A Comparative Market Analysis (CMA) is the report a real estate agent prepares to figure out the current market value of your property. It’s all about comparing your home to similar ones that have recently sold nearby, which helps set a listing price that’s both competitive and realistic.

Understanding What a Comparative Market Analysis Is

Think about pricing a vintage car. You wouldn't just guess a number; you’d look up what similar models in the same condition have sold for recently. A Comparative Market Analysis, or CMA for short, does exactly that for your home. It's a professional assessment, but it’s important to remember it's not the same as a formal valuation done for a bank.

A CMA is really a strategic pricing tool. It's built on a fundamental real estate idea called the principle of substitution. Basically, this means a savvy buyer won’t pay more for your property than what a similar, recently sold home in the same area went for. By digging into these "comparable" properties (we call them "comps"), an agent can pinpoint a data-backed price range for your home.

This analysis is incredibly useful, whether you’re buying or selling.

- For Sellers: It’s the bedrock for setting a sharp listing price that pulls in serious buyers and gets your home sold faster.

- For Buyers: It gives you the confidence to put in a strong, informed offer, making sure you don’t overpay in a hot market like Mandurah.

The Core Components of a CMA

At its heart, a CMA tells a story with data. A good agent knows how to weave together different pieces of information to create a clear picture of where your property sits in today’s market. While every report looks a bit different, they all share the same basic building blocks. Getting to know these elements is the first step in understanding how an agent lands on that final price recommendation.

A well-researched CMA is more than just an estimate; it's a strategic roadmap. It helps ground an emotional decision in objective facts, leading to better financial outcomes whether you are selling or buying.

Here’s a quick look at the essential ingredients an agent like David Beshay uses to build an accurate and reliable CMA. Each one is a vital piece of the puzzle, and together, they form a solid case for your home's true value.

The Core Components of a CMA at a Glance

| Component | What It Is | Why It Matters for an Accurate Valuation |

|---|---|---|

| Subject Property Details | All the specifics of your home: address, size, beds, baths, age, features, and condition. | This is the baseline. The more accurate and detailed this information is, the better the final comparison will be. |

| Comparable Sold Properties ("Comps") | Recently sold properties (usually within the last 3-6 months) that are as similar to yours as possible. | This is the most crucial part. It shows what buyers have actually been willing to pay for homes like yours right now. |

| Comparable Active Listings | Homes currently for sale that are similar to yours. | This shows your direct competition. Knowing their asking prices helps position your home to attract the most attention. |

| Comparable Expired Listings | Nearby homes that were listed but failed to sell. | These are cautionary tales. They often indicate a pricing problem and help us avoid setting a price that's too high for the market. |

| Local Market Adjustments | Nuanced changes for differences between your home and the comps (e.g., a renovated kitchen, an extra garage). | No two homes are identical. These adjustments fine-tune the valuation to reflect the unique value of your property's features. |

| Market Conditions Summary | An overview of the current real estate climate: Is it a buyer's or seller's market? Are prices rising or falling? | Context is everything. A home's value is directly tied to the health of the local market at that specific moment in time. |

This framework is the foundation of a solid CMA and sets the stage for a deeper dive into the methodology, which we'll explore next.

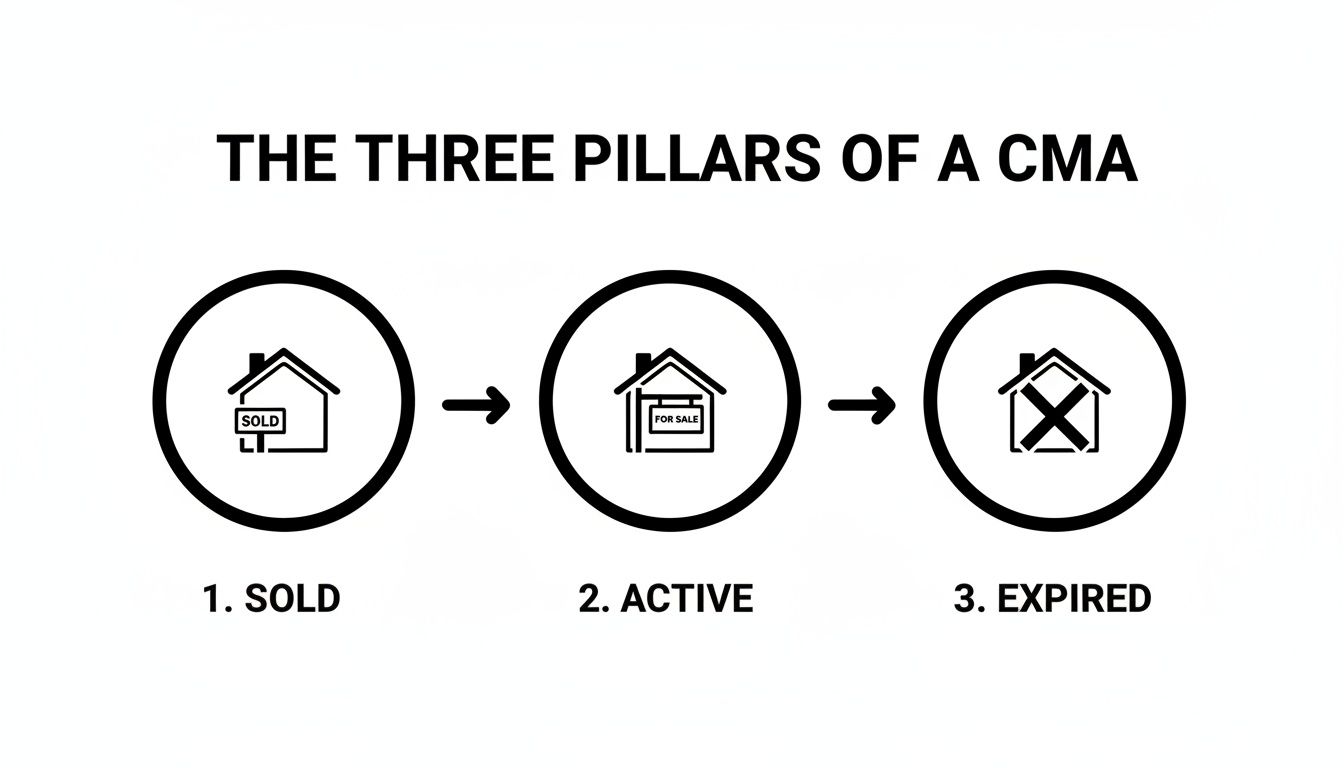

The Three Pillars of a Spot-On CMA Report

To really get what a comparative market analysis tells you about your property's value, picture a three-legged stool. For it to be stable and reliable, all three legs have to be there. Each leg is a different type of property data, and a good agent doesn’t just glance at one—they pull together information from sold, active, and expired listings to paint the full picture of the current market.

This balanced approach grounds the final pricing strategy in reality. It’s not just about past successes; it’s also about today’s competition and what the market has already rejected. By looking at all three pillars together, we move from a rough guess to a solid, well-supported conclusion about what your home is actually worth.

Pillar 1: Recently Sold Properties

The first and most critical pillar is recently sold comparable properties, or "comps" as we call them in the business. This is the bedrock of any accurate CMA because it’s based on hard facts—what a real buyer was willing to pay for a home like yours, in your area, just recently.

This isn't guesswork; it's solid proof of market value. As digital property databases became the norm in Australia, agents gained the power to access detailed sales records, making the CMA a standard tool. Today, a solid CMA leans on 3 to 6 recent comparable sales to establish a strong pricing baseline. You can dig deeper into Australia's property price history over at globalpropertyguide.com.

When picking these comps, an agent is looking for properties that are as close a match to yours as possible:

- Location: Ideally in the same Mandurah suburb, or even better, on the same street.

- Size: Similar land size and internal living space.

- Features: The same number of bedrooms, bathrooms, and car spaces.

- Age and Condition: Built around the same time and in a similar state of repair.

By zeroing in on properties sold within the last 3 to 6 months, we make sure the data is fresh and reflects what’s happening in the market now, not a year ago.

Pillar 2: Active Listings

Sold properties tell us what happened yesterday, but active listings tell us what’s happening today. These are the homes currently for sale in your neighbourhood—your direct competition. Sizing them up is key to positioning your home to stand out.

Looking at active listings helps answer some big questions. How are similar homes priced right now? What features are they shouting about? And how long have they been sitting on the market? If a house down the road has been for sale for 60 days, it’s a good sign it’s overpriced—a valuable lesson for us.

On the flip side, if well-priced homes are going under offer in a week, that’s a clear signal of strong buyer demand. This pillar gives us that real-time context, helping us fine-tune your price to grab the attention of serious buyers straight away, instead of getting lost in the noise.

Pillar 3: Expired and Withdrawn Listings

The third pillar is one that sellers often overlook: expired or withdrawn listings. Think of these as market rejections. These are the properties that went up for sale but didn’t find a buyer, and nine times out of ten, the reason comes down to one thing: price.

These listings are cautionary tales. They show us the ceiling of what buyers in the area are willing to pay. If a home very similar to yours was listed at $650,000 and sat there for three months with no takers, it’s a massive red flag that starting at that price would be a mistake.

By studying what didn’t work for others, we can avoid making the same blunders. This data helps us set a realistic upper limit for your property's value and avoid the costly mistake of overpricing, which can lead to your home going stale on the market and ultimately selling for less than it should have. Together, these three pillars—sold, active, and expired—create a powerful, data-driven foundation for finding the true market value of your home.

How a Professional CMA Is Actually Built

Let's pull back the curtain and show you how a real comparative market analysis comes together. It’s a detailed process that combines hard data with the kind of local knowledge you can only get from being on the ground, day in and day out. This is a far cry from just plugging an address into a website.

It all starts with a walkthrough of your property. This first step is absolutely vital. An agent needs to see your home through a buyer's eyes, taking in its unique features, its current condition, and all the upgrades you’ve poured your time and money into. A new kitchen, that beautifully landscaped backyard, or even just the overall upkeep can make a huge difference to the final price.

Gathering the Raw Data

Once we have a solid feel for your property, the deep dive into the data begins. We use powerful, agent-only databases like CoreLogic to access hyperlocal information that simply isn't available to the public. This gives us the most accurate, up-to-the-minute picture of sales, active listings, and market history right here in your specific Mandurah suburb.

Our goal is to find at least three to four genuinely comparable properties that have sold in the last 90 days. These "comps" are the bedrock of the entire analysis.

- Proximity is key: We start on your street and work our way outwards, keeping it as local as possible.

- Property specifics matter: We’re filtering for homes with a similar land size, the same number of bedrooms and bathrooms, and a comparable floor plan.

- Age and style are considered: A classic 1980s brick-and-tile home is only ever compared to similar builds, not a brand-new contemporary masterpiece.

The diagram below breaks down how we look at the three key pillars of the market—sold, active, and expired listings—to build a complete picture.

This method shows us what prices the market has recently paid (sold), what your direct competition looks like right now (active), and which price points buyers have already rejected (expired).

The Art of Adjustments

This is where experience really shines. No two homes are ever identical, so the next step is to make financial adjustments to account for the differences between your place and the comps. It's a careful process of adding or subtracting value based on specific features.

For instance, let's say a comparable home down the road sold for $650,000, but it had an original, dated kitchen. If you renovated yours last year, we would make a positive adjustment to your property's estimated value to reflect that upgrade—maybe adding $15,000 – $20,000.

On the flip side, if a comp is tucked away on a quiet cul-de-sac and your home backs onto a busier road, a negative adjustment is needed to account for the difference in location. It’s this detailed, methodical process that transforms raw data into a truly refined and accurate price range.

Finalising the Pricing Strategy

The analysis doesn't stop with sold properties. We then layer in what we’ve learned from your direct competition (the active listings) and the market rejections (the expired ones). This adds crucial context, telling us exactly what buyers in the Mandurah market expect and what they aren't willing to pay. To get a better sense of how this differs from a bank's formal valuation, you can learn more about what a property appraisal involves.

A professional CMA is not just a report; it's a pricing strategy. It combines historical sales data, current market competition, and nuanced adjustments to position your home to attract the strongest possible offers in the shortest amount of time.

CMA vs Formal Valuation: What's the Difference?

Many homeowners toss around the terms "market analysis" and "valuation" as if they’re the same thing. It’s a common mix-up, but in the world of real estate, they are two very different beasts. Getting this distinction right is crucial, as each serves a unique purpose at different points in your property journey.

Think of it this way: a Comparative Market Analysis (CMA) is fundamentally a marketing and sales tool. When a real estate agent like myself puts one together, the main goal is to nail down a competitive listing price. We do this by digging into what buyers are doing right now and what the local market is telling us. It’s all about looking forward and answering one key question: "What is a buyer realistically going to pay for this home today?"

A formal valuation, on the other hand, is a legally recognised report cooked up by a licensed valuer, usually for a bank or lender. Its job is completely different—it’s about assessing risk for mortgage lending. This fundamental difference in purpose changes everything about the approach.

Purpose and Perspective

The real split between a CMA and a formal valuation comes down to who it’s for and why it’s being created. An agent prepares a CMA for you, the seller. The aim is to craft a pricing strategy that will pull in the right buyers and land you the best possible sale price. The perspective is optimistic but grounded in reality, focusing on market momentum and the property's potential.

A formal valuation is built for a lender. The valuer's primary responsibility is to protect the bank's investment, which naturally makes their approach more conservative and risk-averse. They’re focused on providing a "safe" value—a figure that ensures the bank can recover its loan if the worst happens and the borrower defaults. You can dive deeper into this in our guide on the difference between bank evaluations and real estate agent appraisals.

Methodology and Legal Standing

The methods used are also worlds apart. While both a CMA and a formal valuation look at comparable sales, a valuer must follow strict, regulated guidelines. They often use more complex models and are required to provide a definitive, single-figure value. This valuation carries legal weight and is used for official business like mortgage applications, refinancing, or legal settlements.

A CMA is not a legally binding document. It’s an informed, expert opinion of value, usually presented as a price range to guide your strategy. Here in Australia, CMAs are incredibly powerful tools for agents setting listing prices and for both sellers and buyers during negotiations. Even though they aren't crystal balls, their reliance on fresh, local sales makes them highly effective for gauging short-term price signals.

A formal valuation looks backward at historical data to establish a conservative, defensible value for a lender. A CMA looks forward, using current market activity to create a strategic sale price for a seller.

To make it even clearer, here’s a quick breakdown of the key differences:

Comparative Market Analysis (CMA) vs Formal Property Valuation

| Feature | Comparative Market Analysis (CMA) | Formal Valuation |

|---|---|---|

| Prepared By | Licensed Real Estate Agent | Licensed and Registered Valuer |

| Primary Purpose | To determine a competitive listing price for selling | To assess risk for lending, legal, or financial purposes |

| Audience | Property sellers (and sometimes buyers) | Banks, lenders, courts, government bodies |

| Perspective | Marketing-focused, optimistic yet realistic | Conservative, risk-averse |

| Output | A suggested price range (e.g., $750,000 – $780,000) | A single, definitive dollar value |

| Legal Status | An informed opinion, not legally binding | A legally recognised and defensible report |

| Cost | Usually free, provided by an agent | Costs money (typically $500 – $800+) |

| When to Use | When thinking of selling or buying a property | When applying for a mortgage, refinancing, or for legal matters |

Ultimately, a CMA is a free, strategic tool designed to help you navigate the sales process successfully. A formal valuation, however, comes with a price tag because it provides a legally recognised figure required for official financial transactions. Knowing which one you need—and when—is key to making smart property decisions.

Putting Your CMA to Work as a Seller or Buyer

A well-researched comparative market analysis is so much more than just a number on a page; it’s a strategic tool that empowers everyone involved in a property deal. Whether you're selling your beloved family home, buying for the first time, or scouting for an investment, a CMA gives you the objective data you need to make confident financial decisions.

It grounds the entire transaction in reality, pushing guesswork and emotion aside in favour of cold, hard facts about what's really happening in the local market.

How Sellers Can Use a CMA

For homeowners looking to sell, the CMA is the absolute foundation of a successful sales campaign. Its most important job is to help you set a competitive and realistic listing price right from the get-go. Nailing the price is arguably the single most critical step in the selling process.

- Attract Serious Buyers: A price backed by solid data pulls in qualified buyers who know fair market value when they see it. This means more feet through the door and stronger offers.

- Avoid Market Stagnation: Overpricing is a classic mistake that leaves a property sitting on the market for too long, eventually becoming "stale" in buyers' eyes. A proper CMA helps you dodge this bullet.

- Negotiate from a Position of Strength: When an offer lands on the table, your CMA is your proof. It lets you negotiate with confidence, knowing exactly what your property is worth based on proven sales data.

At the end of the day, a sharp pricing strategy informed by a great CMA can mean a faster sale and a better final price. Your agent's expertise is crucial here; if you need some pointers on how to choose a real estate agent who can put together a masterful CMA, we have a guide that can help.

Gaining an Edge as a Buyer

It's not just sellers who benefit. Buyers can gain a huge advantage by using a comparative market analysis, too. In a competitive area like Mandurah, it's easy to get swept up in the emotion of finding the perfect home and end up overpaying.

Think of a CMA as your logical anchor. By looking at recent sales of similar properties, you can figure out if a home's asking price is actually fair. This knowledge gives you the confidence to put in a strong, data-backed offer that a seller is far more likely to take seriously.

For buyers, a CMA transforms an emotional decision into a calculated one. It provides the leverage to make a fair offer and ensures you don't pay more than the market dictates, protecting your financial future.

This analysis is also priceless for investors. The savviest property investors lean heavily on CMAs to spot undervalued assets, project potential rental yields, and calculate a property's future value after a bit of work. It’s a non-negotiable tool for maximising your return on investment.

Of course, here is the rewritten section with a more natural, human-expert tone, following the provided examples and requirements.

What a CMA Can't Tell You: Understanding Its Limitations

A comparative market analysis is an absolutely essential tool, but it's important to have a clear-eyed view of what it can and can't do. A CMA isn't a crystal ball; think of it more as a high-resolution snapshot of the market on the day it was taken. Its accuracy hinges entirely on two things: the quality of the data available and the agent's skill in piecing that puzzle together.

This means every CMA has its limits. In certain market conditions or for truly one-of-a-kind homes, its effectiveness can be put to the test. Knowing where these boundaries lie helps manage expectations and highlights why an agent's real-world expertise is so critical.

When the Data Gets Murky

The whole strength of a CMA rests on finding solid, comparable properties. But what happens when good "comps" are few and far between? This is a common hurdle that can really impact the final price estimate.

- For unique homes: If your property has distinctive architecture, sits on an unusually large block for the area, or boasts high-end features you just don't see in your part of Mandurah, finding truly similar sold homes is a real challenge. The fewer the comps, the more interpretation and experience are needed to bridge the gaps.

- In slow markets: When properties aren't selling quickly, an agent might have to look back further than the ideal 3-6 month window. The problem is, that older data might not capture how buyers are feeling right now.

A CMA's value can also fade fast in a rapidly changing market. If Mandurah prices are jumping or dipping week by week, a report that's only a month old could already be out of date. It captures a moment, not the momentum.

A CMA delivers an expert opinion of value, presented as a price range, not a single, unmovable number. That range is there for a reason—it accounts for market quirks, buyer emotions, and data gaps that raw numbers alone just can't express.

The Human Element is Non-Negotiable

At the end of the day, a CMA is only as good as the agent who puts it together. A database can't tell you that one street has a better reputation than the one next to it, or that the new cafe opening on the corner is suddenly making the neighbourhood more desirable. This is where an agent’s "boots on the ground" knowledge is priceless for reading between the lines of the data.

This professional judgment is also why transparency is so important. It's not uncommon for a CMA estimate and a formal bank valuation to differ, sometimes by 5–10%, especially when the market is volatile. As many professional reports show, these gaps can widen during periods of rapid price shifts. This reinforces why a CMA is always an indicative range, backed by solid data and, most importantly, local context. For a broader look at market trends, you can explore insights into the Australian real estate market at imarcgroup.com.

Got Questions About Comparative Market Analysis? We’ve Got Answers.

Even after you've got your head around the basics, it's completely normal to have a few lingering questions. Let's tackle some of the most common queries we hear from homeowners and buyers right here in Mandurah, so you can feel completely confident about the process.

How Much Does a Comparative Market Analysis Cost?

Nothing at all. A CMA from a real estate agent is a complimentary service. We offer them to show you our expertise in the local market and start building a relationship, hoping we can earn your business when you're ready to sell.

This is a big point of difference from a formal bank valuation, which is carried out by a licensed valuer for a fee that usually runs into several hundred dollars.

How Long Does It Take to Prepare a CMA?

A truly thorough and accurate CMA usually takes about 24 to 48 hours to put together. The process isn't just a quick search online; it involves an on-site visit to your property, a deep dive into comparable sales data, analysing current market trends, and then compiling everything into a clear, final report.

An experienced agent dedicates focused time to this, making sure the right comparable properties are chosen and analysed properly. That's how we ensure the final price estimate is as reliable as it can possibly be.

A professional CMA isn't an instant online guess. It’s a detailed analysis that needs careful data gathering and expert interpretation to give you a true picture of your property's value in today's market.

How Accurate Is a CMA and Can I Rely on It?

A well-prepared CMA from an experienced local agent is a highly reliable estimate of what your property is worth right now. Its accuracy really comes down to two things: the quality of the recent sales data we can find and the agent's skill in making logical adjustments for any differences between properties.

While it’s not a legally binding appraisal, it is the industry-standard tool used by professionals to set a strategic listing price and guide negotiations. Think of it as a solid, data-backed foundation for your next move.

Should I Get a CMA If I Am Not Ready to Sell?

Absolutely. It’s a smart move to request a CMA even if you're just curious about your property's value or thinking about selling in a year or two. It helps you stay informed about your most significant financial asset and gives you a real feel for how the local market is behaving.

This knowledge can be incredibly valuable for your broader financial planning, especially when you're considering future renovations or looking at your refinancing options. Keeping up-to-date with your property's value is always a wise move.

Ready to discover what your Mandurah property is truly worth? David Beshay Real Estate offers a completely free, no-obligation property appraisal that gives you the clarity and confidence you need. Request your complimentary property appraisal today!