When you're starting to think about buying a house in Australia, the whole process can feel a bit overwhelming. A house deposit calculator is hands-down the best tool to bring your goal back down to earth. It takes that huge, intimidating number you need to save and turns it into a clear, step-by-step plan, showing you exactly how much you need and a realistic timeframe to get there.

Your First Real Step Towards Owning a Home

Every home ownership dream starts with figuring out that all-important number: your deposit. A good house deposit calculator cuts through the noise and gives you a tangible roadmap, turning a vague wish into a concrete project. It’s not just about hitting one big savings target; it's about seeing all the smaller milestones you'll hit along the way.

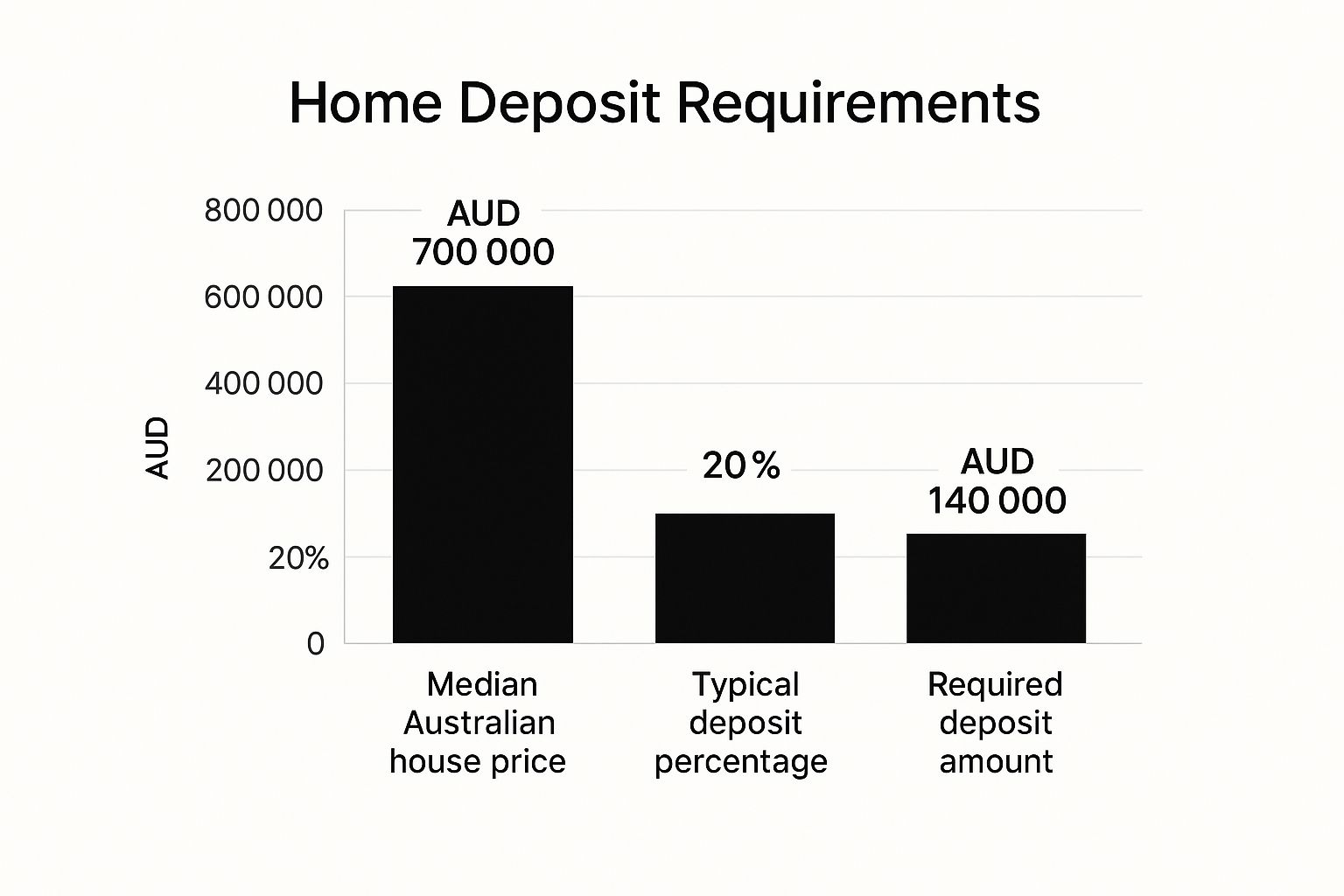

The gold standard for a home deposit in Australia is 20% of the property’s price. If you can hit this magic number, you get to sidestep an extra expense called Lenders Mortgage Insurance (LMI). LMI is a policy that protects the bank—not you—in case you can't make your repayments. For a lot of first-home buyers, saving a full 20% feels like a massive mountain to climb, but this is where a calculator really shines. It shows you how all those smaller, consistent savings efforts build up over time.

This image gives you a clear picture of how these numbers stack up against a typical Aussie property price.

As you can see, the difference between the property price and what you need for a deposit is pretty significant. This is exactly why having a structured savings plan is non-negotiable.

What’s the Deal With LMI?

Most lenders in Australia will let you get started with a deposit as low as 5% of the property’s value. The catch? Anything less than that 20% benchmark means you’ll almost certainly have to pay for LMI.

Let's look at how this plays out with a few different scenarios. Imagine you're eyeing a property worth $700,000. The table below breaks down what your upfront costs might look like depending on the size of your deposit.

Deposit Scenarios for a $700,000 Property

| Deposit Percentage | Deposit Amount | LMI Payable (Approx.) | Total Upfront Cost (Approx.) |

|---|---|---|---|

| 5% | $35,000 | $31,500 | $66,500 |

| 10% | $70,000 | $15,400 | $85,400 |

| 20% | $140,000 | $0 | $140,000 |

As you can see, while a smaller deposit gets you into the market sooner, the added cost of LMI can be substantial. You can learn more about the essentials of home deposits from money.com.au.

Your deposit size is one of the most powerful levers you have. A larger deposit not only helps you avoid LMI but can also lead to a lower interest rate and more manageable monthly mortgage repayments.

Playing around with a house deposit calculator is the first practical step you can take. It lets you experiment with different savings amounts and timelines, empowering you to find that sweet spot between what you can realistically save and the property you're aiming for.

Getting the Most Out of a Deposit Calculator

Think of a house deposit calculator as your first real financial blueprint for buying a home. Its usefulness comes down to one simple thing: the quality of the numbers you punch in. Let's walk through how to feed it the right information so you get a truly reliable picture of your path to home ownership.

First things first, plug in the desired property price. The key here is to be grounded in reality. Spend some time researching median prices in the suburbs you’re actually interested in. For example, if you’ve got your eye on a place in Mandurah for around $650,000, use that as your starting point.

Next, you’ll enter your current savings – that’s the pot of money you’ve already earmarked for your deposit.

Then, tell the calculator your regular savings contribution. This isn't what you hope to save; it's the amount you can realistically and consistently squirrel away each month. If you know you can comfortably put aside $1,500 a month without fail, that’s the figure to use. Being honest here is what makes the timeline accurate.

Looking Beyond the Big Numbers

A really good deposit calculator won't just ask for the basics. It will have fields for other crucial details that make a huge difference in the real world of buying property in Australia. Don't gloss over these – they're what give you the full, unvarnished truth about your upfront costs.

You'll often find these extra inputs:

- Government Grants: Are you a first-timer? Check if you're eligible for the First Home Owner Grant (FHOG) in Western Australia. Ticking this box can give your savings a serious boost right from the start.

- The 'Other' Costs: Smart calculators will nudge you to account for things like stamp duty, conveyancing fees, and building inspections. As a rule of thumb, I always advise clients to budget an extra 3-5% of the purchase price to cover these expenses.

- Savings Account Interest: If your deposit is sitting in a high-interest savings account, don’t forget to add that in. Even a modest 4.5% annual interest rate will compound over time and can help trim a few months off your savings journey.

The whole point of the calculator is to map out the relationship between your deposit, the property's value, and how much you'll need to borrow. This all ties back to your Loan to Value Ratio (LVR), a number that banks care about a lot. If you're not familiar with it, have a read of our guide on what the Loan to Value Ratio is. It’s essential for understanding your borrowing power.

When you take the time to fill in these details properly, the calculator stops being a simple gimmick and becomes a seriously powerful planning tool.

From Numbers on a Screen to a Solid Savings Plan

Alright, you’ve punched the numbers into a house deposit calculator and have a figure staring back at you. That timeline—whether it's two years or ten—is more than just data. It’s the starting block for your entire home-buying journey.

But what do you do with that number? The real magic happens when you connect that savings goal to the mortgage you’ll one day have.

Think of your deposit as a massive head start. The more you save now, the less you have to borrow. A bigger deposit means smaller monthly mortgage repayments down the track, freeing up your cash for everything else life throws at you.

How a Bigger Deposit Shapes Your Financial Future

Getting to that 20% deposit isn't just about avoiding Lenders Mortgage Insurance (though that's a huge win). It’s about setting yourself up for a much healthier financial life for the next 25 or 30 years.

A smaller loan means you’ll pay far less in interest over the life of your mortgage—we’re talking tens of thousands of dollars saved.

Your deposit size is the single biggest factor influencing your borrowing power. Lenders see a larger deposit as a sign of financial discipline, which can lead to better loan terms and a smoother approval process.

With the average new home loan in Australia hovering around $678,011, typical monthly repayments are pushing close to $4,000. These are serious numbers, and they show just how vital a solid deposit is for managing such a big commitment. You can dig deeper into these national figures over at Money.com.au's home loan statistics page.

A disciplined savings plan today is what buys you financial breathing room tomorrow. It’s the difference between just buying a house and owning it comfortably.

Once you feel your savings plan is on solid ground, it's time to take the next step. Finding out where you stand with lenders by getting home loan pre-approval gives you the green light to start searching for your new home with real confidence.

Don't Forget the Extra Costs of Buying a Home

Saving for your deposit feels like the main event, and it is a huge achievement. But I've seen too many buyers get a nasty shock when they realise the deposit is just one piece of the puzzle. It’s easy to get tunnel vision on that big savings goal, but you absolutely have to plan for the other costs that pop up just before you get the keys.

These aren't "hidden" costs, but they are often overlooked in the early stages of planning.

To avoid that last-minute scramble for cash, a good rule of thumb is to budget an extra 3% to 5% of the property’s value. So, if you're looking at a $700,000 home, that's another $21,000 to $35,000 you’ll need on top of your deposit. Factoring this in from day one makes all the difference.

What Are These Upfront Costs?

So, where does all that extra money actually go? It's not just one thing, but a collection of essential fees and charges. Here’s a quick rundown of what to expect after your offer is accepted:

- Stamp Duty: This is almost always the biggest extra expense. It’s a state government tax on your property purchase, and the amount varies wildly depending on where you buy.

- Legal & Conveyancing Fees: You’ll need a professional to handle the complex legal side of the transfer. Budget around $1,500 to $3,000 for their expertise.

- Building & Pest Inspections: Don’t even think about skipping this. For about $400 to $800, you get peace of mind and avoid buying a place with disastrous (and expensive) hidden problems.

- Lenders Mortgage Insurance (LMI): If your deposit is less than 20%, your lender will require LMI. It’s a one-off insurance premium that protects the bank, not you, and it can add thousands to your bill.

To give you a clearer picture, here’s a sample breakdown of these additional costs for a $700,000 property purchase in NSW for someone who isn't a first-home buyer.

Estimated Upfront Costs Beyond the Deposit

| Expense Category | Estimated Cost Range (AUD) |

|---|---|

| Stamp Duty | $25,875 |

| Mortgage Registration Fee | $165 |

| Transfer Fee | $165 |

| Legal/Conveyancing Fees | $1,500 – $3,000 |

| Building & Pest Inspection | $400 – $800 |

| Total Estimated Extra Costs | $28,105 – $30,005 |

As you can see, these expenses add up quickly and can significantly impact your overall budget if you haven't prepared for them.

Stamp duty is the real heavyweight here, often costing tens of thousands of dollars. It’s crucial to know exactly what you’re up for. The best way to do this is with a specialised stamp duty calculator for your state. Getting a precise figure early on is a non-negotiable step for any serious buyer.

By building these costs into your savings plan from the beginning, you can move toward settlement feeling confident and in control. A proper budget means no nasty surprises—just the pure excitement of finally getting your own set of keys.

Actionable Strategies to Grow Your Deposit Faster

Seeing that big target number on a calculator can feel a bit overwhelming, but speeding up your savings isn't about making massive sacrifices. It's about building smart, consistent habits that let your deposit grow almost on autopilot.

A brilliant first move is to open a dedicated high-interest savings account. Keep it completely separate from your daily transaction account. This creates a mental wall, making you think twice before dipping into your house fund for everyday spending.

With that account ready, set up an automatic transfer for the day you get paid. This simple "pay yourself first" trick is incredibly powerful. It prioritises your savings goal before you even have a chance to spend that money elsewhere.

Find Your Savings Superpowers

To really put your savings into high gear, you first need to know exactly where your money is going. This is where a spending audit comes in – and trust me, it’s a game-changer. For just one month, track every dollar you spend. The patterns you'll uncover can be genuinely surprising.

Look for the common culprits:

- Subscriptions: Be honest, are you still paying for a gym you never visit or streaming services you forgot you had? Axe them.

- Convenience Costs: That daily takeaway coffee or regular Uber Eats order adds up fast. A $5 coffee every workday is over $1,200 a year right there.

- Shopping Habits: Are impulse buys getting the better of you? Unsubscribe from those tempting marketing emails and remove the trigger.

Here's something many first-home buyers don't realise: lenders don't just look at your income. They scrutinise your spending habits to see if you can handle a mortgage. Proving you can manage your money and cut back on non-essentials now makes you look like a much better applicant later.

This process does more than just boost your savings; it can directly impact how much you can borrow. Lenders weigh your living expenses against benchmarks, so having lower declared expenses can often lead to a bigger loan approval. You can get a clearer picture of how your living costs affect your loan on homeloanexperts.com.au.

Answering Your Top Questions

Working out your home deposit can feel a bit like putting a puzzle together. There are lots of moving parts, and it’s natural to have questions. Let's tackle some of the most common ones that pop up when you're planning your savings journey.

Are These Online Calculators Actually Accurate?

The short answer is yes, for the most part. Deposit calculators are incredibly useful for mapping out a savings goal and timeline. They do a great job based on the figures you punch in, like how much you can save and when you want to buy.

Where you need to be careful is with the variable costs. Things like stamp duty and Lenders Mortgage Insurance (LMI) can change depending on the property and your specific situation, so the calculator can only give you a solid estimate.

Think of a deposit calculator as your trusted financial compass, not the final map. It points you in the right direction and gives you a fantastic starting point, but you'll always want to confirm the final numbers with your lender or conveyancer before you sign on the dotted line.

What's the Real Minimum Deposit I Need in Australia?

You’ll hear the magic number 20% thrown around a lot, and for good reason—it’s the threshold to avoid paying for LMI. But let's be realistic, that’s a huge hurdle for many first-home buyers.

The good news is that it's not the only way in. Most lenders in Australia will look at applications with a deposit as small as 5% of the property’s value. Plus, don't forget to look into government schemes, as some are designed to help eligible buyers get into the market with even less upfront.

Can I Put the First Home Owner Grant Towards My Deposit?

Absolutely. For most people, the First Home Owner Grant (FHOG) can be a massive help and can be used as part of your deposit. It’s a direct cash injection that goes straight towards those initial costs.

Just be sure to double-check the rules for your state or territory. It's also worth noting that some lenders might still want to see proof of "genuine savings"—that is, money you've consistently saved yourself over a period of time, on top of any grant money.

Will a Bigger Deposit Get Me a Better Interest Rate?

It certainly can. From a lender's perspective, a bigger deposit makes you a less risky borrower. If you can pull together a deposit of 20% or more, you're in a much stronger negotiating position.

Lenders often reward this by offering more competitive interest rates. It might not sound like much, but even a tiny reduction in your rate can save you tens of thousands of dollars over the life of a 30-year loan. It’s a powerful long-term saving strategy.

Planning your property journey in Mandurah or the surrounding suburbs requires expert local knowledge. For a free, no-obligation property appraisal and personalised advice, connect with David Beshay Real Estate. Get the clarity you need to make your next move at https://realestate-david-beshay.com.au.