If you're looking to buy your first home in Western Australia, you've probably heard about the First Home Owner Grant (FHOG). It's a fantastic government scheme designed to give you a leg up, but what exactly is it?

Simply put, the WA First Home Owner Grant is a one-off payment of $10,000 from the state government. It’s for eligible first home buyers who are buying or building a brand-new home. The best part? It's a grant, not a loan, which means you never have to pay it back.

A Head Start for Your Homeownership Journey

Think of the FHOG as a powerful financial boost just when you need it most. Getting into the property market for the first time is a huge step, and the upfront costs—from the deposit to legal fees—can feel daunting. This grant is the government's way of giving you a helping hand, providing a direct injection of cash to lighten that initial load.

But it's about more than just the money. It's about turning the dream of owning a home into a tangible reality for more West Australians. By specifically targeting new builds, the grant also stimulates the state's construction industry, which means more jobs and more new housing.

The Purpose Behind the Grant

The First Home Owner Grant isn't a new concept. It was first rolled out back in July 2000 to support first-time buyers and give the housing sector a bit of a kick-start. Originally set at $7,000, it was designed to help offset the financial hit of the new Goods and Services Tax (GST) on home purchases.

And it worked. According to the Australian Bureau of Statistics, loans to first home buyers jumped from around 12% to over 25% almost immediately after it was introduced.

At its core, the grant has two clear goals:

- To Improve Affordability by giving you a cash payment that can go towards your deposit, settlement costs, or other expenses.

- To Stimulate Construction by limiting it to new homes, which supports our local builders and tradespeople.

The FHOG isn't a complex loan with hidden clauses. It's a straightforward, one-time payment intended to give you a significant advantage as you step onto the property ladder for the first time.

What It Means for Your Budget

So, how much of a difference does $10,000 actually make? A huge one.

Receiving a tax-free payment of that size can completely change your financial position. It might be the final piece of the puzzle you need to secure your home loan by strengthening your deposit. It could also cover other big costs like conveyancing fees, valuation charges, and building inspections.

This frees up your own savings for the things that turn a house into a home—like furniture, moving expenses, or even setting up a solid emergency fund for your new property. For many West Australians, this grant is the key that finally unlocks the door to their first home.

Qualifying for the WA First Home Owner Grant

Getting your head around the eligibility rules for the WA First Home Owner Grant is easily the most important part of the journey. Think of it like a checklist before a big trip—if you miss a single item, you might not get off the ground.

The government has set these rules to make sure the grant helps who it's supposed to: genuine first home buyers building or buying a brand-new home to live in. Let's break down each of the main requirements, one by one.

The Applicant Rules: Who Can Apply

Before you even start looking at properties, the first check is a personal one. The grant has some non-negotiable rules about who can apply, and these form the foundation of your eligibility.

To start, at least one of the applicants must be an Australian citizen or a permanent resident. You also need to be a real person (not a company or trust) and be at least 18 years old when you apply.

But the biggest rule, and where people often get tripped up, is your property history.

- No Prior Ownership: You (and your spouse or partner) can't have owned a residential property anywhere in Australia before. This counts for investment properties or homes you never even lived in.

- No Previous Grant: You can't have already received a First Home Owner Grant in any other Aussie state or territory. It's strictly a one-time deal.

This "no prior ownership" rule is incredibly strict. Even owning a small share in a property years ago could rule you out, so it's vital to be absolutely sure of your history before you go any further.

The Property Criteria: What You Can Buy

Once you've ticked the personal boxes, the next step is making sure the home you want to buy actually qualifies. This is a key part of the grant in WA because it’s specifically designed to encourage new construction.

The grant is only for buying or building a new home. In simple terms, this means no one has ever lived in it or it hasn't been sold as a residence before. This includes:

- A brand-new house, apartment, or townhouse.

- A home you've purchased "off-the-plan."

- A property that has been substantially renovated to the point where it's considered a new home.

What's crucial to remember is that the grant is not available for established homes. While you might get other perks like stamp duty concessions for an established property, the $10,000 grant itself is reserved for new builds.

Property Value Caps and Location

The total value of your home and land package is another critical factor. The government has put caps in place to ensure the grant supports affordable entry into the market, and these limits change depending on where the property is in WA.

The state is essentially split by the 26th parallel south latitude line, which runs just north of Shark Bay.

Property Value Thresholds

| Location of Property | Maximum Total Value (Land + Home) |

|---|---|

| South of the 26th parallel (including Perth) | $750,000 |

| North of the 26th parallel (e.g., Karratha, Broome) | $1,000,000 |

If the total value of your property goes over these caps, you won't be eligible for the grant. For most people buying in and around Perth, that $750,000 figure is the key number to keep in mind while you're house-hunting. For a deeper look into financial planning, our comprehensive first home buyer guide has plenty more tips.

The Residency Requirement: Living in Your New Home

The final piece of the eligibility puzzle is all about actually living in the property. The government isn't handing out this money for you to build an investment portfolio—it's to help you find a place to call home.

To meet the criteria, you must move into your new home as your main residence within 12 months of settlement or the completion of the build. On top of that, you have to live there continuously for at least six months.

This isn't just a suggestion; it's a legal requirement. The Office of State Revenue does conduct audits, and if you're caught not meeting this rule, you could be forced to repay the grant, often with some hefty penalties. It's essential that every person on the application is ready to meet this condition.

How to Navigate the Application Process

So, you’re ready to turn the idea of a $10,000 grant into actual cash for your first home. It all comes down to the application process. At first glance, it might feel a bit daunting, but it’s more straightforward than you think.

Think of it like putting together flat-pack furniture – as long as you have all the pieces laid out and follow the instructions, you’ll get there. This guide breaks it all down, step-by-step, so you can lodge your First Home Owner Grant WA application with confidence.

Choosing Your Application Pathway

Your journey to securing the grant kicks off with one key decision: how you'll submit the paperwork. The path you choose often depends on your finances and can influence how quickly you get the funds.

You’ve got two main options:

-

Through an Approved Agent (Your Lender): This is the go-to route for most people and often the easiest. An "approved agent" is just a fancy term for your bank, credit union, or the financial institution giving you a home loan. They’ll handle the FHOG paperwork as part of your home loan application.

-

Directly with RevenueWA: If you’re not getting a loan to buy your home (for example, if you’re a cash buyer), you can apply directly to the WA government's Office of State Revenue.

For the majority of first home buyers, going through a lender is the path of least resistance. Your mortgage broker or bank is already collecting most of the necessary documents for your home loan anyway, so bundling the grant application in with it is just plain efficient. They’ll guide you, check your forms, and submit everything on your behalf. For more on this, our guide on how to get a home loan is a great place to start.

Gathering Your Essential Documents

A successful application is all about having your paperwork in order. Getting organised now will save you from major headaches and delays later. Think of it as your pre-flight checklist; every item is crucial for a smooth take-off.

To get your application across the line, you’ll need to pull together a few key documents.

Required Documents Checklist for FHOG Application

Getting your documents ready beforehand is the single best thing you can do to speed up the process. Here’s a clear checklist of what you'll need to have on hand.

| Document Category | Specific Examples | Purpose |

|---|---|---|

| Proof of Identity | Driver’s licence, passport, birth certificate | To satisfy the 100-point identification check for all applicants. |

| Citizenship/Residency | Australian passport, citizenship certificate, relevant visa | To prove you meet the residency and citizenship requirements. |

| Property Contract | Signed contract of sale or building contract | To show the details of the property you're buying or building. |

| Proof of Title | A title search or similar document | To confirm the property's legal details and ownership history. |

| Application Form | The official FHOG application form | The central document for your grant request, provided by your lender or RevenueWA. |

Having these ready to go will make the submission process a breeze and show your lender you’re a serious, organised buyer.

Pro Tip: Make digital copies of everything before you submit. Having a backup of your paperwork can be a lifesaver if anything gets lost in the shuffle or if you need to refer back to it quickly.

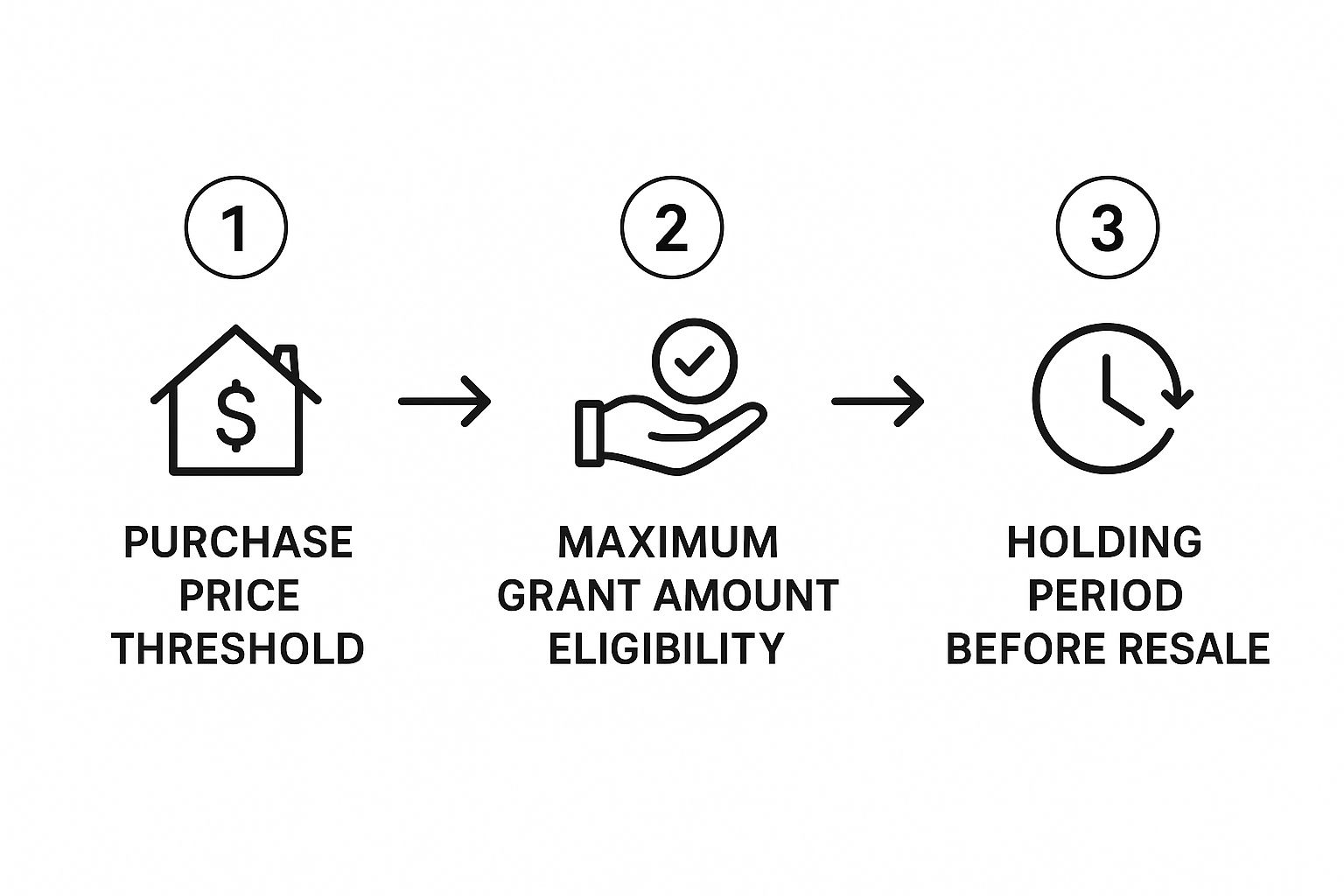

Step-by-Step Submission and Processing

Once your documents are all lined up, it’s time for the final steps: submission and approval. If you're applying through your lender, they’ll take care of this for you. If you’re going direct, you'll lodge everything with RevenueWA yourself.

This infographic breaks down the key stages you need to have ticked off before you can even think about lodging.

As you can see, the property value cap, the grant amount, and the residency period are all foundational pillars of a successful application. You need to meet all three.

After you’ve submitted everything, processing times can vary. Lenders can often provide provisional approval quite quickly, while direct applications might take a few weeks. The real key is to make sure every single detail is accurate to avoid any back-and-forth that will stall the whole thing.

Double-check names, dates, and property details before you sign that dotted line. It’s a simple step, but it can be the difference between a fast approval and weeks of frustrating delays.

Pairing the Grant with Other Savings

Securing the $10,000 First Home Owner Grant is a massive win, but don’t stop there. The WA government has another powerful saving tool you can stack on top of the grant, and it’s designed to slash your upfront costs even further.

This extra benefit is the First Home Owner Rate of Duty, but you’ll usually hear it called a stamp duty concession. Think of it like this: the grant is a direct cash injection, while the concession is a huge discount on one of the biggest hurdles you’ll face.

Understanding how these two programs work in tandem is the secret to unlocking your maximum savings. While the FHOG is only for new homes, the stamp duty savings are available for both new and established properties, giving you more flexibility in your property search.

Understanding Stamp Duty Concessions

Stamp duty, or 'transfer duty' as it's officially known, is a state tax you have to pay when you buy a property. It's calculated on the home's value and can easily climb into the tens of thousands of dollars—a pretty daunting figure for most first home buyers.

To make getting onto the property ladder more achievable, the WA government offers some serious relief from this tax for eligible first timers. It’s not another grant cheque, but rather a reduction—or even a complete waiver—of the duty you owe.

The real magic happens when you combine these perks. For a new build, you could get the $10,000 grant and pay little to no stamp duty. That’s a huge overall saving that directly boosts your buying power.

The concessions are tiered based on your property's value. Let's break down exactly how it works.

How the Savings Stack Up

The amount of stamp duty you save comes down to the dutiable value of your home. The government has set specific price thresholds where the concession really packs a punch.

- Homes up to $430,000: You pay zero stamp duty. This is a full exemption and delivers the biggest saving possible.

- Homes between $430,001 and $530,000: You get a concessional (reduced) rate. The discount gradually phases out as the value gets closer to the upper limit.

- Homes over $530,000: You’ll be up for the standard rate of stamp duty with no concession.

This structure is designed to give the greatest benefit to those buying more affordable properties, whether they’re brand new or already established.

A Real-World Example: New Home Purchase

Imagine you’re buying a brand-new, off-the-plan apartment in a Perth suburb for $420,000. Because it’s a new build and you tick all the eligibility boxes, you qualify for the $10,000 FHOG.

On top of that, since the property's value is under the $430,000 threshold, you are completely exempt from paying stamp duty. Any other buyer would have to cough up $13,875 in duty for the same purchase.

Let’s add it all up:

- First Home Owner Grant: +$10,000

- Stamp Duty Saving: +$13,875

- Total Financial Boost: $23,875

This combined saving dramatically lowers your upfront costs, making it so much easier to get the deal across the line.

Savings on an Established Home

Now, let's say you find an established home you love for the same $420,000 price tag. You won't get the $10,000 grant (since it's not a new build), but you still qualify for the stamp duty concession.

You would pay zero stamp duty, saving you the full $13,875. While the total benefit isn't quite as high as with a new build, it's still a massive financial relief that keeps established properties firmly on the table for first home buyers.

You can dive deeper into the numbers by reading our guide on first home buyer stamp duty in WA to see exactly how these calculations work.

Common Application Mistakes to Avoid

Navigating the application for the First Home Owner Grant in WA can feel like a high-stakes game. One tiny oversight on your paperwork can be the difference between a smooth approval and weeks of frustrating delays and back-and-forth communication.

To make sure you get it right the first time, it’s worth knowing the common hurdles that trip up other applicants. If you understand these pitfalls beforehand, you can put together a clean, error-free application that sails right through.

Misunderstanding the New Home Rule

One of the most frequent mistakes we see is people misinterpreting what actually qualifies as a "new home." The grant is strictly for properties that have never been lived in or sold as a residence before.

This means established homes are a no-go for the $10,000 payment, even if they’re only a few years old. Some buyers think a heavily renovated home will count, but the rules for a "substantially renovated" property are incredibly strict. It’s always best to confirm your chosen property meets the new home criteria before you start banking on the grant.

Overlooking Property Value Caps

Another classic error is forgetting about the property value caps. In the Perth metro area, the total value of your land and home package can't be more than $750,000. It's easy to get caught up in the excitement of house hunting and let this crucial limit slip your mind.

Just remember, this isn’t only the contract price of the build. It includes the value of the land, too. Always do the maths on the total package value to make sure you stay eligible.

A successful grant application is all about attention to detail. Double-checking every requirement before submission isn't just good practice—it's the best way to avoid delays and secure your funds without unnecessary stress.

Failing the Residency Requirement

The obligations don’t stop once you’ve got the keys. A critical mistake is failing to meet the residency requirement, which states you must move into your new home within 12 months and live there continuously for at least six months.

This rule is non-negotiable and applies to everyone on the application. The government does conduct audits, and if you fail to comply, you could be forced to repay the grant, often with hefty penalties attached.

The number of grants paid out often reflects how aware buyers are of these rules. Back in 2013, for instance, FHOG payments surged by 19% to 20,441 recipients, showing just how much activity there is when buyers clearly understand and meet the criteria. You can learn more about WA first home buyer trends from this analysis.

Got Questions About the FHOG?

It's completely normal for questions to pop up when you're navigating the First Home Owner Grant in WA. Even with all the info, some finer details can be tricky. Let's tackle some of the most common ones I hear from first-home buyers.

Can I Actually Use the Grant as My Deposit?

This is a big one, and the answer isn't what most people expect. While that $10,000 grant is a massive help, you generally can't count it as part of your genuine savings for your home loan application.

Lenders want to see your own savings history—it shows them you're financially responsible. The grant itself usually doesn't land in your account until settlement for a new build, or when the first construction payment is made. By then, your deposit has already been paid.

So, where does it help? Think of the grant as your financial relief fund after the fact. It’s perfect for:

- Topping your savings account back up after paying the deposit.

- Covering those extra costs like settlement fees, legal bills, or even stamp duty.

- Helping you furnish the place and buy appliances without dipping into more savings.

What If I Buy the Land Now but Don't Build Straight Away?

This is a super common path for first-home buyers in WA. You find the perfect block and snap it up, but the build comes later. The First Home Owner Grant is designed to work with this scenario, but the timing is everything.

You don’t apply for the grant when you buy the land. Instead, you'll apply when you sign the contract with your builder. The grant money is typically released once construction hits a major milestone, like the slab being poured.

Just remember the golden rule: the total value of your land plus the building contract can't go over the property value cap ($750,000 for the Perth metro area).

What Happens If I Have to Move Out Within the First Year?

This is a condition you absolutely can't ignore. The government is pretty strict here: you have to live in your new house as your main home for a continuous period of at least six months. This six-month stay must start within 12 months of settlement.

Be warned: failing to live there for the full six months can get you in serious trouble. The Office of State Revenue actively checks up on this and will make you repay the entire $10,000, sometimes with hefty penalties on top.

If a genuine emergency or unforeseen event forces you to move, you need to contact RevenueWA immediately. They might grant an exception in rare cases, but you can't count on it. The best approach is to be certain you can commit to living in the property for the required time before you even think about applying.

Navigating the real estate market requires expert guidance. At David Beshay Real Estate, we specialise in helping first home buyers in Mandurah and beyond. Let's make your property dreams a reality. Get in touch with us today!