Figuring out how much you can borrow for a home loan boils down to one simple concept: lenders weigh up your total income against your total debts and living expenses. It's a financial health check, really. They look at your salary, credit card limits, any existing loans, and your day-to-day spending to land on a maximum loan amount they're confident you can manage.

Understanding Your Home Loan Borrowing Power

Before you even think about scrolling through property listings, getting a handle on your borrowing capacity is the most important first step. This number single-handedly dictates your property budget and sets realistic expectations for what you can actually afford.

Think of it from the lender's perspective. It's a risk assessment. They need to be absolutely sure you can handle the repayments, not just on day one, but for the entire life of the loan. To get that confidence, they take a deep dive into your financial world, scrutinising every detail to build a complete picture of your ability to service the loan. This goes way beyond just looking at your payslip; it's a full analysis of your financial habits and commitments.

Key Factors Lenders Analyse for Your Loan

When a lender is deciding how much they’re willing to lend you, they’re essentially putting together a financial jigsaw puzzle. Each piece gives them a clearer picture of the risk and what you can genuinely afford.

Here’s a quick look at the main components they’ll be looking at:

| Factor | What Lenders Look For | Why It Matters |

|---|---|---|

| Income | Your base salary, plus any regular commissions, bonuses, overtime, or rental income. | Non-guaranteed income is often viewed differently, so lenders apply different weightings to assess your stable, ongoing earnings. |

| Financial Commitments | All existing debts are tallied, like car loans, personal loans, and HECS-HELP debt. They also look at your credit card limits, not just the current balance. | The total limit on your credit cards is seen as potential debt you could incur overnight, impacting your ability to repay a home loan. |

| Living Expenses | They compare your declared spending habits against industry benchmarks (like the HEM) and will verify this by reviewing your bank statements. | This ensures your stated expenses are realistic and that you have enough surplus income after covering all your lifestyle costs. |

| The Loan & Deposit | The size of your deposit is a massive factor. This is measured by the Loan to Value Ratio (LVR). | A larger deposit means a lower LVR, which reduces the lender's risk. This often translates to a higher borrowing capacity for you. |

Each of these elements helps the bank build a profile of you as a borrower, and the final number they come up with is a direct result of this detailed assessment.

A larger deposit means you’re borrowing less and have more equity from the start, which is a big tick in the lender's book. You can get a better understanding by exploring our guide on what is Loan to Value Ratio.

With property prices where they are, getting this calculation right is more critical than ever. The average new home loan for an owner-occupier in Australia was recently around $678,000. That figure alone shows why you need a crystal-clear understanding of your financial limits before you even start making offers.

What Lenders See When They Look at Your Finances

When you hand over a home loan application, you’re essentially giving a lender a magnifying glass to inspect your entire financial life. They become detectives, meticulously poring over your income, debts, and spending habits to figure out your true borrowing capacity. It's so much more than just your annual salary; it's about the full picture of money in, money out.

This has become more critical than ever in Australia's hot property market. The average new loan for an owner-occupier recently soared to a record $666,000—that's nearly $300,000 higher than a decade ago. This massive jump shows just how vital it is to get inside a lender's head and understand exactly what they're looking for. You can get more details on these borrowing trends from this housing market analysis.

By seeing your application from their perspective, you can spot potential red flags yourself and sort them out before they ever become an issue.

How Lenders Assess Your Income

In a lender's world, not all income is created equal. They need to feel confident that your earnings are stable and reliable enough to cover repayments for the long haul. Your base salary from a permanent, full-time job is the gold standard because it’s seen as the most dependable.

But of course, plenty of people have more complex income streams. Lenders have specific rules for how they treat these different earnings:

- Bonuses and Commissions: If a big chunk of your pay is performance-based, lenders will want to see a consistent two-year history. Even then, they might only count around 80% of it to buffer against its unpredictable nature.

- Overtime Pay: Just like bonuses, overtime needs to be regular and consistent. If you've only picked up extra shifts for a few months, it probably won't make the cut in their calculations.

- Self-Employed Income: For business owners and contractors, the standard is usually two full years of tax returns and financials. They'll often average out your income over that period to arrive at a conservative figure.

- Rental Income: If you're already an investor, lenders typically only factor in about 80% of the rent you receive. This buffer is there to account for things like vacancies, repairs, and management fees.

This careful vetting is exactly why your borrowing power can swing wildly from one bank to another. For a deeper dive into their different approaches, have a look at our comparison of mortgage brokers vs banks.

The Full Picture of Your Financial Commitments

Once they've tallied up your reliable income, the next move is to subtract all your existing financial commitments. This is where a lot of people get caught by surprise. It’s not just about what you're repaying each month; it's about your total potential debt.

The classic example? Credit cards. Even if you religiously pay off the balance every month, lenders assess your full credit limit.

Key Takeaway: A credit card with a $10,000 limit is treated as a potential $10,000 debt, no matter what your current balance is. Lenders will typically factor in about 3% of that limit as a monthly expense, which can seriously dent your borrowing power.

Here are the common liabilities lenders will plug into their calculators:

- Personal and Car Loans: The outstanding balance and monthly repayments for any existing loans are subtracted directly from your income.

- HECS-HELP Debt: Your student loan is absolutely treated as a liability. Lenders will factor in your compulsory repayment amount based on your income.

- Buy Now Pay Later (BNPL) Services: Frequent use of services like Afterpay or Zip is now under the microscope. Lenders see these as ongoing financial commitments and a window into your spending habits.

- Other Financial Dependents: If you have children or are supporting other family members, these costs are added to your estimated living expenses.

Why Your Living Expenses Matter So Much

This might be the most crucial—and most underestimated—part of the whole assessment. In the past, lenders might have just taken your word for what you spend. Those days are long gone.

Today, lenders start with a benchmark called the Household Expenditure Measure (HEM). This gives them a baseline for modest household spending based on your location, family size, and relationship status. But that's just the beginning.

They will then do a deep dive into your last three to six months of bank statements. They categorise every transaction to build a realistic picture of your lifestyle, looking for patterns in areas like:

- Groceries and dining out

- Entertainment and subscriptions (think Netflix, Spotify, gym memberships)

- Transport costs

- Utilities and bills

- Shopping and personal care

If your actual spending is higher than the HEM benchmark, the lender will always use your higher, real-world figure. This forensic analysis is designed to ensure you aren't low-balling your day-to-day costs, making sure there's enough of a buffer left to comfortably afford your mortgage.

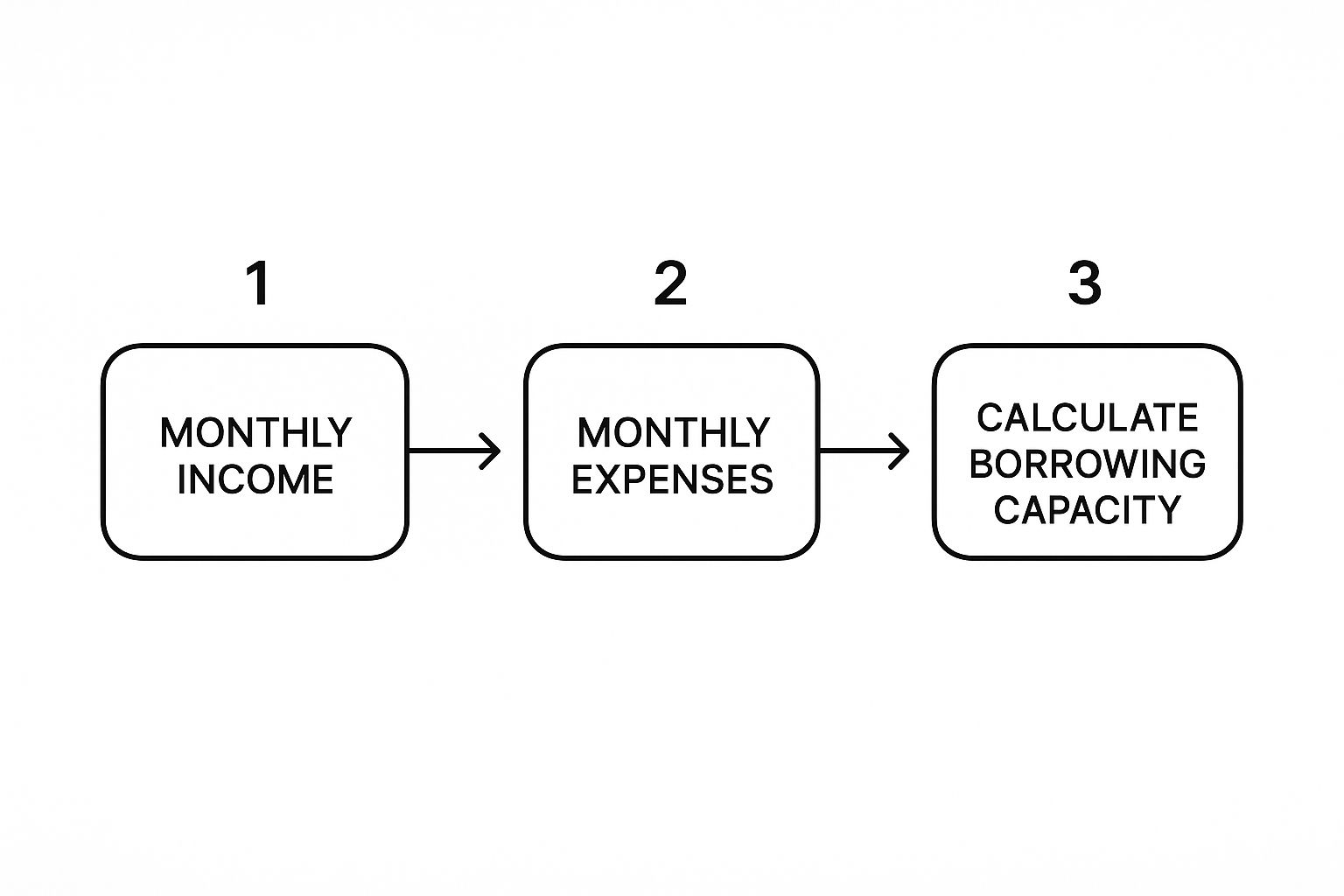

So, you want to know how much you can really borrow? When a lender looks at your application, they aren't just guessing. It's a proper calculation, and it all boils down to two key ideas every Aussie home buyer needs to get their head around: the Debt-to-Income (DTI) ratio and the all-important serviceability buffer.

Understanding how banks use these two figures is a massive advantage. It’s like getting a peek behind the curtain, letting you see your own finances the way a lender does. This way, you can spot potential roadblocks and fix them before you even think about applying.

This simple breakdown shows how a lender takes your income, subtracts your expenses, and lands on your borrowing capacity.

As you can see, it’s fundamentally a process of subtraction. What's left over after all your commitments are paid is what you can put towards a mortgage.

Decoding the Debt-to-Income Ratio

The Debt-to-Income (DTI) ratio is the first big hurdle you need to clear. It’s a simple percentage that stacks up your total monthly debt payments against your gross monthly income. For lenders, it’s a quick-and-dirty test to see if you’re already stretched too thin financially.

Most lenders like to see a DTI ratio below 36%. While some might be a bit more flexible, a lower DTI is always a good thing. It tells the bank you’ve got plenty of cash flow to comfortably handle a new home loan.

Let’s run through a real-world example to see how this works in practice.

Example Debt-to-Income (DTI) Ratio Calculation

Here’s a simplified look at how a DTI ratio is calculated for a typical Australian couple. It's a straightforward process of adding up all monthly debts and comparing them to total monthly income.

| Financial Item | Amount (Monthly) | Calculation Step |

|---|---|---|

| Gross Monthly Income | $12,500 | A combined $150,000 annual income, divided by 12. |

| Car Loan Repayment | $500 | An existing monthly loan payment. |

| Credit Card Limits (2 cards @ $10k each) | $600 | Lenders often use ~3% of the total limit ($20,000) as a monthly expense. |

| HECS-HELP Repayment | $625 | Compulsory repayment based on their income. |

| Total Monthly Debts | $1,725 | The sum of all financial commitments. |

With these numbers, we can figure out their DTI ratio:

($1,725 Total Debts / $12,500 Gross Income) x 100 = 13.8% DTI

A DTI of 13.8% is fantastic. This signals to a lender that the couple has plenty of capacity to take on a mortgage without financial stress.

The Crucial Role of the Serviceability Buffer

Passing the DTI test is only half the story. The next step is where the serviceability buffer comes into play, and it’s a non-negotiable part of every home loan assessment, thanks to the Australian Prudential Regulation Authority (APRA).

Lenders are legally required to add a minimum of 3% on top of the actual interest rate of the home loan you're applying for. Think of it as a "stress test." They need to be sure you could still make your repayments if interest rates were to climb significantly down the track.

This buffer is the single biggest reason why your maximum borrowing power is often lower than you might expect. By assessing your application at a much higher interest rate, the bank protects both you and itself from future market shocks.

Let’s go back to our couple. Imagine they’re applying for a loan with a headline interest rate of 6.0%.

The bank won't assess their repayment ability at that rate. Instead, they'll run the numbers as if the rate was 9.0% (that's the 6.0% rate + the 3.0% buffer).

That higher assessment rate makes the calculated monthly repayment shoot up, which naturally reduces the total loan amount they can service. It’s also why different lenders might offer you different borrowing amounts; some banks add an even larger buffer than the 3% minimum.

You can see the dramatic effect this has by playing around with a reliable mortgage repayments calculator. Plug in your numbers and see for yourself how much a 3% rate jump changes the monthly repayment figure.

How Market Forces Shape Your Lending Potential

While your income and expenses are the bedrock of any borrowing capacity calculation, they don't tell the whole story. Your finances don't exist in a bubble—they’re directly influenced by the wider economy, especially the decisions coming out of the Reserve Bank of Australia (RBA).

Think of it this way: your personal numbers set the stage, but the market conditions ultimately decide how much a bank is willing to lend. A single shift in the RBA's official cash rate can add or subtract tens of thousands from your borrowing power almost overnight, even if nothing about your own situation has changed. Getting your head around these external factors is crucial for timing your application right.

The RBA Cash Rate and Your Borrowing Power

When you hear about the RBA cutting or hiking the cash rate, it’s not just noise in the financial news. It's a direct signal that ripples through the property market. Lenders use the cash rate as their guide for setting home loan interest rates, so when it moves, so do mortgage rates. A lower cash rate usually means lower mortgage rates, which is great news for your borrowing capacity.

Why? It’s pretty simple. A lower interest rate reduces your potential monthly repayments on a loan. This gives you more wiggle room in the bank’s serviceability assessment, allowing them to confidently lend you more money. The difference can be huge.

A household with a combined income of $150,000 recently found they could borrow around $53,700 more than they could just six months earlier. This boost was a direct result of falling interest rates and banks adjusting their serviceability buffers. You can see more on how interest rates are rebuilding borrowing power on Domain.

Of course, the opposite is also true. When the RBA hikes rates to fight inflation, lenders pass those increases on, your assessed repayments climb, and your borrowing power shrinks. It’s a clear example of why timing can be everything.

Strategic Choices That Shift the Numbers

Beyond what the RBA is doing, you have some control. The choices you make about your deposit and loan structure can make a real difference to what a lender will offer you. These are the levers you can actually pull.

One of the biggest is your deposit size. This directly impacts your Loan-to-Value Ratio (LVR)—the percentage of the property’s price you’re borrowing.

- Small Deposit (High LVR): If you only have a 5% deposit, you’re borrowing 95% of the property's value. From a lender's perspective, this is high-risk. You'll almost certainly need to pay for Lenders Mortgage Insurance (LMI), an extra cost often tacked onto your loan that can slightly reduce what you can borrow.

- Large Deposit (Low LVR): A 20% deposit gets you to an 80% LVR. This is the sweet spot that lets you dodge LMI altogether. By presenting a lower risk, lenders are often happier to lend you more and might even offer you a better interest rate.

The type of loan you choose also plays a big part in the assessment.

- Principal and Interest (P&I) Loans: This is the standard option where every repayment chips away at both the interest and the loan balance itself. Lenders like these because you start building equity immediately.

- Interest-Only (IO) Loans: With an IO loan, you only cover the interest for a set period, making your initial repayments much lower. But lenders are much tougher when assessing these. They know your repayments will jump significantly once the interest-only period ends, so they'll typically offer you a lower borrowing capacity compared to a P&I loan to account for that future risk.

By keeping these market dynamics and strategic choices in mind, you can position yourself to get the most out of your application when you’re ready to buy.

Of course. Here is the rewritten section, adopting a more natural, human-written style based on your examples.

How to Maximise Your Borrowing Power

Knowing your borrowing capacity is a great first step, but improving it is where the real work begins. While you can't double your income overnight, there are several practical, high-impact moves you can make right now to look much stronger in the eyes of a lender.

These aren't complex financial strategies. Think of them as simple clean-up jobs that can add tens, if not hundreds, of thousands of dollars to your borrowing power. By tackling the specific areas lenders scrutinise most, you can significantly boost your position and unlock a much higher loan amount.

Tidy Up Your Debts and Liabilities

The single fastest way to increase your borrowing capacity is to reduce your existing financial commitments. From a lender’s perspective, every dollar you owe somewhere else is a dollar you can’t put towards a new mortgage.

Start with the low-hanging fruit. It’s often the small, nagging debts that have an outsized negative impact on your assessment because they represent fixed monthly expenses that eat into your surplus income.

- Pay off small personal loans: That leftover car loan or a small personal loan for a holiday might seem minor, but closing these accounts completely removes them from the liability side of your financial ledger.

- Settle Buy Now Pay Later accounts: Lenders are now looking very closely at services like Afterpay and Zip. Pay off any outstanding balances and, more importantly, close the accounts you aren't using. An open account, even with a zero balance, can still be viewed as an available line of credit.

- Consolidate high-interest debts: If you're juggling multiple credit cards or personal loans, consolidating them into a single loan with a lower interest rate can reduce your total monthly repayments. This directly improves your serviceability.

This isn't just about reducing what you owe; it's about eliminating the monthly repayment obligations altogether. A paid-off car loan doesn't just look good—it frees up hundreds of dollars in your monthly cash flow, which a bank can then factor into your home loan affordability.

The Credit Card Limit Mistake

This is a big one, and it catches so many people by surprise. Lenders don't just look at what you owe on your credit card; they assess the entire credit limit as a potential debt. Even if you have a zero balance, a card with a $20,000 limit is a huge red flag for a lender.

Lenders will typically assume a monthly repayment of around 3% of your total credit card limit. For a $20,000 limit, that’s $600 per month they assume you have to pay—wiping out a significant chunk of your borrowing power before you even start.

Here's the simple fix:

- Review your limits: Be honest with yourself. Do you really need a $15,000 limit on a card you only use for groceries? Probably not.

- Contact your bank: Call your credit card provider and ask them to lower the limit to a more realistic figure, like $2,000 or $3,000.

- Close unused cards: If you have cards you never use, close the accounts completely. Don't just cut them up—formally close them so they no longer appear on your credit file as an open liability.

This simple action can instantly boost your borrowing capacity without you having to pay down a single dollar of existing debt.

Build a Strong and Consistent Savings History

Lenders absolutely love to see a consistent pattern of saving. It's the best evidence you can provide that you have the financial discipline needed to manage a mortgage. A large lump sum that appeared in your account last week from a gift is nice, but it doesn't demonstrate a habit.

What they really want to see is a clear history—ideally over three to six months—of you regularly putting money aside. This shows them two critical things: you can live within your means, and you are capable of making regular, mortgage-sized payments.

Set up an automatic transfer to a dedicated savings account each payday. Even a modest but consistent amount is more powerful than erratic, large deposits. This paper trail of discipline is one of the most compelling arguments you can make to a lender.

Protect Your Credit Score at All Costs

Think of your credit score as your financial reputation. Before you even think about applying for a home loan, it's vital to keep your credit report as clean as possible. A healthy score won't just help you get approved; it can also unlock more competitive interest rates.

The most important rule here is to avoid making multiple credit applications in the months leading up to your home loan submission. Every application for a new credit card, car loan, or even a mobile phone plan can leave a 'hard enquiry' on your credit file.

Too many enquiries in a short period can be interpreted by lenders as a sign of financial stress, making you look like a riskier borrower. It's best to put a freeze on all new credit applications for at least six months before you plan to speak with a broker or a bank. This ensures your credit file is stable and reflects responsible financial management.

Common Questions About Borrowing Capacity

When you start digging into the world of home loans, a bunch of specific questions always seem to pop up. These little details can feel like stumbling blocks, but getting them right is crucial for understanding what you can really borrow.

Let's tackle some of the most frequent queries head-on. Getting these details sorted ensures the borrowing figure you have in your head is as close to reality as possible.

Does My HECS-HELP Debt Affect My Borrowing Capacity?

Yes, it absolutely does. Lenders don't look at your HECS-HELP debt because of the total amount you owe; they're focused on the compulsory repayments. Those repayments come straight out of your salary, which means less net disposable income in your pocket each month.

That reduction in your take-home pay directly hits the amount a lender thinks you can comfortably afford to repay on a home loan. The result? A lower borrowing capacity. You have to declare it on any loan application—it’s going to show up in their assessment anyway.

How Do Lenders View Buy Now Pay Later Services?

Banks and lenders are now paying very close attention to Buy Now Pay Later (BNPL) services like Afterpay and Zip. They’re no longer seen as just harmless shopping tools. Instead, they're viewed as ongoing financial commitments and a window into your spending habits.

If you have regular BNPL repayments showing up on your bank statements, they'll be factored into your living expenses, reducing what you can borrow.

Here's a pro tip: Even if you have zero balances, having multiple BNPL accounts open can be a red flag for a lender, suggesting you might rely on short-term credit. It's a smart move to pay off and formally close any BNPL accounts you don't need well before you apply for a home loan.

This simple bit of financial housekeeping can make your application look much stronger.

How Accurate Are Online Borrowing Capacity Calculators?

Online calculators are a fantastic place to start. They give you a valuable ballpark figure, which is perfect for guiding your initial property search and setting realistic expectations. But it’s vital to remember their results are only an estimate.

Every single lender has its own unique way of assessing an application. They use different interest rate buffers, have their own formulas for calculating living expenses, and varying appetites for risk. A generic online calculator just can't account for every bank's specific policies.

So, use these tools to get a general idea. The only way to get a precise borrowing figure is to go through a full assessment with a mortgage broker or a specific lender.

How Much Deposit Do I Really Need?

While it’s sometimes possible to get a loan with as little as a 5% deposit, there's a good reason why a 20% deposit is considered the gold standard. Hitting that 20% mark gets your Loan-to-Value Ratio (LVR) to 80%—the magic number that lets you avoid paying Lenders Mortgage Insurance (LMI).

LMI is an expensive insurance premium that protects the lender, not you. Worse, the cost is often tacked onto your total loan amount, meaning you end up borrowing more and paying interest on it. By saving a larger deposit to avoid LMI, you reduce the lender's risk, make your application more attractive, and can even unlock better interest rates.

Ready to find out what your property is truly worth? At David Beshay Real Estate, we provide free, accurate property appraisals to help you make informed decisions in the Mandurah market. Get Your Free Property Appraisal Today!