makes the lender's job easier, which is always a good thing for you.

Choosing Your Application Path

Once your documents are all lined up, you have a choice to make: where do you submit them? You can go directly to a bank or work with a mortgage broker. A bank will only offer you its own products, whereas a broker can shop around and compare loans from a whole panel of different lenders.

Understanding the difference between a mortgage broker vs a bank is a critical step in setting yourself up for success. Each has its pros and cons, and the right choice often comes down to how simple or unique your financial situation is.

How Lenders Really Calculate What You Can Borrow

It can often feel like a black box trying to figure out how lenders land on that final pre-approval figure. While your salary is a big piece of the puzzle, it's far from the only thing they look at.

Ultimately, lenders are trying to answer one core question: can you reliably repay this loan without putting yourself under serious financial stress? To do this, they put your finances under a microscope, examining a few key metrics that tell the complete story of your financial health. Understanding these factors helps you see your application through their eyes, giving you the chance to strengthen your position before you even apply.

Let's pull back the curtain on the key factors that shape your borrowing capacity and what you can do to put your best foot forward.

| Factor | Why It Matters to Lenders | How to Optimise It |

|---|---|---|

| Income & Employment Stability | Lenders need to see a consistent, reliable income stream. Stable employment history shows you're a low-risk borrower. | Gather your payslips and employment contracts. If you're self-employed, have at least two years of tax returns ready to demonstrate consistent earnings. |

| Debt-to-Income (DTI) Ratio | This shows how much of your income is already committed to existing debts (credit cards, personal loans). A high DTI is a major red flag. | Pay down high-interest debts like credit cards and personal loans before applying. Consider closing credit card accounts you no longer use. |

| Deposit Size (LVR) | Your deposit determines your Loan-to-Value Ratio (LVR). A bigger deposit means less risk for the lender and more equity for you from day one. | Aim for a 20% deposit if possible to avoid Lenders Mortgage Insurance (LMI). Explore government schemes like the First Home Guarantee if you're struggling to save. |

| Credit Score | Your credit history is a direct reflection of your reliability as a borrower. A high score proves you manage debt responsibly. | Check your credit report for free before applying. Dispute any errors and ensure all your current bills and repayments are made on time. |

| Living Expenses | Lenders scrutinise your bank statements to understand your spending habits. High discretionary spending can reduce your perceived borrowing power. | For a few months before applying, be mindful of your spending on things like dining out, subscriptions, and online shopping. Show them you can live within your means. |

By focusing on these areas, you're not just preparing an application; you're building a stronger financial profile that lenders will see as a safe and reliable investment.

The Debt-to-Income Ratio Unpacked

One of the most critical calculations is your Debt-to-Income (DTI) ratio. This is a simple percentage that shows how much of your monthly gross income is already spoken for by your existing debts. A high DTI is a huge warning sign for lenders, suggesting you might struggle to handle another significant repayment.

They look at everything, including:

- Credit Card Limits: Lenders often assess your total credit card limits, not just your current balance. A common calculation they use assumes 3% of your total limit is a monthly repayment, even if you pay it off in full each month.

- Car Loans and Personal Loans: The actual monthly repayment amounts for any existing loans are factored directly into their sums.

- HECS/HELP Debt: Your student loan is also considered a liability and will be included in their assessment of your overall financial commitments.

A lower DTI signals to the lender that you have plenty of leftover income to comfortably manage a mortgage payment, making you a much more attractive applicant.

Why Your Deposit Size Matters So Much

Another crucial factor is the Loan-to-Value Ratio (LVR). This simply compares the amount of money you want to borrow against the value of the property you intend to buy. A larger deposit means a lower LVR, which is fantastic news for both you and the lender.

From the lender’s perspective, a lower LVR means they are taking on less risk. If you have more of your own money invested in the property, you're seen as a more committed and secure borrower. This reduced risk can often translate into a better interest rate and more favourable loan terms.

A deposit of 20% or more (an LVR of 80% or less) is the magic number. It allows you to avoid paying for Lenders Mortgage Insurance (LMI), which can save you thousands of dollars right from the start.

The Influence of Your Credit Score

Think of your credit score as the lender's snapshot of your borrowing history and reliability. A strong score, built on a history of paying bills on time and managing debt responsibly, tells them you're a low-risk applicant. A lower score, on the other hand, might lead to a smaller pre-approved amount or even a flat-out rejection.

The rising cost of property in Australia has made these calculations even more critical for aspiring homeowners. Recent analysis shows the average new owner-occupier home loan was around $659,922, while first-home buyers were closer to $542,356. These significant figures highlight exactly why lenders are so meticulous in their assessments. You can discover more insights about home loan statistics in Australia and get a clearer picture of the current market.

Navigating the Application and Assessment Phase

Once you’ve got your financial documents in order, you’re ready to dive into the core of the home loan pre-approval process. Whether you’re applying directly to a bank or working with a mortgage broker, this is the point where the lender’s assessment team steps in and puts your financial story under the microscope.

After you hit ‘submit,’ the first thing a lender will do is verify all the information you’ve provided. They’ll be matching your payslips against your bank statements and calling your employer to confirm your job details. This initial check is all about making sure the data is accurate before they get into the nitty-gritty.

The Lender's Stress Test

A huge part of the assessment is the serviceability calculation. Lenders aren't just interested in whether you can afford the repayments right now; they need to know you can still manage if interest rates climb. To figure this out, they add an interest rate "buffer"—usually about 3% higher than the actual rate they’re offering.

This buffer is essentially a stress test. It ensures a future rate hike won’t push your finances to the breaking point, and it’s a massive factor in determining your final pre-approval amount. It’s a cautious approach that protects both you and them.

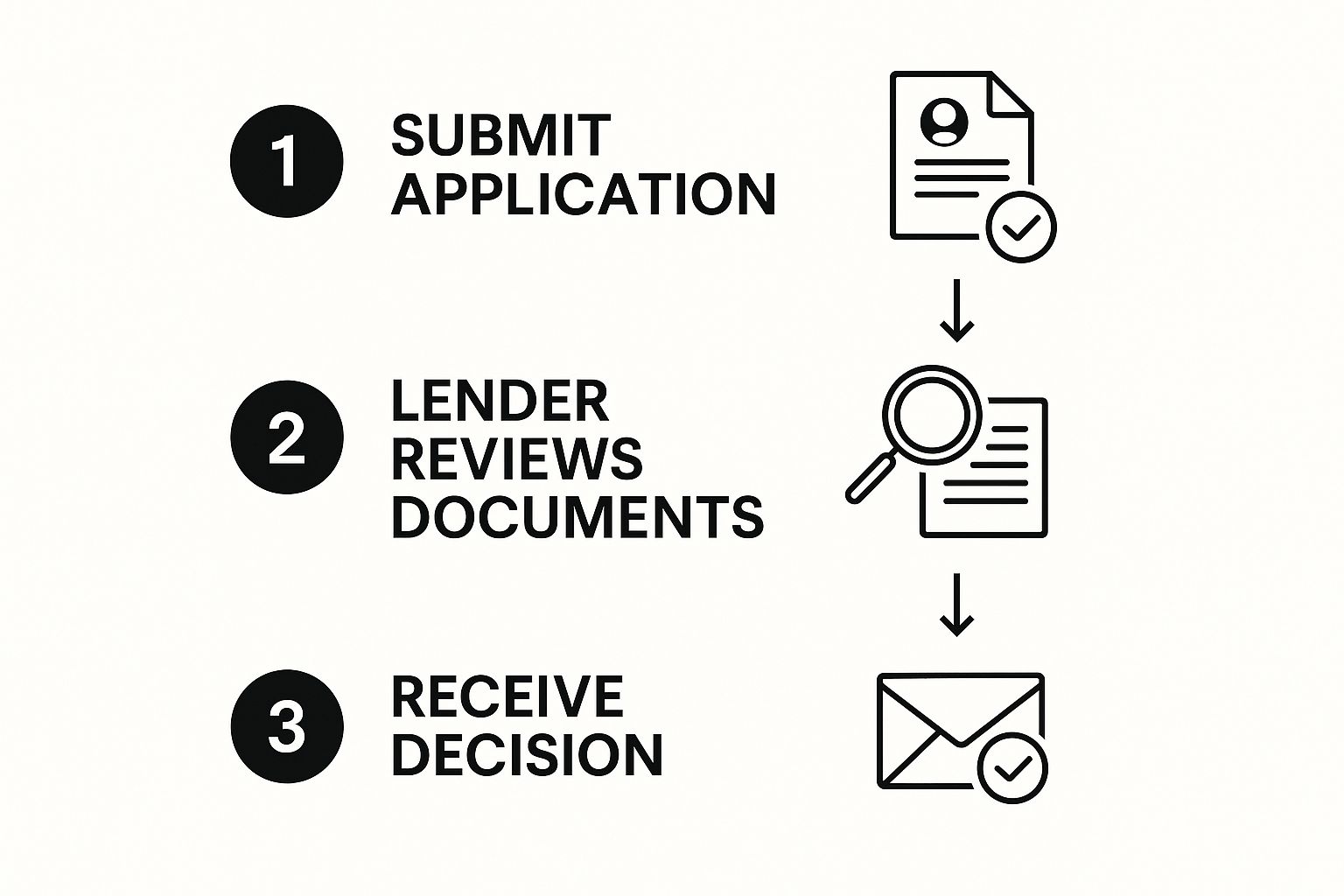

The infographic below gives a simple look at the flow from application to the lender's final decision.

As you can see, after you lodge the application, the lender's review is the most intensive part of the journey before you get an answer.

Credit Checks and Timelines

Next up, the lender runs a hard credit inquiry. This gives them a detailed look at your credit file, including any old defaults or a history of too many credit applications, which can be red flags. A clean credit history really helps to smooth out this stage.

So, how long does all this take? Honestly, it varies. A straightforward application with a major bank might get a thumbs-up in a couple of business days. But if your situation is a bit more complex—maybe you’re self-employed—or if the lender is swamped with applications, it could stretch out to two weeks.

A common roadblock is incomplete or inconsistent documentation. A simple typo on your application or a missing bank statement can send your file to the bottom of the pile, causing frustrating delays. Double-checking every detail before submission is time well spent.

The lender’s assessment is also heavily shaped by what’s happening in the wider economy. For example, the average mortgage rate for housing loans has recently been sitting around 5.76%. Decisions made by the Reserve Bank of Australia on the cash rate directly impact these figures, which then influences how lenders calculate your borrowing power. To get a better feel for the market, you can read more about current Australian mortgage rates. This context helps explain why that serviceability buffer is such a critical part of their risk assessment.

Common Pre Approval Mistakes and How to Avoid Them

The path to securing a home loan pre-approval is usually straightforward, but a few common missteps can easily derail your application. Sidestepping these pitfalls is key to keeping your property dreams on track.

Knowing what can go wrong is the best defence against delays or even an outright rejection.

One of the most frequent errors I see is the "shotgun" approach—applying to multiple lenders at once, hoping for the best. Each application triggers a hard credit inquiry, and several of these in a short period can lower your credit score. Lenders see this as a red flag, suggesting you might be financially stressed or overextending yourself.

Underestimating Your Living Expenses

It’s easy to gloss over your day-to-day spending, but lenders will scrutinise your bank statements to get a real sense of your lifestyle costs. Underestimating your actual living expenses is a classic mistake. Trust me, they’ll look at everything from your daily coffee to streaming subscriptions and weekend spending.

If the numbers you declare don't match the reality reflected in your bank statements, it raises questions about your budget management. Be honest and thorough; it’s far better for a lender to have the real picture upfront.

Another major error is failing to disclose all your debts. That small personal loan or the credit card you barely use still counts. Lenders have ways of finding these things out, and a lack of transparency can damage your credibility and jeopardise the entire home loan pre approval process.

Providing a complete financial picture is essential. If you need a refresher on the basics, our comprehensive guide to home loan pre-approval can help you get organised.

The golden rule from the moment you apply until settlement is simple: freeze all major financial changes. Your pre-approval is based on a snapshot of your finances at a specific moment in time. Any significant change can invalidate it.

Avoid Major Financial Decisions

Making a big financial move during the application or pre-approval period is one of the most damaging mistakes you can make. The lender has approved you based on your financial situation as it was presented. Changing that situation introduces new risk, which they will have to reassess.

Here are a few classic examples of what not to do:

- Financing a new car: This directly impacts your debt-to-income ratio, which is a critical metric for lenders.

- Changing jobs: Even if it’s for a higher salary, a new job introduces instability, especially if you’re in a probationary period.

- Taking on new debt: Applying for new credit cards or personal loans will create more hard inquiries on your credit file and increase your liabilities.

Imagine you get pre-approved and then decide to finance a $40,000 car two weeks before finding your perfect home. When you go back to the lender for final approval, they will recalculate your borrowing capacity with the new car loan.

This new debt could be the very thing that pushes your application from 'approved' to 'denied', causing you to lose the property. Staying financially static is your safest bet.

Your Pre Approval Questions Answered

Even with the best-laid plans, a few tricky questions always seem to pop up during the home loan pre approval process. Getting straight answers is the key to feeling confident and staying on track. Let's tackle some of the most common queries I hear from aspiring homeowners.

Sorting out these details early helps you navigate the final stages without any nasty surprises catching you off guard.

How Long Does a Home Loan Pre Approval Last?

Typically, a home loan pre-approval in Australia is valid for 90 days. Lenders put this three-month window in place because your financial situation can shift, and they need a recent snapshot of your circumstances to stand by their conditional offer.

If you haven't locked in a property within those three months, you'll probably have to re-apply or ask for an extension. It's always a good idea to confirm the exact validity period with your lender. If you're getting close to the expiry date, a quick phone call to your lender or broker can usually get it renewed, often with less paperwork than the first time around.

Does Getting Pre Approved Hurt My Credit Score?

Yes, it can, but the hit is usually minor and temporary. When you apply for pre-approval, the lender runs a "hard inquiry" on your credit report, which is a necessary part of their assessment. A single inquiry is standard practice and won't cause any major damage.

The real danger comes from shopping around and applying with multiple lenders in a short period. Each application triggers a new hard inquiry, which can lower your score more noticeably and make lenders a bit nervous.

The smart way to go is to do your homework on lenders first and apply with your top pick. Better yet, use a mortgage broker who can sound out multiple lenders on your behalf with just a single inquiry on your credit file. If you're just starting out, our first home buyer guide has more tips on getting your finances ready without dinging your credit.

Can a Lender Cancel My Pre Approval?

Absolutely. A pre-approval is always conditional—it’s not a blank cheque. The lender reserves the right to pull the plug if your financial situation takes a nosedive before you've finalised the purchase.

Some common reasons for a lender to cancel include:

- A change in your job: Losing your job is an obvious one, but even starting a new role (especially if you're on probation) can be a red flag.

- Taking on new debt: Financing a new car or racking up a big credit card bill will change your debt-to-income ratio, and not for the better.

- A drop in your credit score: Missing a few bill payments after getting pre-approved can definitely hurt your profile.

- Issues with the property valuation: If the bank's valuer decides the home you want to buy is worth less than what you've offered, it can put the final loan amount in jeopardy.

The main takeaway here? Keep your finances as stable and boring as possible from the moment you get that pre-approval until the keys to your new home are officially in your hand.

Ready to take the next step in your property journey in Mandurah? Whether you're buying your first home or looking to sell, David Beshay Real Estate provides the expert guidance you need. Get your free property appraisal today!