When a borrower stops making their loan repayments, a mortgagee sale is often the lender's final move to recover the money owed. In simple terms, the lender, also known as the mortgagee, takes possession of the secured property and sells it to pay off the outstanding debt.

What Is a Mortgagee Sale Explained

Think of your home loan as a serious agreement between you (the borrower) and the lender (the mortgagee). The property itself is the security for that loan. As long as you keep up your end of the bargain with regular payments, everything ticks along just fine.

But if you default on the loan, the lender can exercise its right to sell the property to recoup what it's owed. This isn't a step taken lightly or quickly. A mortgagee sale is the last resort, usually coming after all other avenues—like negotiating a payment plan—have been exhausted. It's a formal process that kicks in when there's a serious breach of the mortgage contract.

The Core Concept in Simple Terms

It’s a bit like financing a car. If you stop making your car payments, the finance company has the right to repossess the vehicle and sell it to get its money back. A mortgagee sale works on the very same principle, just with a house instead of a car. The lender takes charge of the sale process, with one primary goal in mind: clearing the mortgage debt.

To put it simply, a mortgagee sale is all about debt recovery, not making a profit. While the lender is legally required to act in good faith and aim for a fair market price, its main job is to cover the outstanding loan and any associated costs.

To give you a clearer picture, here’s a quick summary of what a mortgagee sale involves.

Mortgagee Sale at a Glance

| Key Characteristic | What It Means for Buyers & Sellers |

|---|---|

| Lender Controlled | The bank or lender manages the entire sale process, from listing to settlement. The original owner (mortgagor) has no say. |

| Debt Recovery Focus | The primary goal is to pay off the mortgage debt, not to achieve the highest possible price for the homeowner's benefit. |

| 'As Is, Where Is' Sale | Properties are almost always sold in their current condition, with no warranties. Buyers take on the risk of any defects. |

| Limited Information | Buyers may get less information about the property's history or condition compared to a standard sale. |

| Potential for a Bargain | Because the focus is on a quick sale to cover debt, buyers can sometimes purchase a property below its typical market value. |

As you can see, the dynamics are quite different from a regular property transaction, creating both opportunities and risks for those involved.

Key Parties Involved

To really get your head around a mortgagee sale, it’s important to know who the main players are:

- The Mortgagee: This is the lender—think a bank or financial institution—that holds the mortgage. They are the ones who initiate and control the sale.

- The Mortgagor: This is the borrower, the homeowner who has defaulted on their loan repayments. Once the process starts, they have very few rights.

- The Buyer: This is an individual or investor hoping to purchase the property. They are often drawn in by the chance of securing it for a lower-than-market price.

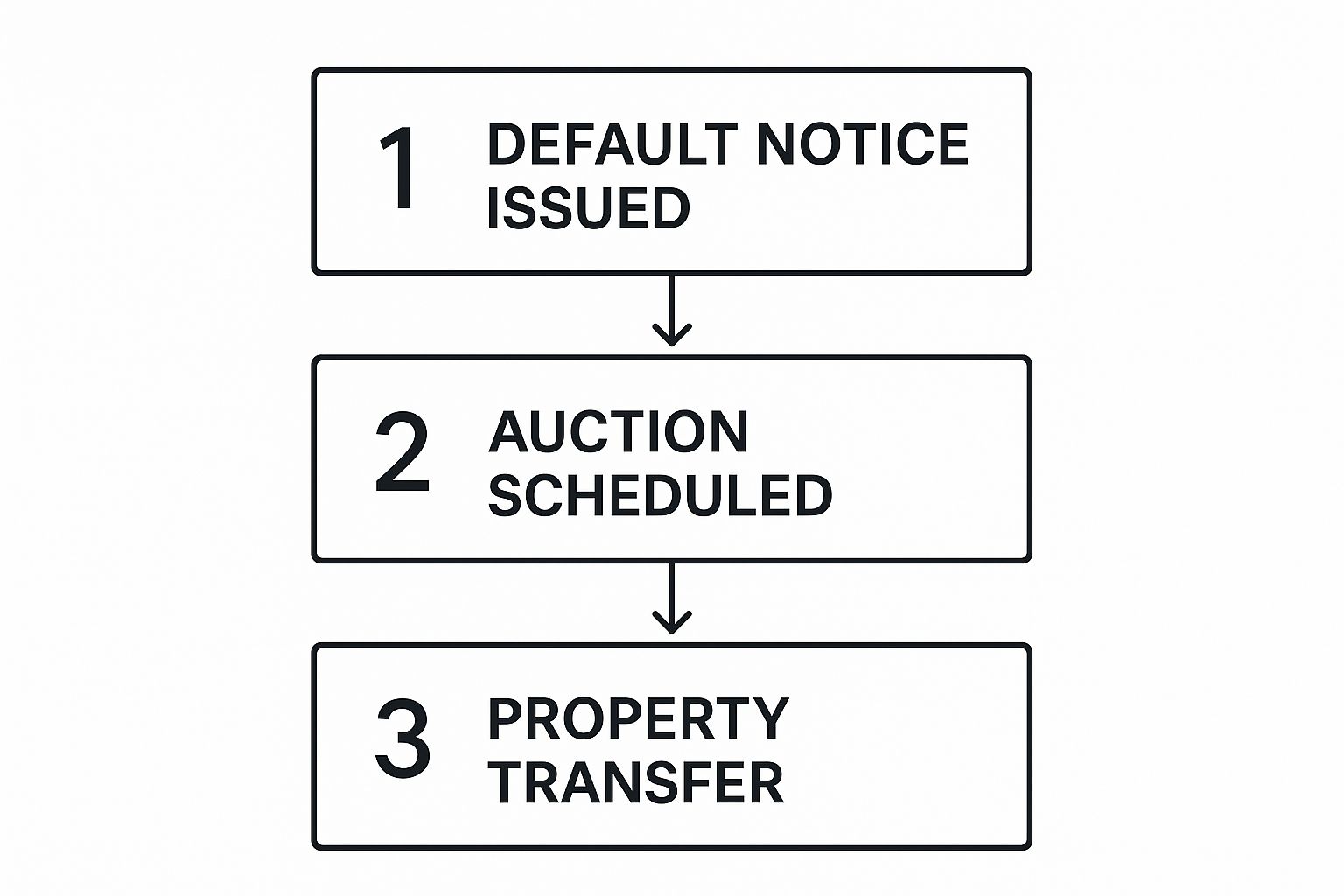

The Legal Journey to a Mortgagee Sale

A mortgagee sale isn't something that happens overnight. It’s actually the final step in a long, legally mapped-out process. This journey starts well before any 'For Sale' sign goes up, kicking off the moment the first mortgage repayment is missed and progressing through a series of formal, regulated stages.

The process is set in motion when a borrower (the mortgagor) falls behind on their loan payments. After a certain period of non-payment, the lender is legally required to issue a default notice. This is an official document telling the homeowner they've breached their loan agreement. It also gives them a specific timeframe, usually about 30 days, to fix the problem by paying what’s overdue.

The Point of No Return

If the borrower can't sort out the default within that window, the lender gets the green light for the next major step. They can start legal proceedings to take possession of the property. This is a critical turning point where control officially shifts from the homeowner to the lender.

Once the lender is in possession, their main goal is to sell the property to recover the money they're owed. This is where you hear the term "mortgagee in possession" used. While the original homeowner still technically owns the property right up until it's sold, they no longer have any control over it.

The infographic below shows the simplified key stages of this journey.

This visual journey makes it clear just how linear and non-negotiable the path is, from that first formal default notice right through to the final property transfer, all governed by a strict legal framework.

The Lender's Legal Duties

Even though the lender is now calling the shots, they can't just sell the property to the first person who waves some cash at them. Australian law places a very important responsibility on the mortgagee.

The lender has a legal duty to act in good faith and take all reasonable steps to sell the property for at least its market value. They must be able to prove that the property was properly advertised and exposed to the open market to attract genuine buyer competition.

This duty is there to protect the borrower from a quick, cheap sale that only covers the lender's immediate losses. The lender must actively market the home, usually by hiring a real estate agent and often selling via public auction to keep the process transparent and fair.

This legal requirement ensures that if there's any money left over from the sale after the debt and costs are paid, it goes back to the original homeowner. If a lender fails to meet this standard, they can end up facing legal action themselves.

The Economic Pressures That Trigger Mortgagee Sales

While a mortgagee sale is always triggered by an individual's financial hardship, it's rarely an isolated event. These situations don't just appear out of nowhere; they are often the result of wider economic shifts that put pressure on household budgets across the board.

Think of it like this: the economy is a bit like the weather, and every household is a small boat trying to navigate it. When a big storm rolls in—like a sudden spike in interest rates or a wave of job losses—a lot of those boats start taking on water at the same time. A mortgagee sale happens when a family can no longer bail the water out fast enough.

For this reason, these sales act as a real-time indicator of the economy's health. They show us exactly where the financial pressure points are for everyday homeowners.

How Economic Shifts Squeeze Homeowners

Several key economic factors can dramatically ramp up the risk of mortgage default in Australia. Each one tightens the financial squeeze on homeowners, making it tougher and tougher to keep up with their repayments.

The most obvious pressure point is rising interest rates. When the Reserve Bank of Australia lifts the cash rate, lenders quickly pass this on to borrowers, and suddenly, monthly mortgage payments are higher. For a family already on a tight budget, even a small jump can be the straw that breaks the camel's back. We’ve seen this happen recently, and you can dive deeper into how rising interest rates in Australia affect homeowners in our detailed article.

Another major trigger is job market instability. If people start losing their jobs or having their work hours cut back, their income takes a direct hit. Without that reliable paycheque, meeting mortgage commitments can become next to impossible.

A mortgagee sale in Australia occurs when a borrower defaults on their home loan, prompting the lender to sell the property to recover the debt. During 2023 and early 2024, Australia saw a rise in housing market stress as climbing mortgage interest rates, which hit an average variable rate of around 7.26% by January 2024, significantly strained borrowers. Learn more about the Australian residential housing market on Statista.com.

Finally, a dip in the property market itself can cause real problems. If property values fall, some homeowners can find themselves in negative equity—meaning their loan is actually worth more than their home. This makes it impossible to sell the property to pay off the debt, trapping them in a tough spot if they can no longer afford the repayments.

Ultimately, these forces show that a mortgagee sale is rarely just one person's story. It’s often a reflection of the economic climate affecting an entire community.

Weighing the Risks and Rewards of Buying

Buying a property through a mortgagee sale can often feel like a high-stakes treasure hunt. The biggest drawcard, without a doubt, is the chance to snap up a property for well under its market value. But that path is paved with serious risks that any potential buyer needs to weigh up carefully.

This isn’t your typical property purchase. Think of it as a calculated gamble where you trade certainty for a rare opportunity. Getting your head around this balance is the first step to making a smart move.

The Allure of a Bargain

The main reason buyers flock to mortgagee sales is the price. The lender isn't looking to make a massive profit; their primary goal is just to recover the outstanding debt as quickly as possible. This means they're often motivated to accept a reasonable offer that covers the loan and any associated costs, which can lead to a sale price that’s comfortably below what the property would fetch on the open market.

For an investor or a first-home buyer, that discount could be the golden ticket into a competitive market or the key to securing a property with fantastic capital growth potential. It's a high-reward play that, if you get it right, can seriously fast-track your property ambitions.

The Inherent Risks of Buying 'As Is'

While the idea of a bargain is compelling, the risks are very real and shouldn't be swept under the rug. The most critical thing to understand is that these properties are almost always sold on an ‘as is, where is’ basis.

This legal phrase is your warning sign. It means you are buying the property in its exact current state, warts and all—both the faults you can see and the ones you can't. The lender offers zero guarantees about the building’s structural integrity, the state of the plumbing, or even if the oven will turn on.

This lack of information and protection throws up several big hurdles:

- No Property History: You won't get the usual rundown from a previous owner about past repairs, renovations, or any known quirks and issues.

- Fixtures and Chattels: There’s no promise that appliances or other items you’d expect to be included in a sale will still be there or in working order.

- Potential for Damage: In some sad situations, resentful former owners might deliberately damage the property before they leave, landing you with unexpected and costly repairs.

This situation is often the result of intense financial stress, where high home prices meet rising interest rates. With the average residential dwelling price in Australia tipped to hit around $976,800 AUD by late 2024, the stakes are incredibly high for everyone. You can read more about the factors influencing Australian mortgages and market pressures on Statista.

To give you a clearer picture, here’s a breakdown of what you're up against.

Risk vs Reward in a Mortgagee Sale

| Potential Rewards (Pros) | Inherent Risks (Cons) |

|---|---|

| Below-Market Price: The biggest draw is securing a property for less than its true value. | 'As Is, Where Is': You buy the property with all its faults, seen and unseen. No warranties. |

| Reduced Competition: The unique nature of these sales can deter less experienced buyers. | Hidden Damage: Potential for vandalism or neglect from previous occupants. |

| High Capital Growth: A lower entry price can lead to stronger long-term returns. | No History or Disclosures: You have limited to no information about past issues or repairs. |

| Quick Transaction: Lenders are motivated to sell quickly, leading to a faster process. | Financing Hurdles: Banks are extra cautious, making loan approval more challenging. |

Navigating these pros and cons requires a sharp eye and a solid strategy.

Navigating the Emotional and Financial Complexities

Beyond the bricks and mortar, a mortgagee sale comes with its own emotional and financial baggage. You’re stepping into a home under difficult circumstances, and that can be an uncomfortable reality to face.

Financially, getting a loan can be trickier too. Lenders will be extra diligent, and having pre-approval isn't just a good idea; it's absolutely essential. Understanding how different lenders operate is crucial, which is why exploring the differences between a mortgage broker vs a bank can give you a real strategic edge.

At the end of the day, a mortgagee sale is a classic high-risk, high-reward opportunity. It demands meticulous due diligence, a healthy emergency fund for surprise repairs, and a cool head in what is often a fast-paced and unforgiving process.

How to Find and Secure Mortgagee Properties

Jumping into the world of mortgagee sales isn't a passive activity; it demands a proactive approach and a sharp eye for opportunity. While you might occasionally spot these listings on major real estate websites, the truly successful buyers know you have to dig a little deeper.

Finding these properties is one thing, but securing them is another. It all comes down to diligent searching followed by even more diligent checking.

Where to Look for Listings

Your search strategy should be a smart mix of online digging and old-fashioned networking. Casting a wide net is key, so don't just rely on a single source, especially if you want to see every opportunity popping up in the Mandurah area.

Here are the key places to focus your search:

- Specialist Websites: Some websites are built specifically for listing distressed assets, including mortgagee and deceased estate sales. For a serious buyer, these platforms are an absolute goldmine.

- Real Estate Agent Networks: Start building relationships with local Mandurah agents who have experience in this niche. They’re often the first to get the call when a lender is about to list a property and can give you a vital heads-up.

- Newspaper and Legal Notices: It might seem old-school, but lenders are legally required to advertise these sales. Keep a close watch on the public notice sections of local and state newspapers, as this is where you'll often find the formal auction announcements.

Once you’ve pinpointed a potential property, that's when the real work begins. The trade-off for the potentially lower price of a mortgagee sale is always higher risk. This is where your due diligence becomes completely non-negotiable.

Your Essential Due Diligence Checklist

Before you even consider putting in an offer, you have to investigate the property from top to bottom. Unlike a standard purchase, what you see is what you get, and there are no second chances once that contract is signed.

Securing a mortgagee property isn't about winning a race; it's about finishing it safely. Your due diligence is your protective gear, shielding you from hidden defects and financial pitfalls that could turn a bargain into a costly mistake.

Here’s a checklist of the critical steps you absolutely must take:

- Get Unconditional Finance Approval: Pre-approval simply isn't enough. You need unconditional, rock-solid finance ready to go. Mortgagee sale contracts come with very strict settlement dates and absolutely no room for delays.

- Order a Comprehensive Building and Pest Inspection: This is non-negotiable. An inspector will uncover any structural problems, pest infestations, or other major defects that the lender definitely won't be disclosing.

- Engage a Solicitor or Conveyancer: Get a legal professional to go over the sale contract line by line. They will spot any unusual clauses or risks that are specific to a mortgagee transaction.

- Research the Property's Value: Don't take the agent's price guide as gospel. Do your own homework on comparable sales in Mandurah to figure out the property’s true market value. The last thing you want is to get caught up in the moment and overpay.

By following this playbook, you can move through the complexities of a mortgagee sale with much more confidence, turning what can be a high-risk opportunity into a well-calculated investment.

Mortgagee Sale vs. Foreclosure vs. Auction

In the Australian property world, you’ll hear terms like mortgagee sale, foreclosure, and auction thrown around, sometimes as if they all mean the same thing. But they don't. For any savvy buyer looking for opportunities in the Mandurah market, getting your head around these differences is absolutely vital.

While they all point to a property being sold due to some kind of financial trouble, the real distinction is about who legally owns the property while the "for sale" sign is up.

The Australian Standard: Mortgagee Sale

Here in Australia, the term you'll encounter most often is mortgagee sale. This is what happens when a lender (the mortgagee) has to step in and take possession of a property because the borrower has defaulted on their loan. The lender then sells the property to get back the money they're owed.

The crucial point here is that the original homeowner (the mortgagor) legally remains the owner right up until the sale is finalised and settled. The bank or lender is simply exercising its right to sell the property on the owner's behalf to cover the debt. This isn't a free-for-all; the process is tightly regulated by state laws that force the lender to act in good faith and aim for a fair market price.

Understanding Foreclosure

Foreclosure is a word you've probably heard a thousand times in American movies, but it's a very different—and much rarer—beast in Australia. In a true foreclosure, the lender doesn't just sell the property; they go to court to take complete legal ownership of it themselves.

Unlike a mortgagee sale where the lender sells the property for the owner, a foreclosure means the lender legally becomes the new owner. They can then choose to sell it, rent it out, or even keep it.

As you can imagine, this is a much more complicated and expensive route for lenders, which is exactly why the more straightforward mortgagee sale is the standard way of doing things across Australia.

Where an Auction Fits In

So, where do auctions come into all this? An auction is simply a method of selling a property, not a type of sale in its own right. A property can be sold via auction, private treaty, or tender.

Many lenders choose to sell mortgagee properties by public auction because it’s a very open and transparent way to show they've done their best to achieve a fair price. It creates a competitive environment and a clear, public outcome.

However, don't assume every auction is a distressed sale. Far from it. Most auctions are just standard property sales where the owner has decided that going under the hammer is the best strategy for them. Given that Perth's property market is seeing strong demand and rapid sales, auctions are an increasingly popular choice for all kinds of sellers trying to get the best result.

Your Questions About Mortgagee Sales Answered

Diving into the world of mortgagee sales can feel a bit like navigating uncharted waters. Whether you're a buyer who smells a potential bargain or a homeowner feeling the pinch, it's natural to have questions. This final section tackles some of the most common queries head-on, giving you the practical clarity you need.

It's no secret that the economy plays a huge role in how often these sales pop up. Historically, mortgagee sales in Australia have ebbed and flowed with interest rate cycles. While we enjoyed relatively stable rates averaging around 4.25% between 2019 and early 2024, recent spikes have squeezed many households. With rates touching a high of 6.15% in early 2025, more borrowers are finding themselves in a tough spot, which unfortunately can lead to more defaults. You can see more on how economic shifts influence the housing market on tradingeconomics.com.

Can the Original Owner Stop a Mortgagee Sale?

Honestly, it's incredibly difficult. Once the legal wheels are in motion and the lender has taken possession of the property, there's really only one way to slam on the brakes: the borrower must pay off the entire outstanding loan balance.

This isn't just the principal and interest; it includes every last cent of the lender's legal fees and associated costs. And it has to be paid in full before a contract of sale is signed with a new buyer. For someone already in financial distress, finding that kind of money is often an impossible hurdle.

Do I Need a Special Type of Loan for a Mortgagee Property?

Not usually, no. A standard home loan is what you'll use. However, you can bet your lender will be extra cautious. They will absolutely insist on a full, independent valuation and will scrutinise your finances with a fine-tooth comb.

It is absolutely crucial to have your finance unconditionally approved before you even think about making an offer. The bank selling the property is not a typical seller; they won't grant you any flexibility or extensions on settlement dates.

Is the Lender Required to Get the Highest Price Possible?

This is a really important point. In Australia, lenders have a legal duty to act in good faith and take reasonable care to get a fair market price for the property.

Now, this doesn't mean they have to hold out for the absolute highest offer imaginable. What it does mean is they can't just sell it for a rock-bottom price to get their money back quickly. They must be able to prove they marketed the property properly and made a genuine effort to attract competition from buyers.

Are you thinking of selling your Mandurah home or looking for your next property investment? Get a clear, accurate picture of your property's value in today's market. Contact David Beshay Real Estate for a free, no-obligation property appraisal and expert advice. Visit https://realestate-david-beshay.com.au to get started.