A property appraisal is a professional and impartial assessment of your home's market value. It’s not just an educated guess; it’s a detailed report prepared by a qualified valuer, designed to provide a precise, evidence-based figure for financial and legal purposes.

What a Property Appraisal Really Means

Think of a property appraisal as a thorough financial health check for your home. It's often confused with a real estate agent's price estimate, but they serve very different purposes. An agent's opinion is a marketing tool, but an official appraisal is an objective analysis conducted by an independent, certified valuer. This distinction is critical when major financial decisions are on the line.

The valuer’s job is to deliver an unbiased opinion of value, which is precisely why lenders rely on these reports. They conduct a deep-dive analysis, combining an on-site inspection with meticulous research into market data. Their final figure isn't just a suggestion—it's a legally defensible valuation that forms the bedrock of transactions like securing a mortgage or refinancing an existing loan.

The Purpose Behind the Process

At its core, what is a property appraisal if not a tool for managing risk? For lenders, it confirms that the property is sufficient collateral for the loan amount. For buyers and sellers, it provides a transparent, data-driven value that everyone can trust.

The importance of this process grows with the market's complexity. For instance, with national home prices hitting new records and seeing an annual increase of 4.12%, an accurate appraisal is more critical than ever to ensure all parties are making sound financial choices. You can explore more data on Australian home price trends to see why this matters.

This independent valuation serves several key purposes:

- Securing a mortgage: Lenders almost always require an appraisal to approve a home loan.

- Refinancing: An updated appraisal is needed to determine your home’s current equity.

- Setting a sale price: It gives sellers a realistic and defensible starting point for negotiations.

- Property settlements: It ensures a fair division of assets during a divorce or inheritance.

An appraisal provides a clear, impartial snapshot of value at a specific moment in time. It removes guesswork and emotion, replacing them with verifiable facts and market analysis to protect everyone involved in a property transaction.

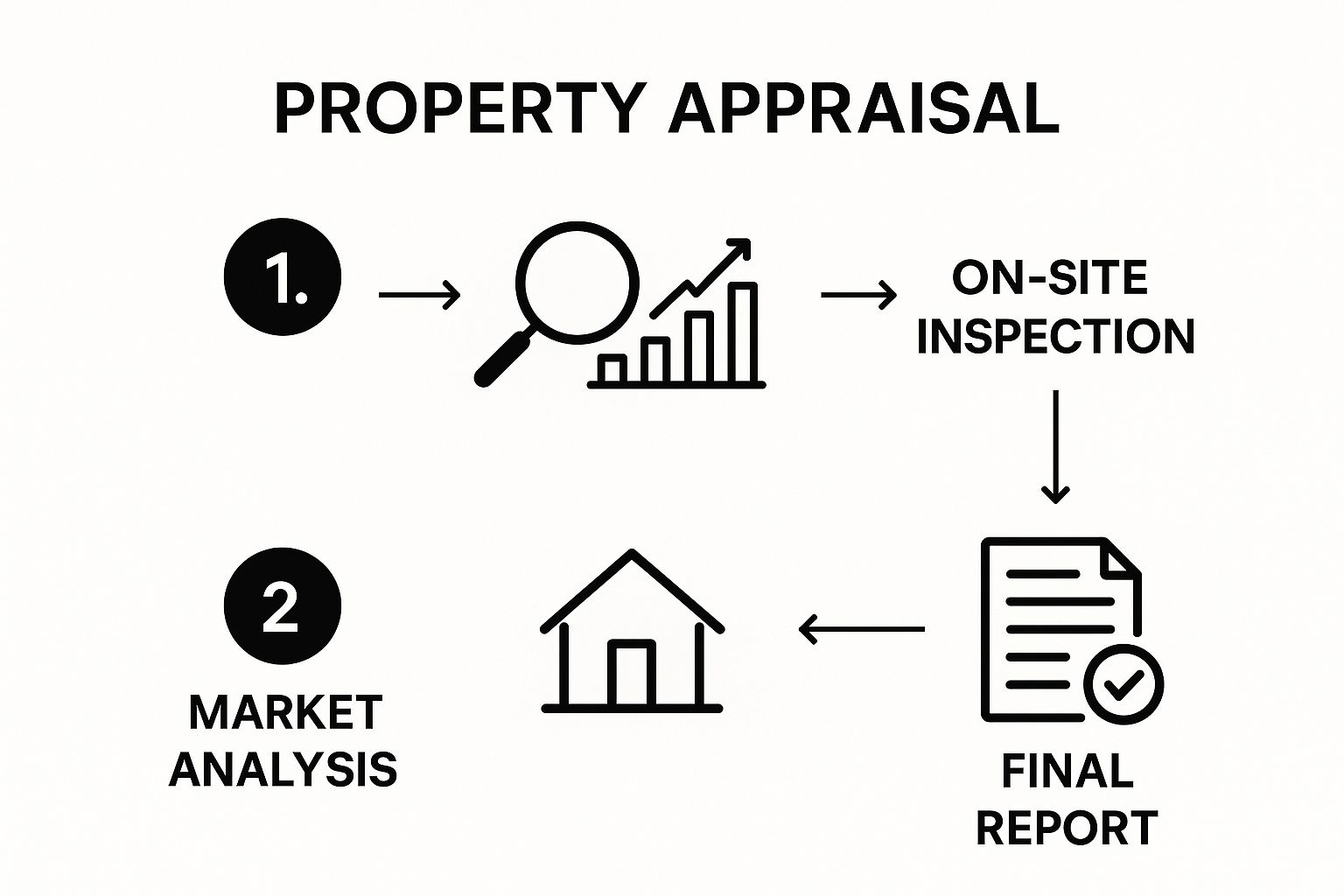

The Property Appraisal Process Unpacked Step-by-Step

Understanding how a property appraisal actually works can take a lot of the mystery out of a real estate deal. It's far more than just a quick look-around; it’s a structured, methodical process that starts with deep research and ends with a comprehensive report. When you know what goes on behind the scenes, you can really appreciate the level of detail involved.

The whole thing kicks off the moment an appraisal is ordered, whether by a lender, a buyer, or a homeowner. The valuer doesn’t just show up at your front door unannounced. Their work starts with crucial off-site research, digging into property records, checking zoning information, and analysing recent market activity in your suburb. This builds a solid foundation before they even set foot on the property.

The On-Site Inspection and Analysis

Next up is the on-site inspection, which is the part most people are familiar with. Here, the valuer will meticulously measure the home, sketch its layout, and document all its features. They're assessing the property's overall condition, the quality of its construction, and the state of any fixtures and fittings—from the kitchen benchtops right down to the landscaping, sheds, and pools outside.

After the physical visit, the valuer moves on to the analysis. This is where they perform what’s known as a comparative market analysis, but with much more rigour than a real estate agent’s opinion. They pinpoint and scrutinise comparable sales (or ‘comps’)—these are recently sold properties that are as similar to yours as possible in location, size, age, and condition.

The flow from the hands-on inspection to the final report is really a structured journey, as this infographic shows.

It’s this combination of physical inspection and hard data that produces a valuation you can stand by.

Finalising the Valuation Report

The last step is to bring all of this information together into a detailed report. The valuer reconciles all the data, making adjustments to the prices of the comparable properties to account for any differences. For instance, if a 'comp' home has a newly renovated kitchen and yours doesn't, a value adjustment will be made to level the playing field.

Think of a property appraisal as a story told with data. The on-site inspection introduces the main character (your home), while the market analysis provides the setting and context. Together, they create a logical and evidence-based conclusion about its value.

This final, comprehensive document details the property’s characteristics, current market conditions, the valuation method used, and of course, the final estimated market value. It's this thorough, step-by-step process that makes an official appraisal the gold standard for financial institutions.

Key Factors That Actually Influence Your Property's Value

While everyone knows the old mantra "location, location, location," a professional property appraisal goes much, much deeper. Think of a certified valuer as a property detective. They piece together dozens of clues about your property to arrive at an objective, evidence-based conclusion on what it’s really worth.

This investigation scrutinises both the physical aspects of your home and the external market forces shaping its value. It’s a methodical process that looks past simple aesthetics, assessing everything from the fundamental land size and building age to its structural integrity. The functional layout, number of bedrooms and bathrooms, and the quality of any recent renovations are all meticulously documented and stacked up against current market standards.

Core Property Attributes

A valuer starts by getting up close and personal with the tangible features that define your property. These are the elements you have the most direct control over and they form the foundation of the initial assessment.

- Size and Layout: This isn't just about the total land area, but also the home's liveable square meterage. A practical, flowing floor plan is often valued more highly than a larger but poorly designed space.

- Age and Condition: The overall state of the property is critical. A valuer takes note of everything from the roof's condition and the foundation's stability to the quality of interior fixtures and fittings.

- Rooms and Features: The number of bedrooms and bathrooms is a primary value driver. On top of that, extras like a double garage, a swimming pool, or a modern, well-appointed kitchen can add significant value.

- Recent Renovations: Quality upgrades, especially in kitchens and bathrooms, can definitely have a positive impact. It’s crucial, however, that any major extensions have the proper council approvals to be fully recognised.

External Market and Location Factors

Beyond your fence line, a whole range of external factors can dramatically influence the final figure. These elements are often tied to the health of the broader real estate market, which is an immense force. To give you an idea of the scale, the total value of Australian residential dwellings recently grew to a staggering $11.3664 trillion, with the national mean dwelling price now sitting at $1,002,500.

A property's value is a blend of its physical self and its place in the community. A great house in a poor location will be valued differently than a modest house in a prime spot.

Other key external drivers include local council zoning, which dictates what can be built nearby, and proximity to desirable amenities like schools, parks, public transport, and shopping centres. While a formal valuer provides a specific type of assessment, it’s also helpful to understand the difference between bank evaluations and agent appraisals to get a complete picture of where your property stands in the market.

An appraisal isn't just another box to tick in the property transaction process. Think of it as a crucial financial shield that protects everyone involved. It cuts through the emotion and guesswork, establishing a fair and independent value for a property. This impartial number becomes the solid ground on which confident negotiations are built.

How It Protects Home Sellers

If you're selling your home, an appraisal gives you a realistic and defensible price target. It's one thing to have an asking price; it's another to have it backed by a formal valuation. This instantly strengthens your negotiating position and helps you sidestep the classic blunders of pricing your home too high or, even worse, too low. A home priced accurately from the start is far more likely to attract serious buyers and sell without unnecessary delays.

Think of an appraisal as a financial safety net. It ensures the price everyone agrees on is actually validated by the market. This protects the buyer from overpaying and, just as importantly, stops the seller from undervaluing what is likely their biggest asset.

The Security It Offers Home Buyers

For anyone buying a home, the appraisal is an absolutely essential safeguard. It provides independent confirmation that the price you've agreed to pay is supported by the property's real market value. This is vital for your lender, too. It gives them the confidence that their loan is secured against an asset that’s been fairly valued, preventing you from borrowing more than the property is actually worth.

This whole process is closely tied to the bigger picture of the property market. For instance, things like RBA interest rate decisions have a direct impact on property values. After recent rate cuts, Australian housing values have seen steady growth, with some experts now anticipating an estimated 5.8% annual growth rate. In a market that’s always moving, getting an expert valuation is more important than ever. You can read more on how rate cuts influence housing growth to see the full story.

Ultimately, by understanding what a property appraisal is and the vital role it plays, both buyers and sellers can move forward with much greater confidence and peace of mind.

Simple Steps to Prepare for Your Property Appraisal

While you can’t exactly pick up your house and move it to a different suburb, you absolutely have control over its condition. A bit of prep work before the appraiser arrives can make a world of difference, ensuring your property is seen in its best light for a fair and accurate valuation.

Think of it like getting your home ready for a special guest. First impressions are powerful, and a few simple actions can have a surprisingly big impact. Start with the outside to give your home's kerb appeal a real boost.

Your Pre-Appraisal Checklist

Putting in a little effort before the valuer walks through the door allows them to see your home's best features without any distractions getting in the way.

- Tackle Minor Repairs: That dripping tap in the bathroom? The cracked tile in the laundry? Those little scuffs on the wall? Now’s the time to fix them. These small jobs signal that the home is well-maintained and you've taken pride in ownership.

- Declutter and Clean: A clean, tidy space instantly feels bigger, brighter, and more inviting. Make sure every room, window, and storage area is easy to access so the appraiser can get a clear view of everything.

- Gather Your Documents: It's a great idea to pull together a simple folder with key paperwork. Include a list of any recent upgrades or renovations you've done (with costs, if you have them), along with council approvals for extensions and recent utility bills.

Preparing for an appraisal isn’t about hiding flaws; it's about highlighting strengths. By providing clear documentation of improvements and ensuring the home is well-presented, you help the valuer build a complete and accurate picture of its value.

Taking these steps shows that your home has been genuinely cared for. If you'd like to dive deeper into what valuers look for, our guide on the power of in-person property appraisals in Mandurah offers some extra perspective.

Get Your Professional Appraisal with David Beshay Real Estate

So, you're ready to find out what your property is genuinely worth in today's market? The first thing to get your head around is the difference between a formal bank valuation and a real estate agent’s market appraisal. Think of it this way: a bank valuation is a strict, conservative process they use for lending purposes. Our market appraisal, on the other hand, is a realistic, no-strings-attached guide to help you understand your position.

We don't just pull a number out of thin air. We combine our deep, on-the-ground knowledge of the Mandurah market with the very latest sales data. This two-pronged approach gives us a practical estimate of what your property could genuinely sell for right now. Our aim is simple: to give you the clarity and confidence you need to plan your next chapter, whether you're looking to sell tomorrow or just testing the waters.

An agent's market appraisal is your starting point, your first strategic move. It's designed to arm you with the right information so you can make smart decisions in a fast-moving property market, all without any pressure or commitment.

Getting started is easy. Our expertise will help you see exactly where your property stands, empowering you to make a move when the time is right for you. We invite you to request a free property appraisal with our team and get the insights you need.

Common Questions About Property Appraisals

Even once you get your head around the basics of property appraisals, it’s completely normal to have more questions. This is a process that sits at the heart of major financial decisions, so you need clear, straightforward answers. Let’s run through some of the most common queries we get from homeowners and buyers right here in Australia.

One of the first things people ask is about the lifespan of an appraisal. How long is the report actually good for?

In most cases, a formal property appraisal is considered reliable for about 90 days. The real estate market never sits still; values can change thanks to interest rate shifts, local supply, and buyer demand. Because of this, lenders will almost always ask for a fresh valuation after this three-month window to make sure the numbers reflect the current market.

Can You Challenge a Low Appraisal?

Getting a valuation that’s lower than you hoped for can be a real blow, but it’s not necessarily the end of the road. Yes, you absolutely can challenge a low property appraisal, but you need to go about it the right way. Simply saying you disagree with the figure won't get you very far.

To have a real shot at an appeal or reconsideration, you need to arm yourself with solid evidence. This could include things like:

- Factual errors in the report: Did they get the land size, number of rooms, or square meterage wrong? Point it out.

- Missed comparable sales: Details of recent, similar property sales in your immediate area that the valuer might have overlooked.

- Undocumented improvements: Proof of any significant upgrades or renovations that weren't factored into the final number.

Your challenge has to be objective and backed by data to be taken seriously.

The key difference between a market appraisal and a council valuation is their purpose. A market appraisal determines what a property might sell for today, while a council valuation is used purely to calculate rates and land tax.

Who Pays for the Appraisal?

Another point of confusion is who covers the cost. In the vast majority of situations, the borrower pays for the property appraisal. It doesn’t matter if you’re buying a home or refinancing an existing loan; the cost is usually rolled into your loan application or closing fees.

Even though the bank or lender orders the report to protect their own investment, the expense gets passed on to you. This is standard practice and ensures the lender gets an impartial, third-party view of the property's value before they finalise the loan.

Are you ready to understand your property's true potential in the current market? Contact the team at David Beshay Real Estate for a comprehensive, obligation-free market appraisal to get the clarity you need. Learn more at https://realestate-david-beshay.com.au.

Pingback: What Is Property Valuation? Your Essential Guide - David Beshay Real Estate - The Agency

Pingback: Your Free Property Appraisal Online Guide - David Beshay Real Estate - The Agency

Pingback: How Do You Sell Your House Privately in Australia? Learn Now - David Beshay Real Estate - The Agency