When you're looking to get a home loan, one of your first big decisions is whether to go directly to your bank or to use a mortgage broker. It's a common fork in the road. For most Australians, particularly if your financial situation isn't straightforward or you simply want to see what's out there, a mortgage broker can open up a world of options and provide expert guidance that a single bank just can't match.

Understanding the Fundamental Differences

To choose the right path for your home loan, you first need to understand how each one works. A bank is a direct lender. That means they only offer their own products, and their decisions are governed by a single, internal set of lending rules. This can work if you’re a perfect fit for their criteria and maybe already have a long-standing relationship with them.

A mortgage broker, on the other hand, is your advocate and an intermediary. They aren't tied to any one bank. Instead, they have access to a panel of dozens of lenders, from the big banks to smaller, specialist institutions. Their job is to dive deep into your financial profile and goals, then find the lenders and products that are the best match for you. This one difference completely shapes the experience and the options you'll have.

The numbers speak for themselves. The trend in Australia is clearly moving towards this kind of personalised service. Recent data shows that brokers are now responsible for 74.6% of all new residential home loans—a record-breaking market share worth over $103 billion in a single quarter. This huge shift shows that Aussie borrowers are increasingly seeing the value in the tailored advice and wider market access that brokers bring to the table. You can dig into the details of why Australians are making this choice in this in-depth report.

The key distinction lies in choice and advocacy. A bank sells its own products, whereas a broker shops the market for the product that best serves you.

Before we get into the nitty-gritty, here’s a quick-reference table to frame our comparison. It gives you an immediate sense of the two paths you can take.

Quick Comparison Mortgage Broker vs Bank

To kick things off, this table summarises the core differences between using a mortgage broker and going straight to a bank.

| Attribute | Mortgage Broker | Bank |

|---|---|---|

| Product Choice | Access to dozens of lenders and hundreds of loan products. | Limited to the bank’s own in-house loan products. |

| Primary Role | Acts as an intermediary and advocate for the borrower. | Acts as a direct lender representing its own interests. |

| Service Model | Personalised guidance tailored to your specific situation. | More transactional, focused on selling their products. |

| Best For | Complex situations, first-home buyers, and time-poor individuals. | Straightforward applications and clients with strong bank loyalty. |

This gives a high-level overview, but the real value is in understanding how these differences play out in the real world.

How Brokers and Banks Actually Work

To make a smart choice between a mortgage broker and a bank, you first need to get your head around how they operate. They have fundamentally different business models, and the way they make money directly shapes the service, options, and advice you’ll get. Nailing this down is the first real step in figuring out which path is right for you.

When you walk into a bank, you're entering their world. The loan officer you sit down with is an employee of that bank, and their job is to sell you that bank's specific home loan products. Their entire universe is defined by one set of lending rules and a limited menu of options.

What this means is their loyalty lies with the bank, not you. While they're there to help, the solutions they offer are strictly limited to what their employer has on the shelf, which might not be the best or most competitive deal out there on the wider market.

The Role of a Bank Loan Officer

Going direct to a bank is pretty straightforward. You’re dealing directly with the institution that will lend you the money and manage your loan from day one.

- Product Offerings: They can only show you loans from their own bank’s catalogue.

- Lending Criteria: Your application gets measured against a single, rigid set of internal policies.

- Service Model: The whole process can feel a bit transactional because the officer’s main goal is to sell you one of their in-house products.

This single-lender approach can be efficient, but only if your financial situation is clean-cut and you happen to be the perfect customer they're looking for.

The crucial difference is advocacy. A bank loan officer represents their institution's interests. A mortgage broker is legally required to act in your best interests, placing your needs ahead of their own or the lender's.

The Broker as a Market Navigator

A mortgage broker, on the other hand, is your personal guide and advocate in the home loan market. They aren’t tied down to one institution. Instead, they work with a whole panel of different lenders, from the big banks you know to smaller credit unions and specialist financiers you’ve probably never heard of.

A broker's process always starts with you. They'll do a deep dive into your finances, your borrowing power, and what you want to achieve with your property. Only then do they hit the market to find lenders and products that are a strategic fit for your unique situation. This is especially vital for anyone new to the property game, and our comprehensive first home buyer guide gives you the essential background for this journey.

This saves you the massive headache of researching and applying to a dozen different lenders yourself, which also protects your credit file from getting hit with multiple enquiries. They navigate the market for you, bringing a world of choice right to your doorstep.

Comparing Key Decision-Making Factors

Choosing between a mortgage broker and a bank isn't just a simple preference; it's a decision that can genuinely shape your borrowing experience. To weigh it up properly, you have to look past the surface-level stuff and dig into the factors that really matter. Your financial situation, how complex your application is, and the level of guidance you’re after will all point you in the right direction.

Let's break down the critical areas where brokers and banks really differ, using some real-world examples to show you what each choice looks like in practice.

H3: Loan Choice and Flexibility

The most obvious difference right off the bat is the sheer range of options available. A bank works with a closed set of products—they can only offer you their home loans. This can work out just fine if you’re a perfect fit for what they have, but it’s a naturally limited menu.

A mortgage broker, on the other hand, is like an open marketplace. They aren’t tied to a single institution. Instead, they can show you a huge variety of loans from dozens of lenders, including the big banks, smaller credit unions, and even specialist lenders you’ve probably never heard of.

- Bank Scenario: You’ve got a stable PAYG income, a solid 20% deposit, and your credit score is sparkling. Your bank has a competitive rate, and you’re happy with it. The process is pretty smooth because you tick all their boxes.

- Broker Scenario: You're self-employed with an income that goes up and down. A broker knows which specialist lenders have more flexible ways of verifying income. They can open doors that would otherwise be firmly shut by a big bank’s automated, rigid assessment system.

H3: Interest Rates and Overall Costs

While banks have their standard retail rates, mortgage brokers often get access to wholesale rates from lenders—the kind not offered directly to the public. Because brokers bring a high volume of business to lenders, they often have the leverage to secure better terms for you.

A good broker also knows how to negotiate on your behalf. They understand the ins and outs of lender policies and can push for fee waivers or extra rate discounts, which brings down the total cost of your loan. This is especially important when rates are all over the place. Understanding these trends is crucial—you can get more detail in our guide on how rising interest rates in Australia are affecting borrowers.

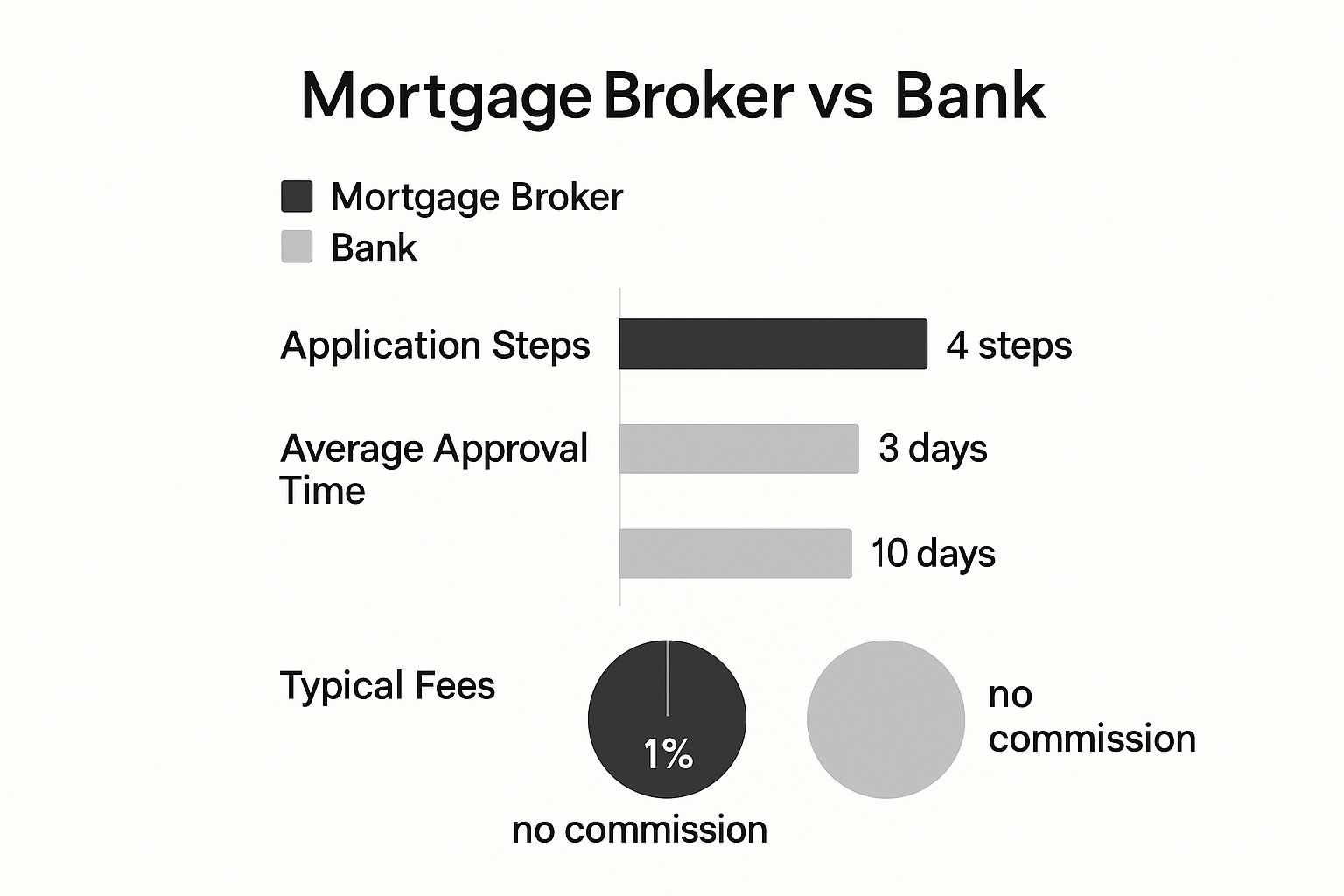

This chart shows just how different the process can be when it comes to time and complexity.

As you can see, a broker can often streamline the paperwork and potentially get you to approval faster.

H3: Approval Success and Personalised Guidance

The national trends speak for themselves. Mortgage brokers are now facilitating a huge chunk of new home loans—71.7% in a recent quarter. That's a massive jump from 59.1% just seven years ago. It really shows how much value borrowers see in having an expert guide them, especially with 80% of borrowers under 35 now using a broker.

One of the biggest advantages is a broker's ability to "workshop" your application. They can spot potential red flags and frame your financial story in the best possible light before it even lands on a lender's desk.

This hands-on approach is a world away from the often transactional feel of dealing with a bank. A bank's loan officer is there to process your application against their specific checklist. A broker’s job is to be your long-term advisor, helping you not just with this purchase but with your future property goals too. It's a relationship-based model that offers a level of personal service a big institution usually can't match.

How Banks Are Adapting to Broker Dominance

The huge growth of the broker channel has completely changed the game in Australian lending, forcing the big banks to rethink how they operate. It's not just about winning your business directly anymore; banks now have to fight hard for a mortgage broker's business, and that competition is great news for you, the borrower. This intense rivalry in the mortgage broker vs bank space is driving real, positive change.

Lenders are now under constant pressure to lift their game, investing in faster technology and offering more flexible credit policies. Why? Because if they don't, brokers will simply take their clients to a competitor. A broker's recommendation is a massive vote of confidence, and banks are battling to stay on their preferred lists.

The Broker Effect on Bank Policies

This market pressure is a powerful quality filter, pushing banks to be more efficient and responsive. Even if you decide to go straight to a bank, the high standards set by the competitive broker market have likely improved the products and services you'll be offered.

This shift means banks have no choice but to prioritise what brokers—and by extension, their clients—value most. A recent industry survey highlighted that the number one priority for brokers when choosing a lender is its credit policy, scoring 4.705 out of 5. This shows brokers demand clear, flexible, and common-sense lending rules for their clients. You can read more about how brokers are shaping bank services in the latest industry report.

The takeaway is clear: brokers aren't just go-betweens. They are strategic partners holding banks accountable. Their collective feedback directly shapes how lenders design products and streamline their processes, making sure the entire market evolves to meet the real-world needs of borrowers.

What This Means for Your Home Loan

This competitive tension has a ripple effect that improves the borrowing experience for everyone. To stay in the game, banks have been forced to make some significant adjustments.

- Faster Turnaround Times: Banks are pouring money into technology to speed up their assessment and approval times, trying to match the efficiency that brokers demand.

- Improved BDM Support: Lenders are beefing up their Business Development Manager (BDM) teams. These BDMs give brokers expert support, helping to sort out complex applications much faster.

- More Flexible Products: The need to cater to the diverse range of client scenarios that brokers bring has pushed banks to develop more niche and adaptable loan products.

At the end of the day, the dominance of the broker channel has created a more customer-focused lending environment. Banks know they are constantly being compared and benchmarked, which is a powerful incentive to innovate and improve their service quality across the board.

Making the Right Choice for Your Situation

The whole "mortgage broker vs bank" debate doesn't have a one-size-fits-all answer. The truth is, the best option comes down to your unique financial situation, how confident you are navigating the loan process, and frankly, how much time you have on your hands. What works perfectly for one person could be a terrible fit for another.

To help you decide, let's move past the generic pros and cons and dive into some real-world scenarios. This will give you a much clearer idea of which path is the smarter move for you, especially in a fast-paced market like Mandurah.

When Going Direct to a Bank Makes Sense

Walking straight into your bank can be a perfectly good strategy, especially if you fit the mould of what they consider an ideal borrower. You’re probably a great candidate to go direct if your situation is clean and simple.

You should consider your bank if:

- You have a long-standing relationship. If you’ve been with your bank for years and have a solid history, they might reward that loyalty with a slightly better rate or a smoother application process because you're a known quantity.

- Your finances are straightforward. Think stable PAYG job, a great credit score, and a healthy deposit of 20% or more. This makes you a low-risk, tick-all-the-boxes applicant that banks love to see.

- You're confident and have time to spare. You feel comfortable doing your own research on the bank's products and are happy that their offer is competitive enough without needing to shop around.

In these cases, the simplicity is a big plus. But you have to accept the trade-off: you're only seeing a tiny slice of the market.

The biggest risk of going direct to a bank is not knowing what you don’t know. You might get what seems like a ‘good’ deal from your bank, but you’ll never be certain it was the best deal available across all lenders.

When a Mortgage Broker Is the Clear Choice

For a huge number of borrowers—especially in today’s lending climate—a mortgage broker offers a massive advantage. Their real value shines when your situation has a bit more complexity to it.

A broker is almost certainly your best bet if:

- You're a first-time home buyer. The process can be overwhelming. The guidance, education, and hand-holding a good broker provides is priceless when you're doing this for the first time.

- Your income isn't a simple 9-to-5. Are you self-employed, a contractor, or do you earn variable commissions? A broker knows exactly which lenders are more flexible with income verification and which ones to avoid.

- You want the most choice with the least hassle. Instead of you filling out endless forms for different banks (and getting multiple hits on your credit file), a broker does the legwork, packaging your application for multiple lenders at once.

- You're determined to get the absolute best deal. Whether you're buying or refinancing, a broker's entire job is to hunt down the most competitive interest rates and loan features. This can save you thousands upon thousands over the life of your loan.

Frequently Asked Questions

When you're weighing up a mortgage broker versus your bank, a few questions always seem to pop up. Getting straight answers is the only way to feel confident about your decision, so let's tackle the most common queries I hear from home buyers.

Do Mortgage Brokers Charge a Fee?

This is usually the first question people ask, and the answer is typically no—at least, you won't be paying them directly. Most of the time, brokers receive a commission from the lender once your home loan settles. This payment isn't an extra charge slapped on top of your loan.

That said, the exact structure can differ. It's always smart to ask for a clear explanation of how the broker gets paid. Any good broker will be upfront about their commissions right from the start; transparency is non-negotiable.

Will Using a Broker Impact My Credit Score?

Actually, using a broker can be a great way to protect your credit score. If you go directly to several banks yourself, each application triggers a separate hard inquiry on your credit file. Too many of those can drag your score down.

A mortgage broker, on the other hand, usually only needs to perform a single credit inquiry. They can then take that one report and present your application to a wide range of lenders, which keeps the impact on your credit history to a minimum. It’s one of the quiet, but significant, advantages brokers bring to the table.

A key takeaway is that a broker shops your application to lenders without shotgunning multiple credit checks. This protects your score while maximising your options.

Can a Bank Offer Me a Better Deal Directly?

It's possible, but it’s not something you should count on. A bank can only ever offer you products from its own lineup. If you’ve been a loyal customer for years and your financial situation is very straightforward, they might roll out a competitive "loyalty" deal to keep you.

However, a broker has access to a much bigger playground, including wholesale rates that aren't available to the public. They effectively create a competitive arena where different lenders have to fight for your business. More often than not, this leads to better overall terms than what a single bank is prepared to offer on its own.

For a deeper dive into common concerns, you can explore our detailed FAQ page for more insights.

Article created using Outrank

Pingback: What Is a Mortgagee Sale in Australia - David Beshay Real Estate - The Agency

Pingback: Mastering the Home Loan Pre Approval Process - David Beshay Real Estate - The Agency

Pingback: Finding the Best Mortgage Brokers Mandurah - David Beshay Real Estate - The Agency

Pingback: What Is Loan to Value Ratio? Learn How It Affects Your Mortgage - David Beshay Real Estate - The Agency

Pingback: How to Get a Home Loan in WA: Your Practical Guide - David Beshay Real Estate - The Agency

Pingback: How to Calculate Borrowing Capacity in Australia - David Beshay Real Estate - The Agency