At its heart, rental yield is a simple calculation: divide your annual rental income by the property's value, then multiply by 100 to get a percentage. This core formula is the single most important metric for understanding how well a property is performing as an investment.

What Rental Yield Reveals About Your Investment

Before you can really analyse an investment property, you need to understand what its rental yield is telling you. Think of it as the property's annual report card. It shows the income it generates relative to its market value, giving you a powerful way to compare different potential investments on a level playing field, rather than just looking at the weekly rent in isolation.

For any serious investor in Australia, calculating rental yield is a critical first step. Market dynamics can vary wildly from city to city. For instance, 2023 data showed median gross rental yields ranged from around 3.5% in Sydney to a much stronger 6.2% in places like Adelaide and Darwin. If you want to dive deeper, CoreLogic's detailed analysis offers some great insights into these trends.

Essentially, there are two crucial calculations every investor needs to get their head around:

- Gross Rental Yield: This is your quick, back-of-the-napkin calculation. It gives you a high-level snapshot of a property’s earning potential before factoring in any expenses. It’s perfect for doing initial comparisons when you're shortlisting properties.

- Net Rental Yield: This is the number that truly matters. It accounts for all the ongoing costs of owning the property, giving you a clear, honest picture of its actual profitability and what you’re left with at the end of the day.

Understanding both gross and net yield is non-negotiable. The gross figure helps you quickly filter opportunities, but it's the net yield that tells you the true financial story of your investment.

One gives you a quick snapshot, the other reveals the genuine financial health of your asset. Mastering both is key to making sharp, confident decisions that will actually help you hit your long-term investment goals.

In the next sections, we'll walk you through exactly how to work out both.

Getting a Quick Snapshot with Gross Rental Yield

When you’re first sizing up a potential investment, you need a quick and easy way to compare apples with apples. This is where Gross Rental Yield is your best friend. It’s a simple, high-level calculation that gives you an instant feel for a property's earning potential before you start digging into the nitty-gritty of running costs.

The formula itself is straightforward, giving you a crucial starting point for figuring out an investment's performance.

Gross Rental Yield Formula:

(Annual Rental Income / Property Value) x 100 = Gross Yield %

This calculation simply shows the total annual rent as a percentage of the property’s price tag. It’s the perfect tool for creating a shortlist and seeing which properties stand out.

Putting the Formula into Practice

Let's ground this with a real-world example. Say you've got your eye on a townhouse in a popular Mandurah suburb like Lakelands. The asking price is $550,000, and it's already tenanted at $600 per week.

First, we need to work out the total rent for the year. A common rookie mistake is just multiplying the weekly rent by 52, but it's the standard way to get a quick annual figure.

- Annual Rent Calculation: $600 (weekly rent) x 52 (weeks) = $31,200

With that number in hand, you can plug it straight into the gross yield formula. For a new purchase, the 'Property Value' is simply the price you're paying.

- Gross Yield Calculation: ($31,200 / $550,000) x 100 = 5.67%

So, this Mandurah townhouse has a gross rental yield of 5.67%. This single number is incredibly useful. It allows you to quickly stack this property up against others you might be considering.

But remember, this is just the first checkpoint. The gross yield paints a rosy picture because it doesn't factor in any of the real-world expenses that come with owning a property. It's an essential metric for your initial filtering, but it's only telling half the story.

Finding the True Return with Net Rental Yield

Gross yield gives you a quick snapshot, but it’s the net rental yield that tells the real story of your investment's health. This is the figure that actually hits your bank account because it paints a realistic picture of your property's performance after all the running costs have been paid. It’s the critical difference between what a property earns and what you genuinely keep.

To figure out your net yield, you need to be brutally honest and account for every single expense tied to holding that property. Skipping this step gives you a dangerously rosy view of your returns, which can lead to poor financial decisions down the road.

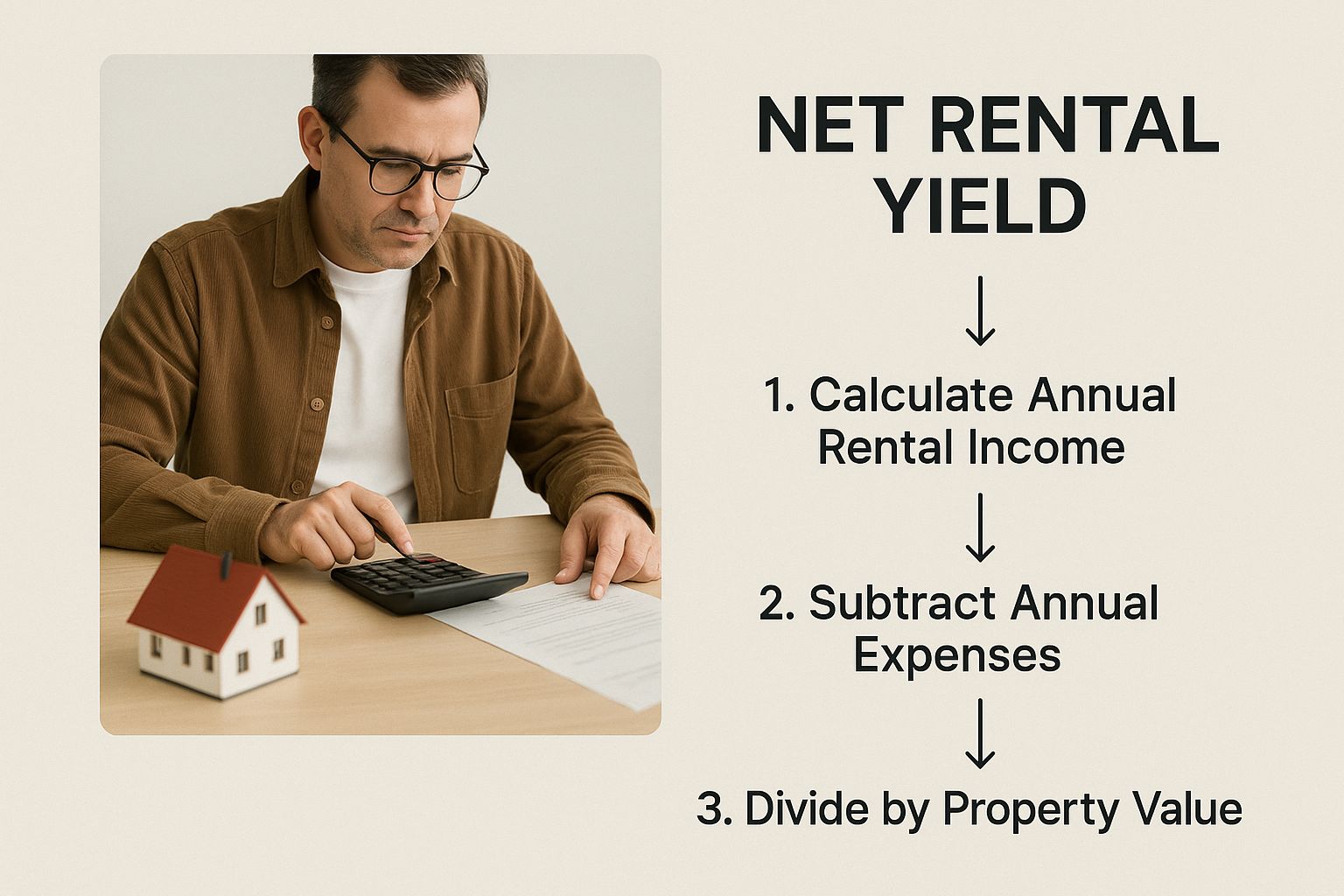

This image breaks down how you get from that top-line gross income to a clear, calculated net yield.

As you can see, the calculation drills down past the initial rent to factor in the unavoidable costs of being a landlord, revealing the true profit margin.

Identifying Your Annual Operating Costs

Before you can crunch the numbers, you need a complete list of your annual expenses. These are the costs that consistently chip away at your gross income all year long. Forgetting even one can throw your entire calculation off.

Here’s a practical checklist of the usual suspects to keep track of:

- Property Management Fees: Usually a percentage of the weekly rent, often landing between 7% and 10%.

- Council Rates: A quarterly bill that varies depending on your local council.

- Landlord Insurance: Absolutely essential. This protects you from tenant-related risks and property damage.

- Repairs and Maintenance: A savvy investor always has a fund for this. A good rule of thumb is to set aside 1-2% of the property’s value each year.

- Strata or Body Corporate Fees: If you own a townhouse or apartment, these fees cover the maintenance of common areas.

- Water Rates and Other Levies: Ongoing utility charges that are typically the landlord's responsibility.

By diligently tracking these expenses, you move from a speculative guess to a precise financial metric. The net yield is your proof of profitability, showing exactly what is left over after the property pays for itself.

The Net Rental Yield Formula in Action

The formula for net rental yield is pretty straightforward: it subtracts all those ongoing costs from your annual rental income before dividing by the property value. This gives you the actual return on your investment. You can discover more about this calculation's components and why it's so vital in financial analysis.

Let’s go back to our Mandurah townhouse example, which was bringing in a gross annual rent of $31,200. Now, let's plug in some realistic yearly expenses:

- Property Management (8%): $2,496

- Council & Water Rates: $3,000

- Insurance: $1,200

- Maintenance Fund: $2,500

- Total Annual Expenses: $9,196

First, we work out the net rental income by subtracting these costs from the gross rent.

- Net Income: $31,200 – $9,196 = $22,004

Now, we can use this net figure to calculate the final yield.

- Net Yield Calculation: ($22,004 / $550,000) x 100 = 4.0%

All of a sudden, that appealing 5.67% gross yield has dropped to a much more realistic 4.0%. This highlights precisely why understanding your net yield isn't just a "nice-to-know"—it's non-negotiable for making smart, sustainable investment decisions.

To make this crystal clear, here’s a side-by-side comparison of the two calculations for the same Mandurah property.

Gross vs. Net Rental Yield Example Calculation

| Metric | Gross Yield Calculation | Net Yield Calculation |

|---|---|---|

| Purchase Price | $550,000 | $550,000 |

| Weekly Rent | $600 | $600 |

| Annual Rental Income | $31,200 | $31,200 |

| Total Annual Expenses | $0 (Not included) | $9,196 |

| Net Annual Income | $31,200 | $22,004 |

| Formula | (Annual Income / Price) x 100 | (Net Income / Price) x 100 |

| Final Yield | 5.67% | 4.0% |

As the table shows, ignoring expenses inflates the return by over 1.6%. While gross yield is a useful starting point for comparing properties quickly, the net yield is the number that truly reflects the investment's performance and what you can expect to pocket.

What’s a Good Rental Yield in Australia, Anyway?

Once you’ve crunched the numbers, the big question always pops up: is my rental yield actually any good?

Honestly, there’s no single magic number that screams "success." A good yield really depends on your personal strategy, the type of property you own, and most importantly, where it’s located.

An investor chasing strong capital growth in a blue-chip Sydney or Melbourne suburb might be thrilled with a net yield of 2.5% to 3.5%. Their game plan isn’t about immediate cash flow; it’s about the property's value soaring over time. On the flip side, someone focused on positive cash flow in a regional hub would be aiming much higher, often looking for 5% or more.

It All Comes Down to Location

Different markets deliver different results. It’s pretty common to see lower yields in high-demand capital cities simply because the entry prices are so steep. Regional areas, on the other hand, can often serve up much more attractive rental returns.

A strong rental yield in one market could be considered just average in another. Context is everything. Always measure your property’s performance against local benchmarks, not some generic national average.

The Mandurah property market is a perfect example of how regional hubs can shine. As of late 2023, the median gross rental yield for houses was hovering around 5.0%, with units pushing up to about 5.5%. These figures look especially robust when you compare them to Perth's overall median of 4.7% for houses. You can dig into more of these local trends in REIWA’s quarterly market updates.

Does the Yield Match Your Goals?

At the end of the day, a good yield is one that fits your financial goals like a glove.

- Going for Cash Flow? If you’re trying to generate passive income right now, you’ll need a higher net yield that covers all your expenses and still leaves a profit in your pocket each month.

- Playing the Long Game? If your strategy is all about growth, a lower yield might be perfectly fine, as long as the location has solid potential for capital growth. This is a common approach in many parts of the Perth metro area. Understanding how Perth's housing market continues its upward climb gives you some crucial context for this kind of strategy.

Before you even think about investing, get clear on your primary goal. That clarity will tell you whether a 4% yield is a fantastic result or a signal to keep looking.

Practical Ways to Increase Your Rental Yield

Once you've got your head around the rental yield calculation, the next logical step is figuring out how to improve it. This is where you shift from just running the numbers to taking action, and it's how you turn a decent investment into a great one.

Boosting your property’s performance doesn't always mean a massive, expensive overhaul. Often, it’s a game of smart adjustments and strategic upgrades that make a real difference.

Seasoned investors know that improving yield is a two-sided coin. You can either increase the rental income coming in or decrease the operational expenses going out. The sweet spot, of course, is doing a bit of both. Every small improvement you make adds directly to a healthier bottom line.

Drive Up Your Rental Income

The most direct way to bump up your yield is to make your property more appealing to quality tenants who are willing to pay a premium. This means putting your money into upgrades that give you the biggest bang for your buck.

Minor cosmetic renovations are often the key. A survey from the Property Investment Professionals of Australia (PIPA) found that investors who modernise fixtures and slap on a fresh coat of paint can increase their rental income by an average of 10-15%. It's well worth having a look at PIPA's investment insights to see how small changes can deliver big results.

Here are a few high-impact, low-cost upgrades I've seen work time and again:

- A Kitchen Refresh: You don't need to rip everything out. Something as simple as replacing old benchtops, painting the cabinet doors, and installing a new splashback can completely transform the feel of the space.

- Modern Fixtures: Swapping out dated taps, light fittings, and door handles is a quick win. It’s a small detail that instantly makes a property feel more contemporary and cared for.

- Add Air Conditioning: In a climate like Mandurah's, a split-system air conditioner isn't just a luxury; it's a massive drawcard. It can justify a significant rent increase and seriously cut down your vacancy periods.

Reduce Your Ongoing Expenses

Just as important is getting a tight grip on your expenses. Every dollar you save on running costs is a dollar that goes straight into your pocket as net yield.

Proactively managing your expenses is just as powerful as increasing rent. It gives you more control over your net return and protects your cash flow from unexpected hits.

Start by going through your regular outgoings with a fine-tooth comb. Are you getting the best deal on your landlord insurance? Could you have a chat with your property manager about their fees? Even small savings here add up significantly over the course of a year.

On top of that, setting up a preventative maintenance schedule can save you a fortune on expensive emergency repairs down the track. Fixing a small roof leak now is far cheaper than dealing with major water damage later.

Cutting down your expenses not only improves your yield but can also have positive tax implications. It’s smart to explore all your options to understand your full financial position, which is something we cover in our guide on investment property tax benefits.

Common Questions About Calculating Rental Yield

When you start digging into rental yields, a few questions always seem to come up. It's totally normal. Getting the details right is what separates a good paper-based investment from a great real-world one.

Let's clear up some of the most common sticking points investors run into.

Purchase Price or Current Market Value?

One of the biggest hurdles is deciding which property value to use in the formula. Should it be what you paid for it, or what it's worth today?

Honestly, the answer depends on what you're trying to figure out.

- Use the original purchase price (plus your buying costs like stamp duty) when you want to see the total return on your investment since day one. It tells you the full story of its performance over time.

- Use the current market value to get a real-time snapshot of how that asset is performing right now. This is crucial for deciding if your capital is working as hard as it could be, or if it might be better off somewhere else.

Should I Factor in Vacancy Periods?

Absolutely. Forgetting to account for vacancy is a classic rookie mistake that can make your numbers look much better than they really are. It’s just not realistic to assume your property will have a tenant for all 52 weeks of the year.

A smart, conservative approach is to build a buffer into your calculations. I always recommend deducting two to four weeks of rent from your total annual income.

So, for a property bringing in $600 per week, that means subtracting between $1,200 and $2,400 from your yearly total. It’s a simple step that gives you a much more accurate net yield.

What happens when your costs are higher than your income? This is a common scenario for investors focused on capital growth. When your total annual expenses exceed your rental income, you have a negative net rental yield.

This situation is the very definition of a 'negatively geared' property. Investors in this position aren't making a monthly profit from rent. Instead, they are banking on the property's value increasing over time (capital growth) to deliver a strong overall return when they eventually sell. If you want to learn more, you can read our detailed guide explaining what negative gearing is and how it works as an investment strategy.

The Hidden Costs That Can Sink Your Yield

Beyond the obvious mortgage repayments, plenty of smaller, recurring costs can quietly eat away at your profit margin. It's easy to overlook them, but they add up.

Make sure you've included these often-missed expenses in your calculation:

- Landlord insurance

- Body corporate or strata fees (for apartments and townhouses)

- Council and water rates

- A dedicated budget for both routine and unexpected maintenance

Forgetting these will make a property look far more profitable on paper than it actually is. Getting granular with these costs is the key to a truly accurate rental yield figure.