Let's be honest, saving up a 20% deposit for a home can feel like a mammoth task, especially in a competitive market like Mandurah. Just when you think you're getting close, property prices can creep up again. This is where Lenders Mortgage Insurance (LMI) comes into the picture.

So, what exactly is it? Think of LMI as a one-off insurance premium that gives your lender the confidence to approve your home loan even if you have a deposit smaller than 20%. It's not insurance for you; it's for them. It covers their risk if, for whatever reason, you can't make your mortgage repayments down the track.

Unlocking Your First Home Sooner With LMI

For many first-time buyers, LMI is the key that unlocks the door to homeownership years earlier than planned. Banks see a 20% deposit as the gold standard—a sign of a "low-risk" borrower. If you come to the table with a smaller deposit, say 10% or 15%, they see it as a higher risk.

LMI is designed to bridge that risk gap.

By paying for this insurance, you're essentially covering the lender's extra risk. In return, they're happy to lend you the money with a smaller deposit than they would normally accept.

It's a trade-off. You pay an extra fee upfront, but you get onto the property ladder much faster. In a rising market, getting in sooner can often work out to be a very smart financial move.

Before we go further, let's break down the basics with a quick summary.

LMI Core Concepts at a Glance

This table simplifies the most critical aspects of Lenders Mortgage Insurance to give you a clear, at-a-glance understanding.

| Concept | Simple Explanation |

|---|---|

| What It Is | A one-off insurance premium paid to the lender. |

| Who It Protects | The bank or lender, not the home buyer. |

| When It's Needed | Usually when your deposit is less than 20% of the property's value. |

| Why It Exists | To give lenders the confidence to approve loans with smaller deposits. |

| The Outcome | It allows you to buy a home sooner with less savings upfront. |

Understanding these core points is the first step to making an informed decision about your home loan.

Who Does LMI Really Protect?

This is the most common point of confusion, so it’s worth repeating: LMI protects the lender, not you. If you were to default on your loan and the sale of your home didn't cover the outstanding balance, the LMI policy would pay the bank the difference.

It’s crucial to know that this doesn't wipe the slate clean for you. The insurance company that paid the lender can still legally pursue you to recover that money. So, think of it less like personal insurance and more like a security fee you pay to the bank for taking on a higher-risk loan.

LMI in the Australian Property Market

Lenders Mortgage Insurance is a huge part of the Australian property scene, helping thousands of Aussies buy a home every year. It’s particularly common among first-time buyers trying to keep up with rising property prices and the ever-increasing cost of living.

With the average first home buyer loan in Australia now at $560,249—a massive 15.9% jump in just one year—it’s no surprise that many people need to borrow more than 80% of a property's value. You can dig into more of these trends in Finder's detailed report on Australian home loan statistics.

LMI isn't just another annoying fee; it’s a strategic tool. Once you understand how it works, you can decide if it's the right move to get you into your dream home sooner.

When LMI Becomes a Requirement

Probably the biggest question I hear from home buyers is, "Will I actually have to pay for lenders mortgage insurance?" The answer always comes down to one thing: the size of your deposit. LMI isn't some random fee tacked on by the banks; it’s a specific requirement that kicks in when a buyer doesn't meet a certain financial benchmark.

In Australia, that magic number is almost always a 20% deposit. If you’ve saved up less than 20% of the home's purchase price, your lender will almost certainly require you to take out an LMI policy. Why? Because from their perspective, a smaller deposit means higher risk when they're lending you hundreds of thousands of dollars.

To really get this, we need to look at the main metric the banks use.

The Role of Loan to Value Ratio

The entire LMI decision boils down to your Loan-to-Value Ratio (LVR). It’s just a simple percentage that shows how much you need to borrow compared to the property's value. The formula is really straightforward:

LVR = (Loan Amount / Property Value) x 100

If your LVR is over 80%, LMI is pretty much guaranteed. An LVR of 80% or less means you've hit that 20% deposit milestone and can sidestep the premium altogether. This ratio is the single most important factor for LMI.

An Example in the Mandurah Market

Let's put this into a real-world scenario for someone buying a place right here in Mandurah.

- Property Price: $550,000

- Your Saved Deposit: $55,000 (which is exactly 10% of the property price)

- Loan Amount Needed: $495,000

Now, let's plug those numbers into the LVR calculation:

($495,000 / $550,000) x 100 = 90% LVR

Because the LVR is 90% — a good bit higher than the 80% threshold — the lender will need LMI to feel secure enough to approve the loan. Figuring out your potential LVR early is a huge part of your home-buying prep. It's also why getting a solid home loan pre-approval is so valuable, as it gives you a clear picture of where you stand with lenders.

Who Pays for LMI and How

Let's be crystal clear on this: the borrower pays for LMI, even though the policy is there to protect the lender. When it comes to paying this one-off premium, you generally have two choices.

- Pay Upfront as a Lump Sum: You can pay the entire LMI premium out of your own pocket at settlement. This can be a hefty cost on top of your deposit, stamp duty, and all the other moving expenses.

- Capitalise it into Your Loan: This is what most people do. The lender simply adds the LMI premium to your total loan amount, and you pay it off over time.

While capitalising avoids a big upfront hit, remember it's not free money. When you add the LMI cost to your mortgage, you'll be paying interest on it for the life of the loan. Over 25-30 years, that can add up to thousands of extra dollars.

How Your LMI Premium Is Calculated

Figuring out the cost of Lenders Mortgage Insurance isn't as simple as looking up a standard fee on a price list. The premium isn't one-size-fits-all; it's a dynamic calculation based on how much risk the lender is taking on by approving your loan with a smaller deposit.

Think of it a bit like car insurance. A younger, less experienced driver in a high-performance car is going to pay a higher premium than a seasoned driver with a spotless record in a safe family wagon. The principle with LMI is the same: the higher the lender's perceived risk, the higher the cost of the insurance policy.

Key Factors Influencing Your LMI Cost

Insurers look at a few main variables when crunching the numbers for your premium. While the exact maths can differ between providers, the core components are always the same.

- Property Value and Loan Amount: These are the foundational numbers. A bigger loan on a more expensive property naturally represents a greater financial risk for the lender if things go south.

- Your Loan-to-Value Ratio (LVR): This is the big one. Your LVR is the percentage of the property’s value you are borrowing. A smaller deposit means a higher LVR, which directly translates to higher risk and, you guessed it, a more expensive LMI premium.

- Employment Status: Lenders and their insurers love to see stable, long-term employment. If you're self-employed, a casual worker, or have recently changed jobs, this might be viewed as a slightly higher risk factor.

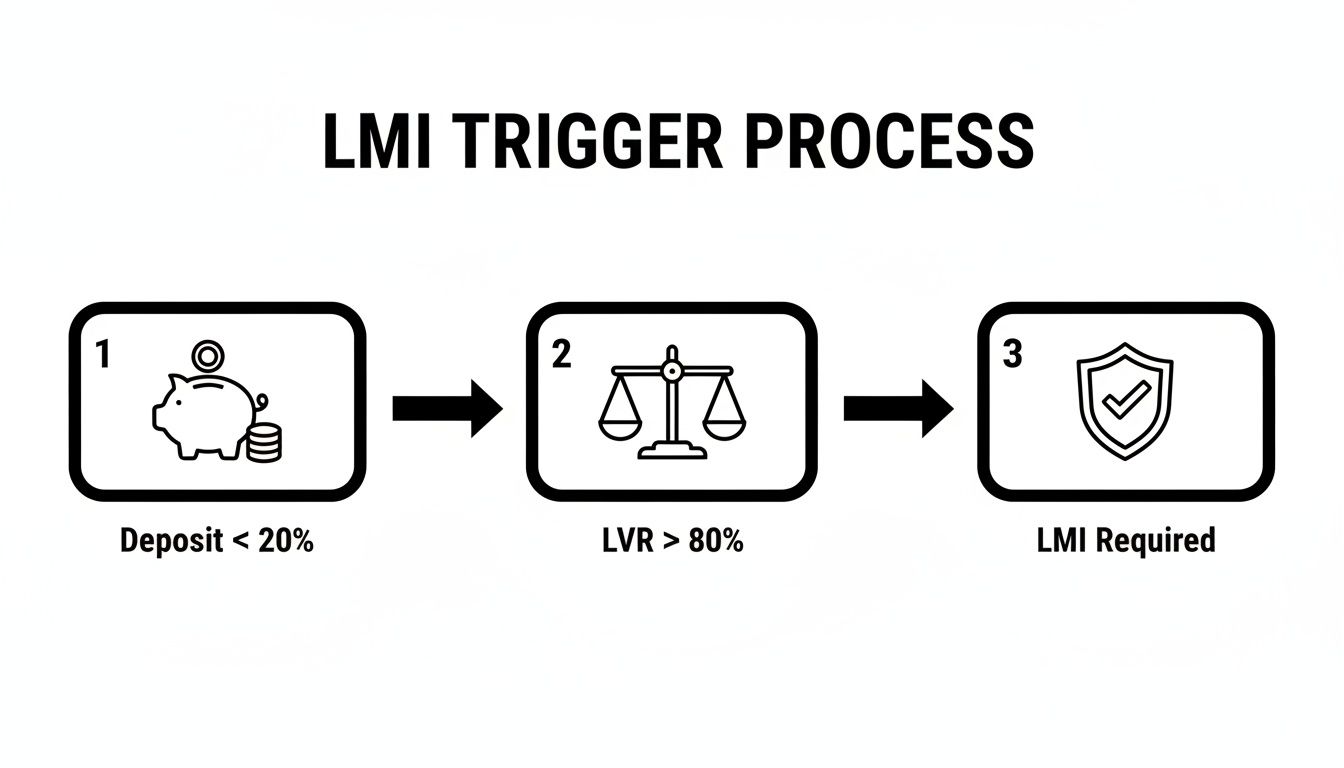

This simple flowchart shows exactly how a deposit under 20% kicks off the need for LMI.

As you can see, it all comes down to the high Loan-to-Value Ratio that results from a smaller deposit. That’s what makes LMI a non-negotiable for the lender.

LMI Calculation: A Mandurah Example

Let's make this tangible with a real-world scenario for a property right here in Mandurah. This comparison really highlights just how much your deposit size can swing your LMI cost.

Scenario Details:

- Property Purchase Price: $580,000

Buyer 1: 10% Deposit

- Deposit: $58,000

- Loan Amount: $522,000

- LVR: 90%

- Estimated LMI Premium: Approximately $12,500

Buyer 2: 15% Deposit

- Deposit: $87,000

- Loan Amount: $493,000

- LVR: 85%

- Estimated LMI Premium: Approximately $6,900

In this example, just by scraping together an extra 5% for their deposit, Buyer 2 saves around $5,600 on their LMI premium. It's a powerful demonstration of the direct link between your LVR and the final cost of your insurance.

This is exactly why getting your head around LVR is so important. You can dig deeper into this concept in our detailed guide on what is Loan-to-Value Ratio. Arming yourself with this knowledge shows you exactly where you can save.

The mortgage broking sector is crucial in helping buyers navigate these complexities. The industry has grown into a $6.2 billion powerhouse, fuelled by a 10.6% annual growth rate. Brokers are essential guides for first-home buyers, especially as average national loan sizes have jumped 16.6% yearly to hit $693,802, pushing more and more loans into the LMI bracket. You can find more details on these market trends and their impact in this IBISWorld industry report on mortgage brokers.

Proven Strategies to Avoid or Reduce LMI

While paying Lenders Mortgage Insurance can be a smart move to get into the property market sooner, let's be honest—most of us would rather keep that money in our own pockets. It’s a significant cost, and avoiding it is a high priority for many home buyers.

The good news is that saving up a 20% deposit isn’t the only way out. There are several clever strategies that can help you minimise or even completely sidestep the LMI premium, potentially saving you thousands from day one. Let's break down the most effective options available to buyers here in Western Australia.

Use a Guarantor Home Loan

One of the most common ways to dodge LMI is by using a guarantor home loan. This is where a close family member—usually a parent—uses the equity they have in their own property to act as extra security for your loan.

Think of it this way: your cash deposit might only be 10% of the purchase price. Your guarantor then pledges a portion of their home's equity to cover the remaining 10%. In the lender’s eyes, this brings your total security up to that magic 20% threshold, which means the risk is gone and so is the need for LMI.

Key Takeaway: A guarantor loan can allow you to borrow up to 100% of the property value without paying a cent in LMI. It’s a fantastic option for buyers who have strong family support from someone with significant equity in their own home.

It’s worth noting this is a huge commitment for your guarantor. Their property is on the line if you can't make your repayments, so it’s absolutely essential that both you and your guarantor get independent legal and financial advice before going down this path.

Access Government Assistance Programs

The Australian government has rolled out some brilliant schemes to help first-home buyers get over the deposit hurdle and avoid LMI altogether. These programs have already helped thousands of Aussies into their first homes, and they could be a game-changer for you, too.

The most popular one is the First Home Guarantee (FHG). Through this scheme, the government essentially acts as a guarantor for up to 15% of the property value. This allows eligible buyers to purchase a home with a deposit as small as 5% without having to pay for Lenders Mortgage Insurance.

Here are the main government schemes to look into:

- First Home Guarantee (FHG): The big one. Helps you buy with just a 5% deposit and no LMI.

- Regional First Home Buyer Guarantee (RFHBG): A dedicated version of the FHG for those buying in regional areas like Mandurah and the Peel region.

- Family Home Guarantee (FHG): A lifeline for eligible single parents and legal guardians, allowing them to buy a home with a tiny 2% deposit, again with no LMI.

These programs come with rules, like income caps and property price limits, so be sure to check the latest requirements on the Housing Australia website to see if you qualify.

Comparing LMI Avoidance Strategies

Navigating your options can be tricky. This table breaks down the main strategies to help you see which one might be the best fit for your situation.

| Strategy | Best For | Key Requirement |

|---|---|---|

| Guarantor Loan | Buyers with strong family support. | A close relative (usually a parent) with sufficient equity in their own property who is willing to act as guarantor. |

| First Home Guarantee | First-home buyers who can save a 5% deposit but not 20%. | Meeting income and property price caps set by the government, and being an eligible first-home buyer. |

| Gifted Deposit | Buyers receiving financial help from family. | A formal "gift letter" confirming the money is a non-refundable gift, not a loan. |

| Professional Waiver | High-income professionals in specific fields. | Being employed in an eligible occupation (e.g., doctor, lawyer, accountant) and meeting the lender's criteria. |

Each path has its own set of pros and cons, so it's all about finding the one that aligns with your personal and financial circumstances.

Explore Other Deposit Sources and Waivers

Beyond the main strategies, there are a couple of other avenues that could help boost your deposit and reduce or eliminate LMI.

A gifted deposit is a popular choice. If a family member gives you a non-refundable cash gift to put toward your deposit, most lenders will accept it as part of your genuine savings. All you need is a clear gift letter stating it's not a loan. This extra cash could be just what you need to push your deposit over a key LVR threshold and slash your LMI premium. You can see how different deposit amounts affect your costs by playing around with our house deposit calculator for Australia.

Finally, if you work in a specific high-income, stable profession, you might qualify for an LMI waiver. Lenders sometimes waive the LMI requirement for occupations like doctors, lawyers, and accountants, even if their deposit is as low as 10%. They see these professions as lower risk and are willing to make an exception to the usual rules. It's always worth asking your broker if your job puts you on that special list

Weighing the Pros and Cons of Paying LMI

Let’s be honest, Lenders Mortgage Insurance is rarely anyone’s favourite topic. It often feels like a costly roadblock on the way to getting your keys. While LMI is definitely a significant expense, it’s not always the villain it's made out to be. The trick is to see it as a strategic tool, not just a penalty.

Ultimately, the choice to pay LMI comes down to a classic trade-off: your money versus your time. Are you better off paying the premium to buy a property now with the deposit you have, or waiting potentially years to save up that full 20%?

The Biggest Pro: Getting Into the Market Sooner

Without a doubt, the strongest argument for paying LMI is the head start it gives you. In a rising property market like we’re seeing in Mandurah, waiting another two or three years to save could mean that property prices shoot up by far more than what you’d pay for the LMI premium.

Think about it this way: if a $550,000 home goes up in value by just 5% in one year, that’s a $27,500 capital gain. That potential gain could easily dwarf the LMI cost, making the premium a savvy investment to lock in a property before prices climb even higher.

By paying LMI, you start building equity in your own home right away, instead of pouring money into rent while property prices potentially drift further out of reach. It’s a calculated risk, but one that can really pay off in a strong market.

This is a familiar story all over Australia. Many first-home buyers are finding that their savings just can't keep up with rapid price growth. Recent figures show new owner-occupier loan commitments for existing homes hit a staggering $49.7 billion, with a huge chunk of those loans needing LMI. With the average loan for a first-timer now at $560,249—a 15.9% jump in just one year—LMI is still a crucial stepping stone into the market. You can dig deeper into these trends and what they mean for the insurance sector in this in-depth industry analysis from Insurance Asia.

The Clear Cons: A Significant Added Cost

Of course, we have to look at the other side of the coin. The most obvious downside is the cost itself. LMI can run into thousands of dollars, and if you choose to capitalise it—that is, roll it into your total loan balance—you'll be paying interest on that amount for the entire life of your mortgage.

This doesn't just bump up your monthly repayments; it also adds to the total interest you'll pay over decades. And it's critical to remember what LMI is for: it offers you, the borrower, absolutely no protection. You're paying a premium purely to protect your lender.

Here’s a quick summary to help you weigh it up:

- Pro: You can buy a home and get onto the property ladder years earlier.

- Con: It's a major expense that increases your total loan amount and your repayments.

- Pro: In a rising market, your home's capital growth could far exceed the cost of LMI.

- Con: The insurance policy is there to protect the lender, not you. It offers no personal benefit.

In the end, the right call depends entirely on your financial goals, how comfortable you are with risk, and what the property market is doing in your local area right now.

Where to From Here? Putting Your LMI Knowledge Into Action

Getting your head around lenders mortgage insurance is a massive step forward. Now you can take that knowledge and turn it into a genuine, actionable plan to get you closer to your property goals. The final part of the journey is all about mapping out your finances and getting the right experts on your team to pull it all together.

This is where preparation meets opportunity. It’s so important to get a realistic picture of your upfront costs and borrowing power before you even start scrolling through listings in Mandurah. The numbers can sometimes be a bit of a reality check, but trust me, going in with your eyes wide open is the best way to avoid stress down the line.

Your First Practical Steps

The most empowering thing you can do right now is to start crunching the numbers yourself. Jump online and use a few key tools to get a baseline idea of what your purchase might look like financially. These calculators are brilliant for demystifying the real costs of buying a home.

- Mortgage Calculators: These are fantastic for estimating your potential monthly repayments. You can plug in different loan amounts, interest rates, and loan terms to see what feels comfortable for your budget.

- Stamp Duty Calculators: Stamp duty is one of the biggest upfront costs you’ll face, no doubt about it. A good calculator will give you a specific figure for Western Australia, so there are no nasty surprises waiting for you at settlement.

Playing around with these tools helps you see exactly how a bigger deposit or a different purchase price directly impacts your bottom line. It takes the whole thing from being an abstract idea to a set of concrete figures you can actually plan for.

By taking the time to calculate these initial costs, you transform from a hopeful buyer into an informed one. You gain clarity on your budget, understand the impact of LMI, and can approach lenders with confidence.

The Power of Professional Guidance

While calculators are a great starting point, they can't replace personalised advice from an expert who knows the ropes. Every buyer's situation is different—we all have our own unique incomes, savings goals, and financial histories. This is exactly why partnering with a trusted mortgage broker is the single most important next step you can take.

A good broker does so much more than just find you a loan. They become your strategic partner, digging into your specific financial circumstances to find a lending solution that’s a genuinely good fit. They know the ins and outs of different banks' policies (which change all the time!) and can pinpoint lenders who will look more favourably on your situation.

For anyone looking to buy in the Mandurah region, a local broker brings that extra layer of market insight. They can help structure your finances correctly, guide you through any government schemes you might be eligible for, and work to minimise costs like LMI wherever possible. Their expertise is absolutely essential for navigating the complexities of securing a home loan and making your dream of owning a home a reality.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following the provided style guide.

Your LMI Questions Answered

Even after you get your head around the basics of lenders mortgage insurance, it’s completely normal to have a few questions still floating around. Home loans have a lot of moving parts, and LMI can feel like one of the trickiest.

To help clear up any lingering confusion, we’ve tackled some of the most common questions we hear from buyers right here in Mandurah and across WA. These practical answers will give you a better feel for how LMI works on the ground.

Is Lenders Mortgage Insurance Tax Deductible?

This is a great question, and the answer really hinges on one thing: what you're planning to do with the property.

For the vast majority of people buying a home to live in—what the banks call an "owner-occupier"—the answer is a straightforward no. Because it's tied to buying your main residence, LMI is seen as a capital expense, so you can't claim it on your personal tax return.

But the story changes completely if you’re buying as an investor.

If you purchase an investment property and pay LMI, the premium is generally tax-deductible. The Australian Taxation Office (ATO) considers it a cost of generating rental income. The catch is that you typically claim the deduction over five years, not as a lump sum in the first year.

As always, it's a smart move to have a chat with your accountant to see exactly how this applies to your situation before making any big financial decisions.

Can I Get a Refund on My LMI Premium?

This one comes up a lot, especially from buyers who are thinking ahead. What if you sell the place or refinance to a different lender just a couple of years down the track?

Unfortunately, in almost every case, LMI premiums are non-refundable. Once that one-off payment is made at settlement, you won't see it again, even if you pay off your loan much faster than expected.

While there used to be rare exceptions where a lender might offer a partial refund if you paid out the loan in the first year or two, this is almost unheard of now. It’s safest to think of your LMI premium as a sunk cost. It’s also important to know that your LMI policy isn't portable. If you decide to refinance with a new bank, you can't just transfer it over. You’ll have to take out a brand new policy if your loan-to-value ratio is still above 80%.

Do All Banks Charge the Same for LMI?

No, they definitely don't. While the idea behind LMI is the same everywhere, the actual dollar figure you're quoted can vary quite a bit between lenders. Banks don't actually provide the insurance themselves; they use one of a few major insurance providers in Australia, like Helia or QBE.

Each of these insurers has its own rate card for calculating the premium based on your loan size and LVR.

So, why the difference in quotes?

- Different Insurance Partners: Lenders have relationships with different LMI providers, and each provider has its own pricing.

- Unique Risk Profiles: Some banks might consider certain types of properties or borrowers a higher risk and add a loading to the standard premium.

- Negotiated Deals: A major bank might have a special deal with an insurer that gives their customers slightly better rates than a smaller credit union could offer.

This is exactly where a good mortgage broker proves their worth. They have the tools to quickly compare LMI premiums from dozens of lenders, making sure it's not just the interest rate you're looking at, but the total upfront cost. This gives you a much clearer picture of what your home loan will really cost you from day one.

Navigating the complexities of the Mandurah property market requires local expertise and a strategic approach. At David Beshay Real Estate, we provide the guidance and support you need to make confident, informed decisions on your home buying journey. Whether you have questions about LMI or are ready to find your perfect home, we're here to help. Explore our resources and see how we can assist you at https://realestate-david-beshay.com.au.