If you sell an investment property in Australia for more than you paid for it, that profit is subject to Capital Gains Tax (CGT). It’s a common point of confusion, but CGT isn't a separate tax you pay on its own. Instead, the capital gain gets added to your assessable income for the year and is taxed at your usual marginal rate. This rule applies to any assets you've acquired after 20 September 1985.

What Is Capital Gains Tax on Property in Australia

Let's try a simple analogy. Imagine you buy an old, rundown car, pour some money into restoring it, and then sell it for a handsome profit. The Australian Taxation Office (ATO) is only interested in the profit you made, not the total sale price. Capital gains tax on property works in much the same way.

The key thing to grasp is that CGT is based on your net capital gain. This is your total capital gains for the financial year, minus any capital losses you might have incurred and any discounts you’re eligible for. This final figure is then included in your income tax return, which will increase your taxable income for that year.

The Foundation of Australian CGT

Australia introduced CGT way back on 20 September 1985, aiming to create a fairer and more complete income tax system. Any property owned before that date was grandfathered in and remains exempt. As those pre-CGT properties have gradually been sold off over the decades, CGT has become a much more significant factor for property investors.

But the most important rule, and the one that provides peace of mind for most Aussie homeowners, has always been the main residence exemption.

Key Takeaway: For most people, the profit you make from selling the home you live in is completely tax-free. CGT is primarily designed for investment properties, holiday homes, and other real estate assets you hold to generate income or profit.

Understanding the Key CGT Concepts

To get a handle on CGT, you first need to get comfortable with a few core terms. It might seem like tax jargon, but these concepts are the building blocks for calculating your obligations and planning smart investment strategies.

First, you have a CGT event. This is the trigger that requires you to work out if you’ve made a gain or a loss. The most common CGT event is simply selling your property, but it can also be triggered by gifting a property to someone or even if it's destroyed.

Once a CGT event happens, you're on the hook to calculate your financial position. You can explore more real estate insights on our blog.

To help you get started, here’s a quick rundown of the essential terms you’ll come across.

Key CGT Concepts at a Glance

| Term | Simple Explanation |

|---|---|

| CGT Event | The specific action that triggers a capital gain or loss calculation, most commonly the sale of a property. |

| Capital Gain | The profit you make when the sale price of your asset is higher than its cost base. |

| Capital Loss | The loss you incur when the sale price of your asset is lower than its cost base. |

| Cost Base | The total amount your property has cost you, including the purchase price plus other expenses like stamp duty and legal fees. |

| Net Capital Gain | Your total capital gains for the year, minus any capital losses and applicable discounts. This is the amount added to your taxable income. |

| Main Residence Exemption | The rule that generally allows you to sell your primary home without paying any CGT on the profit. |

Getting these basics down is the first step. With this foundation, you'll be better equipped to understand how CGT applies to your specific situation and plan your property investments more effectively.

Calculating Your Property's Capital Gain or Loss

Working out your capital gains tax (CGT) might sound like a headache, but it really just boils down to a simple idea: what you got for your property, minus what it cost you. The Australian Taxation Office (ATO) has specific terms for these two sides of the equation, and getting your head around them is the key to figuring out exactly where you stand.

The whole calculation hinges on two critical numbers: your capital proceeds and your cost base. Nailing these two figures is the first and most important step to determining your final capital gain or loss.

Defining Your Capital Proceeds

Think of capital proceeds as the total money or value you get when you sell your property. For most sales in Australia, this is simply the sale price you and the buyer agreed on.

However, the good news is you can often reduce this figure by subtracting certain selling expenses. These are costs directly tied to the sale of your property. They usually include:

- Real estate agent commissions or fees

- Advertising and marketing costs to promote the sale

- Legal fees for the transaction, like conveyancing

- Auctioneer's fees if you sold that way

By subtracting these costs from your sale price, you arrive at your final capital proceeds. For instance, if you sold a property for $750,000 but had $20,000 in agent and legal fees, your capital proceeds would be $730,000.

Building Your Property's Cost Base

Next up is your cost base. This is the grand total of everything you spent to buy, hold, and improve the property. A higher cost base is your best friend here because it directly shrinks your capital gain—and it’s a lot more than just the price you paid.

The cost base is built from five key elements:

- Acquisition Costs: The original purchase price of the property.

- Incidental Costs: These are the upfront expenses from buying (and later selling), such as stamp duty, legal fees, and surveyor reports.

- Ownership Costs: Things like council rates, land tax, and the interest on your home loan. A crucial catch here: you can only include these if you haven't already claimed them as a tax deduction against rental income.

- Capital Improvement Costs: This covers major upgrades that boost the property's value, like adding a deck, renovating a kitchen, or building an extension.

- Title Costs: Any money spent to preserve or defend your ownership of the property, such as legal fees from a boundary dispute.

Meticulous record-keeping is absolutely essential. Every receipt for a capital improvement or an eligible ownership cost you can find and prove will increase your cost base, directly cutting down the tax you'll owe on your capital gains tax property australia liability.

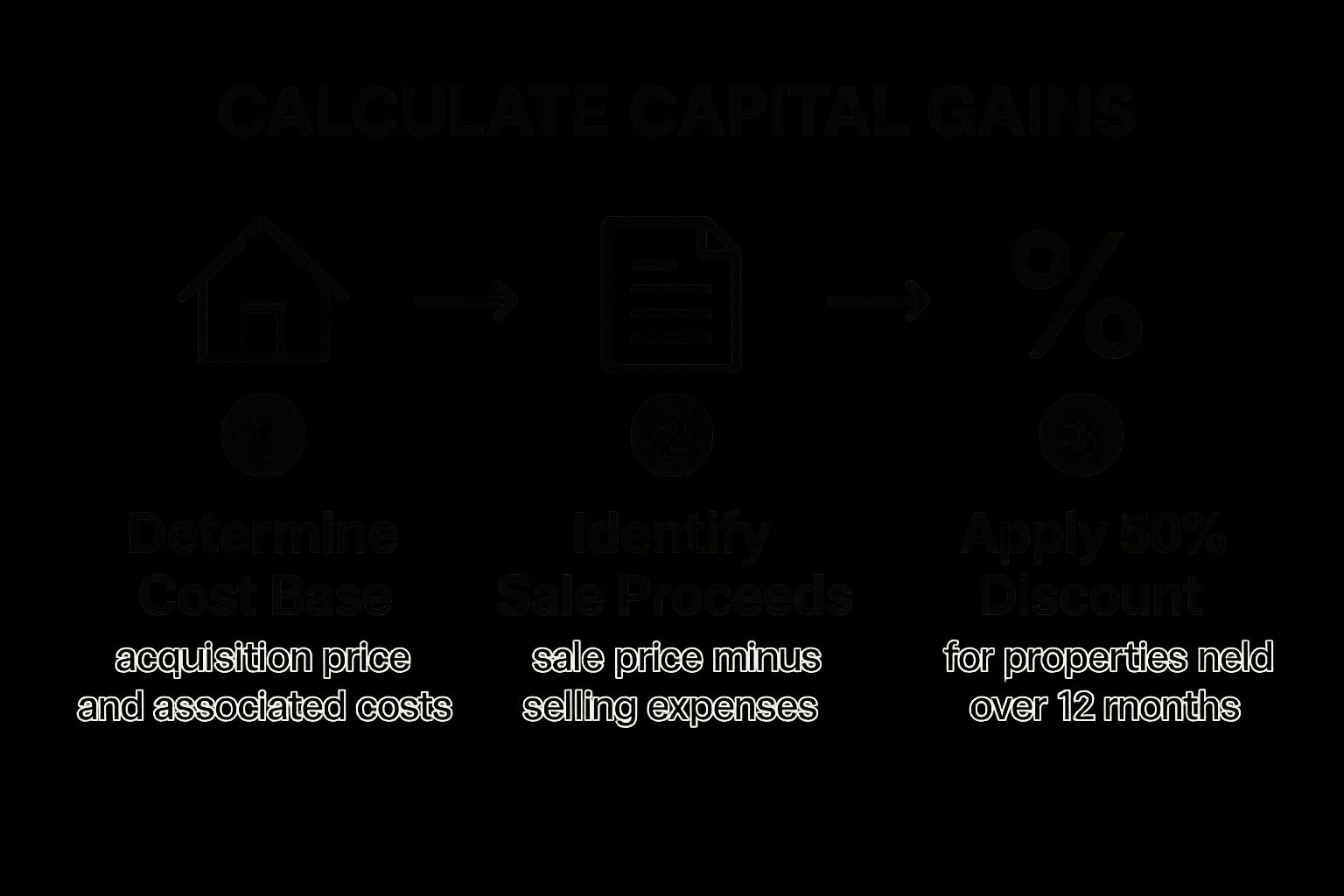

This infographic breaks down the core steps for calculating your potential capital gain.

As the visual shows, once you've worked out your cost base and sale proceeds, applying the 50% discount is a vital final step for investors who have held their property long-term.

Applying the Right Calculation Method

Once you have your capital proceeds and your cost base, you can calculate the raw gain. Just subtract the cost base from the proceeds. If you get a positive number, that's a capital gain. If it's negative, you have a capital loss, which you can use to offset other capital gains.

But a capital gain doesn't mean you're taxed on the whole amount. The ATO has a couple of methods to reduce your taxable gain, with one being far more common for property investors.

- The Discount Method: This is the big one. If you're an individual and have owned the property for more than 12 months, you can slash your capital gain by 50%. This is the go-to method for most property investors in Australia.

- The Indexation Method: This is an older method that's only available for properties you bought before 21 September 1999. It lets you increase your cost base to account for inflation up to that date, which can sometimes lead to a lower tax bill than the discount method. You have to pick one or the other—you can't use both.

By carefully adding up every single eligible expense to maximise your cost base and then applying the right discount, you can make sure you only pay the tax you're legally required to, and not a dollar more.

Understanding The Main Residence Exemption

When it comes to capital gains tax property Australia, the main residence exemption is easily the most important rule for most Aussie homeowners. In a nutshell, it means that when you sell the home you actually live in—your principal place of residence—any profit you make is completely tax-free.

This exemption is really the foundation of Australian property tax law. It’s designed to ensure families aren't hit with a massive tax bill just because their home has naturally gone up in value over the years. But, as we all know, life isn't always that straightforward.

There are a few common situations that can complicate things and affect whether you get the full exemption. It’s absolutely vital to get your head around these scenarios, because they can lead to a partial, or sometimes even total, CGT bill on what you thought was your tax-free family home.

When The Full Exemption Might Not Apply

The easiest way to think about the full main residence exemption is that it applies to the simplest case: you buy a home, live in it the entire time you own it, and it's on a block of land under two hectares. If your situation is any different, you'll need to take a closer look at the rules.

Common curveballs that can impact your exemption include:

- Using part of your home to earn an income (like running a business from a home office).

- Renting out a room or the whole house.

- Owning a property on land bigger than two hectares (which is about five acres).

- Being away from your home for a long time.

Let's unpack what these common situations mean in the real world.

Running a Business from Home

If you use part of your home to run a business, you generally lose the exemption for that specific portion of the property. For example, if you turn a spare bedroom into a dedicated office and start claiming tax deductions for it, that space is no longer considered just part of your home.

Let's say your home has a total floor area of 200 square metres and your dedicated home office is 20 square metres (10% of the total area). When you eventually sell, you'd likely need to calculate capital gains on 10% of the profit. It’s a matter of fairness—you can't claim business deductions on a space and then also get a completely tax-free gain on it.

Key Insight: The moment you claim business-related expenses for part of your home (like a portion of your mortgage interest or depreciation), you're flagging to the ATO that this area has an income-producing purpose. This is where meticulous record-keeping becomes your best friend, as you'll need it to correctly calculate the capital gain down the track.

The Six-Year Absence Rule

So, what happens if you have to move out of your home for a while? Maybe you’ve been transferred for work or you’re taking an extended trip overseas. The ATO has a pretty generous rule for this, known as the “six-year rule”.

This rule lets you treat your property as your main residence for up to six years after you move out, as long as you use it to generate income (in other words, you rent it out).

During this six-year window, you can still claim the full main residence exemption when you sell, provided you don't buy another property and call that your main residence. If you're away for more than six years, you’ll be on the hook for CGT for the period that goes beyond that six-year limit.

What's really interesting is that if you don't rent the property out, you can technically be absent from it indefinitely and still keep the exemption. The key condition, again, is that you don't nominate another home as your main residence. This flexibility is a massive advantage for homeowners who need to relocate temporarily.

Unlocking CGT Discounts for Property Investors

Beyond the main residence exemption, which is a huge benefit in itself, the Australian tax system has some powerful tools for property investors looking to reduce their Capital Gains Tax (CGT) bill. The most important one by a long shot is the 50% CGT discount. It’s the cornerstone of any smart, long-term property investment strategy and the main reason why patience really pays off in real estate.

It’s actually quite simple. If you’re an individual Australian resident for tax purposes and you hold onto an investment property for more than 12 months before selling, you get to cut your taxable capital gain in half. This one rule can save you thousands of dollars and completely changes the financial outcome of your investment.

This major CGT change came into effect back in 1999. Before that, the system was a lot different—your capital gains were just taxed at your full marginal rate. The 1999 reform swapped the old, clunky 'indexation' method for the much simpler 50% discount, aiming to spur on investment and make things easier. If you're a history buff, you can dig into the details of how Australian tax policy has shifted over the years.

The 50% CGT Discount in Action

Let's walk through how this works with a real-world example. Say you bought an investment apartment five years ago and now you've decided it's time to sell.

- Your Capital Gain: After you subtract your total cost base from what you sold it for (your capital proceeds), you're left with a capital gain of $100,000.

- Applying the Discount: Because you owned the property for well over 12 months, you're eligible for the 50% CGT discount.

- Your Taxable Gain: You slice that gain in half. This means only $50,000 gets added to your assessable income for the year.

If this discount didn't exist, the whole $100,000 would be piled onto your income. That could easily push you into a higher tax bracket and leave you with a much bigger tax bill. This is exactly why holding an asset for at least one year and a day is a fundamental play for any serious property investor.

Important Note: This 50% discount is available to individuals and trusts. However, companies are not eligible for the CGT discount. This is a critical factor to consider when deciding on the ownership structure for your investment property.

Using Capital Losses to Your Advantage

Another key strategy for managing your CGT is using losses to offset your gains. A capital loss happens when you sell an asset for less than what it cost you (its cost base). While no one ever aims to make a loss, they can be a surprisingly valuable tool when it comes to tax planning.

You can't just deduct a capital loss from your regular salary or business income. What you can do is use it to cancel out your capital gains. And it’s not just limited to property—you could use a loss from selling shares, for instance, to reduce a gain you made on a property sale.

Here’s the order of operations:

- Calculate Total Gains: First, add up all your capital gains for the financial year.

- Subtract Capital Losses: Next, subtract any capital losses you have from this year or have carried forward from previous years.

- Apply the Discount: Only after you've subtracted your losses do you apply the 50% CGT discount (if you're eligible) to whatever gain is left over.

For example, imagine you had a $100,000 gain from a property sale but also a $20,000 loss from selling some shares. You’d first subtract the loss, which brings your net gain down to $80,000. Then, you apply the 50% discount to that amount, leaving you with a final taxable gain of $40,000. This kind of strategic offsetting is crucial for managing your entire investment portfolio and keeping your tax bill as low as legally possible.

Proven Strategies to Legally Minimise Your CGT

Knowing the rules of Capital Gains Tax is one thing, but using them to your advantage is where the real magic happens. With a bit of smart planning, you can legally and significantly reduce the tax you’ll owe on your property sale. These strategies aren't about shady loopholes; they're about making savvy, informed decisions that work within Australian tax law.

Honestly, the most effective ways to manage your capital gains tax property australia bill often just come down to good timing and being incredibly organised. It’s all about looking at the big picture of your finances, not just the property sale in isolation.

Time the Sale to Your Advantage

One of the simplest yet most powerful strategies is all about timing. Remember, your net capital gain gets added straight on top of your assessable income for the financial year. This means the actual tax you pay is tied directly to your marginal tax rate for that specific year.

If you have the flexibility, try to sell your investment property in a year when you know your overall income will be lower. This could be a year where you’re:

- Taking a career break or enjoying some long-service leave.

- Winding down for retirement with a reduced income.

- Working part-time or have seen your earnings dip for another reason.

By finalising the sale (that’s when the contract is signed, not when it settles) in a lower-income year, you make sure the capital gain is taxed at a much friendlier marginal rate. This simple act of strategic timing can genuinely save you thousands of dollars.

The Power of Meticulous Record-Keeping

I really can’t overstate this: keep every single receipt and invoice related to your property. Every dollar you can legitimately add to your cost base is a dollar less of taxable capital gain. Think of your cost base as a growing shield protecting you from CGT.

From the day you buy, you should be keeping detailed records of:

- Initial Purchase Costs: This includes stamp duty, your conveyancing fees, and any building inspection reports.

- Improvement Costs: This is for the big stuff—invoices for a new kitchen, adding a deck, or building an extension. It's different from general repairs and maintenance.

- Ownership Costs: If you haven’t already claimed them as a tax deduction against rental income, things like council rates, land tax, and interest on your loan can often be included.

- Selling Costs: Don’t forget the expenses at the end, like real estate agent commissions and the legal fees for the sale.

Expert Tip: The moment you buy an investment property, create a dedicated digital folder or a physical file for it. Every time you spend money on a capital cost, scan the receipt and drop it in there. Trust me, the future you will be incredibly thankful for this small habit.

Advanced Ownership and Structuring Strategies

For investors with a more complex portfolio or those planning for the long haul, the ownership structure itself becomes a key part of the strategy. A straightforward tactic is owning an investment property in the name of the spouse who earns less. This can ensure any future capital gain is taxed at their lower rate.

Another powerful approach is using a family trust. A trust gives you incredible flexibility to distribute the capital gain among different beneficiaries, who might be on much lower tax brackets. This is especially handy for long-term wealth creation and planning for the next generation.

Of course, these structures come with their own costs and complexities, so getting professional financial advice here is non-negotiable. Even your selling method can affect the final numbers; you can learn more by checking out the pros and cons of an off-market property sale. By putting these proven strategies into action, you can take back control and make sure you walk away with the best possible financial result.

How to Report and Pay CGT to the ATO

Once your property sale is finalised and the dust has settled, there’s one last crucial step: squaring up with the Australian Taxation Office (ATO). Many people assume CGT is a separate, standalone tax they need to pay immediately. It’s actually much simpler than that.

Your capital gain isn't taxed on its own. Instead, it’s added to your other earnings for the financial year, like your salary or business income. This total figure becomes your assessable income, which then determines the tax bracket you fall into. It’s a core principle of how capital gains tax on property in Australia works, and it’s all handled through your annual tax return.

Lodging Your Income Tax Return

When tax time rolls around, you’ll need to declare your capital gain. The ATO has a specific "Capital gains or losses" section in the tax return (whether you're using myTax online or a paper form) where you’ll report the transaction. Here, you’ll detail your total capital gains and offset them with any capital losses you might have.

The final number—your net capital gain after all discounts and losses are applied—is what gets added to your income. This is why the timing of your sale can be so important. A large capital gain in a year where you also had a high salary could easily push you into a higher tax bracket, meaning a bigger tax bill.

These property transactions are a huge part of the national economy. The ATO’s own data reveals that real estate gains make up a massive slice of the total capital gains reported each year. You can actually see the trends for yourself by exploring the government's housing data reports.

Crucial Reminder: If you're lodging your own tax return, the deadline is typically 31 October. Using a registered tax agent often gives you a later deadline, but you must engage them before the October cut-off. Missing these dates can result in penalties from the ATO, so don’t leave it to the last minute.

Key Details for Your Tax Return

To make sure lodging is a smooth process, get your paperwork in order well beforehand. Meticulous record-keeping isn't just good practice; it’s non-negotiable. The ATO can, and does, ask for documentation to verify your figures.

Here’s a checklist of the critical numbers you'll need:

- Date of the CGT event: This is the contract date, not the settlement date. It’s a common point of confusion.

- Capital proceeds: The final sale price less any costs you incurred to sell (like agent fees and legal costs).

- Cost base: The original purchase price plus all the other eligible expenses you’ve tracked over the years.

- Net capital gain or loss: The final figure you’ve calculated after applying any discounts or losses.

By understanding that CGT is simply part of your standard tax return, you can confidently handle this final part of your property journey. With good records, the process is straightforward, ensuring you meet your obligations accurately and on time.

Frequently Asked Questions About Property CGT

Diving into the world of property tax can feel like learning a new language. When it comes to capital gains tax on property in Australia, the general rules are one thing, but it’s how they apply to your specific situation that really counts. This section tackles some of the most common questions we hear from property owners just like you.

We’ve kept the answers direct and practical to clear up the confusion around these common, yet often tricky, scenarios. Whether you're dealing with an inherited home, wondering about renovations, or trying to figure out the tax implications of a knockdown-rebuild, we've got you covered.

What Happens if I Inherit a Property?

Inheriting a property often happens during an emotional and complicated time, and honestly, CGT is probably the last thing on your mind. But it pays to understand the rules, as they’re quite specific and depend on when the deceased first bought the property and what you choose to do with it.

There's some good news. If the property was the main home of the person who passed away and you sell it within two years of their death, you can usually claim a full CGT exemption. This gives you a clear window to manage the estate without worrying about an unexpected tax bill.

However, if you decide to rent out the inherited property, it instantly becomes an investment asset in the eyes of the ATO. From that day forward, you’ll need to know its market value. When you eventually sell, you'll be liable for CGT on any capital growth from the date it first started earning you income.

Key Consideration: When you inherit a property, you also inherit its cost base for CGT purposes. If it was a pre-CGT asset (bought before 20 September 1985), you’ll use its market value at the date of death. If it was a post-CGT asset, you generally take on the deceased's original cost base.

To make it clearer, let’s look at how the rules differ between inheriting a property and being gifted one.

CGT Scenarios for Inherited vs Gifted Property

| Scenario | Inherited Property | Gifted Property |

|---|---|---|

| Your Cost Base | Usually, the market value at the date of death or the deceased's original cost base. | The market value of the property on the day you received it. |

| CGT Event Trigger | CGT is calculated only when you sell the property down the track. | The person gifting you the property might have to pay CGT at the time of the transfer. |

| Main Residence Exemption | Can be available if you sell within two years of the owner's death. | The exemption status depends on how both the giver and the receiver used the property. |

As you can see, the tax implications can be vastly different, so it's always worth getting specific advice for your situation.

Do Renovations Affect My CGT?

Absolutely. In fact, major renovations and capital improvements are one of the most powerful tools you have to reduce your future capital gains tax bill. Why? Because they increase your property's cost base. But it’s crucial to know the difference between an 'improvement' and a simple 'repair'.

A repair is just maintenance—think fixing a leaky tap or replacing a cracked window pane. A capital improvement, on the other hand, is something that fundamentally adds to the property’s value or structure. We’re talking about things like:

- Building an extension

- Adding a swimming pool

- A full-blown kitchen or bathroom renovation

- Constructing a brand-new deck or pergola

Think of it this way: repairs bring something back to its original condition, while improvements take it to a new level. Every dollar you spend on a genuine capital improvement gets added to your cost base, which directly shrinks the taxable profit you’ll make when you sell.

What if I Demolish and Rebuild an Investment Property?

A knockdown-rebuild is a massive project with its own set of CGT rules. The cost of demolishing the old house can actually be added to the cost base of the original land.

From there, every expense tied to building the new home—from the architect's plans to the builder’s invoices and materials—forms a new, separate cost base for the new building itself. When you finally sell the new property, you're essentially dealing with two assets: the original land and the new building, each with its own cost base. The viability of a project like this can also hinge on market conditions, like whether there's a shortage of homes for sale. This two-part approach ensures you account for all your expenses properly when it’s time to calculate your final capital gain.

Navigating the specifics of Capital Gains Tax can feel overwhelming, but you don't have to do it alone. For expert guidance on your property's value and how to achieve the best possible sale outcome in the Mandurah market, reach out to David Beshay Real Estate. Get your free, no-obligation property appraisal today and make your next move with confidence. https://realestate-david-beshay.com.au

Article created using Outrank

Pingback: Unlocking Investment Property Tax Benefits - David Beshay Real Estate - The Agency

Pingback: What Is Negative Gearing? Your Essential Guide for Investors - David Beshay Real Estate - The Agency

Pingback: Using a Property Investment Calculator Australia - David Beshay Real Estate - The Agency

Pingback: Your Guide to Commission Fee Real Estate in Australia - David Beshay Real Estate - The Agency