Dipping your toes into the Australian property market is a massive step, but getting the finance sorted is often more straightforward than you might think. An investment property loan isn't just another mortgage; it's a specific financial tool designed to help you build an asset portfolio that generates wealth. Think of this guide as your roadmap, breaking down everything you need to know.

Why Now Is a Great Time for Property Investment

Getting into the Australian property market is an exciting prospect, and a quick look at the current landscape shows exactly why so many investors are making their move. Unlike the loan you get for the home you live in (an owner-occupier loan), investment property loans in Australia are looked at differently because they’re tied to an income-producing asset. This is a critical distinction—it shapes how lenders see your application and what kind of loan structures are on the table.

The goal here is to cut through the confusing financial jargon and give you a clear, practical handle on the basics. This guide is your first step toward using real estate to build your financial future, giving you the confidence to make sharp, informed decisions.

The Surge in Investor Activity

Recent trends show a huge jump in investor confidence. The market isn't just ticking along; it's seeing record-breaking levels of action from people just like you. This kind of momentum signals a really healthy environment for anyone looking to start or grow their property portfolio.

To put it in perspective, investor activity is actually outpacing the owner-occupier market right now. In a recent September quarter, new investment property loans in Australia hit a record high, with 57,624 loans approved for a whopping $39.8 billion. That’s a 13.6% lift in the number of loans and a staggering 17.6% surge in value from the previous quarter—a powerful trend by any measure. You can dig deeper into this investor surge with data from the Australian Bureau of Statistics.

Think of an investment property loan as a business partnership with the bank. You bring the strategy and management, while they provide the capital to acquire an asset designed to deliver returns through rent and capital growth.

Key Differences to Understand

It’s crucial to get your head around the core differences between borrowing for an investment property versus your own home. Nailing these points will set you up for productive chats with lenders and brokers:

- Purpose and Assessment: Lenders assess investment loans based on the property's potential rental income, which can give your borrowing power a serious boost.

- Interest Rates: You might find that rates for investment loans are sometimes a touch higher than owner-occupier loans. This is because lenders often view them as having a slightly different risk profile.

- Tax Implications: This is a big one. The interest you pay on an investment loan is generally tax-deductible, a major advantage that doesn’t apply to your standard home loan.

Decoding the Different Types of Investment Property Loans

Choosing the right loan for your investment property is like picking the perfect tool for a job—what works for one strategy might be completely wrong for another. To get the best of the investment property loans Australia has on offer, you need to match the loan structure to your specific financial goals. Are you chasing maximum cash flow, or is building equity your main game?

Let's walk through the most common loan types. Think of this as getting to know your toolkit so you can pick the right instrument for your investment plan. Understanding these options is the first step toward building a solid financial foundation for your property portfolio.

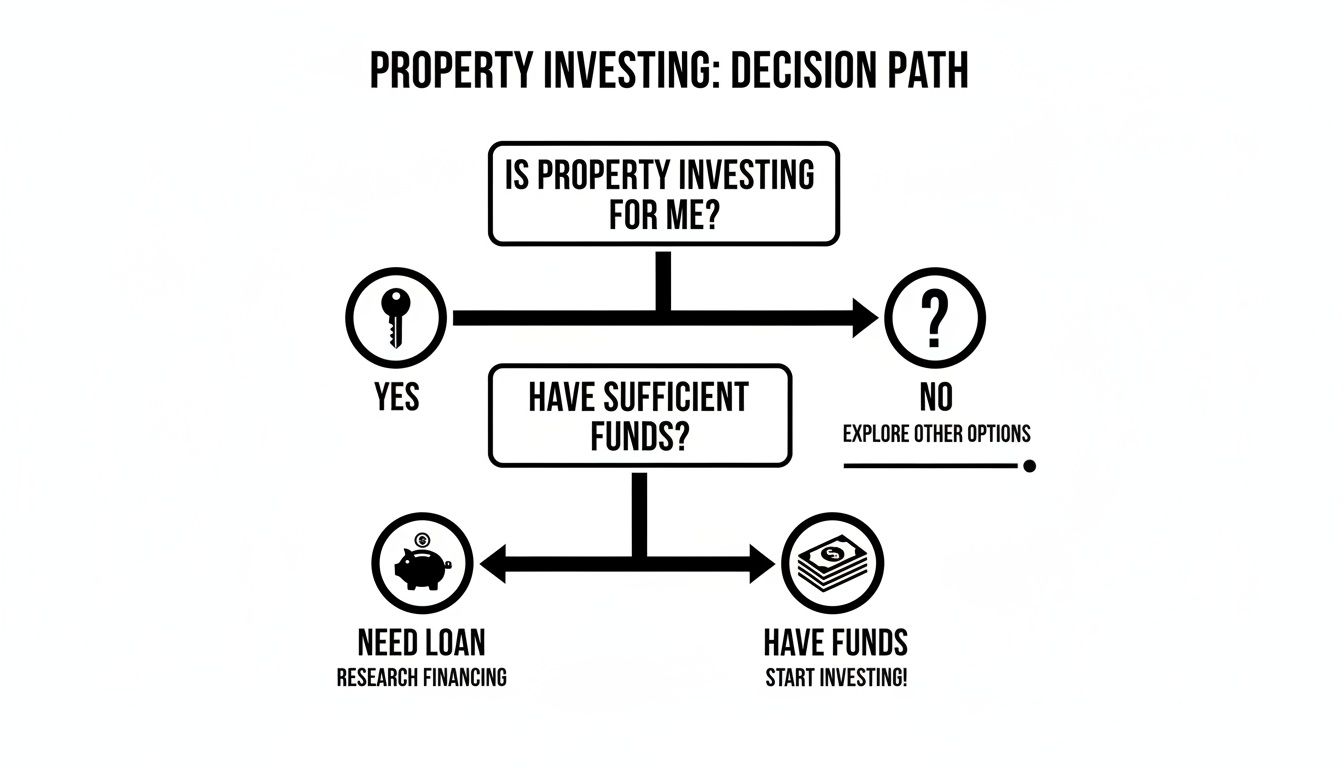

The decision tree below gives you a clear picture of the initial questions every potential investor needs to ask. It helps you figure out if property investment is the right path and where financing fits into the whole picture.

As you can see, sorting out the loan is a central part of the process for most people looking to get into the property game.

Principal and Interest Loans

Think of a Principal and Interest (P&I) loan as the classic way to buy a home. Every single repayment you make is doing two jobs: it covers the interest the bank is charging you, and it chips away at the original loan amount (the principal).

With every payment, you're actively building equity, which is just another way of saying you're increasing your ownership stake in the property. It’s a straightforward and disciplined approach, usually favoured by investors who are in it for the long haul and want to own the asset outright one day.

- Who it’s for: Best for investors with strong, reliable cash flow who want to pay down their debt steadily and build wealth through ownership. It's the lower-risk play.

- Key benefit: You’re on a clear path to owning the property free and clear at the end of the loan term.

- Main drawback: Your monthly repayments are higher because you're paying back both principal and interest. This can put a squeeze on your monthly cash flow.

Interest-Only Loans

Now, let's look at an Interest-Only loan. This is more like leasing a car than buying it. For a set period, usually between one and five years, your repayments only cover the interest on the loan. The actual loan balance doesn't shrink at all.

This structure means your monthly repayments are much lower, freeing up cash for other things. Investors often use this strategy to maximise their tax deductions (since the interest is generally tax-deductible) and improve the property's cash flow in the early years. It’s a popular choice for those wanting to grow their portfolio quickly.

An Interest-Only period is a strategic play, not a permanent solution. Once the interest-only term ends, the loan switches back to a P&I structure. Your repayments will jump up significantly because you have to start paying back the principal over a shorter remaining loan term.

It's a powerful tool, but you absolutely need a plan for when those higher repayments kick in.

Comparing Your Investment Loan Options

To make it easier to see the differences at a glance, this table breaks down how each loan structure works and who it’s best suited for.

| Loan Type | How It Works | Best For Investors Who… | Key Risk |

|---|---|---|---|

| Principal & Interest (P&I) | Each repayment covers both the interest and a portion of the original loan amount. | …have strong cash flow and want to build equity steadily while reducing their debt over time. | Higher monthly repayments can reduce cash flow, potentially limiting portfolio growth. |

| Interest-Only (IO) | For a set term (e.g., 1-5 years), repayments only cover the interest. The principal isn't paid down. | …want to maximise cash flow and tax deductions in the short term to fund further investments. | "Payment shock" when the IO period ends and repayments jump significantly to cover P&I. |

| Fixed Rate | The interest rate is locked in for a specific period, typically 1 to 5 years. | …need certainty in their budget and want protection against potential interest rate rises. | You miss out if rates fall, and there are often restrictions on making extra repayments. |

| Variable Rate | The interest rate fluctuates with the market, moving up or down over the loan term. | …want flexibility, the ability to make extra repayments, and access to features like offset accounts. | Your repayments can increase if interest rates rise, which can strain your budget. |

| Line of Credit (LOC) | A flexible loan with a set credit limit secured by property equity. You draw funds as needed. | …need ready access to funds for renovations, deposits, or other investment opportunities. | The lack of a structured repayment schedule requires discipline to avoid accumulating debt. |

Choosing the right loan really comes down to your personal strategy, risk tolerance, and financial situation.

Fixed Versus Variable Rate Loans

Once you’ve settled on either P&I or Interest-Only, your next big decision is the interest rate structure. This choice is all about certainty versus flexibility.

-

Fixed Rate Loan: This is like pre-paying for your petrol at a set price for the next three years. You know exactly what your repayments will be for a fixed term, which is fantastic for budgeting and gives you peace of mind if you're worried about rates going up. The downside? You won't get the benefit if rates drop, and you’re often limited in how many extra repayments you can make.

-

Variable Rate Loan: This is the opposite—it’s like paying the pump price for petrol each week. Your interest rate can go up or down depending on what the Reserve Bank of Australia and your lender do. The big plus here is flexibility. You can usually make unlimited extra repayments and use features like an offset account, but you also have to be prepared for your repayments to rise.

Line of Credit Loans

A Line of Credit (LOC) loan is less like a traditional loan and more like a high-limit credit card secured against your property. You get an approved credit limit based on your equity, and you can draw down funds from it whenever you need to, up to that limit. You only pay interest on the money you’ve actually used.

Investors love this for its flexibility. It means having cash ready for a quick renovation to boost a property's value or to jump on a new investment opportunity without having to go through a full loan application each time. It’s a very versatile tool, but it demands discipline to manage it properly and not let the debt get out of hand.

What Lenders Look for When You Apply for a Loan

Getting the green light for an investment property loan isn't about luck; it's about presenting a solid business case to the lender. They're not just glancing at your application—they're sizing you up as a potential business partner. If you can understand what they're looking for, you can tell your financial story in the best possible light.

Think of it this way: the lender’s main goal is to minimise their risk. They need to feel confident that you can comfortably handle the repayments, both today and if things change down the track. To figure this out, they’ll systematically check off a few key pillars of your financial health, starting with your deposit.

Your Deposit and Loan to Value Ratio

The very first number any lender zooms in on is your deposit, as it directly shapes your Loan to Value Ratio (LVR). This is just a simple percentage showing how much you need to borrow versus how much you're putting in yourself.

For example, if you're eyeing a $600,000 property and have a $120,000 deposit, your loan will be $480,000. That gives you an LVR of 80% ($480,000 loan ÷ $600,000 property value). If you want to get into the nitty-gritty, you can learn more about how to calculate your loan to value ratio in our detailed guide.

From a lender's point of view, a lower LVR is always better. An LVR of 80% or below is the gold standard. Hit that mark, and you’ll sidestep the costly Lenders Mortgage Insurance (LMI). A bigger deposit shows you’ve got financial discipline and reduces the bank's exposure.

Lenders are also keen to see proof of genuine savings. This isn't just about the total amount; it's about showing a consistent habit of saving over at least three to six months. A big lump sum that just landed in your account last week is far less convincing than a savings history that proves you can manage your money responsibly over time.

Assessing Your Income and Borrowing Power

Your capacity to actually service the loan is everything. Lenders will put your income and existing financial commitments under the microscope to work out your true borrowing power.

Here’s what they’ll dig into:

- Stable Employment Income: A steady, permanent job is what lenders love to see. If you’re self-employed or work on contract, they’ll typically want to see at least two years of tax returns and financials to get comfortable with your income stability.

- Existing Debts: Every single debt you have gets tallied up. This includes car loans, personal loans, HECS-HELP, and even your credit card limits—not just what you currently owe.

- Potential Rental Income: Now for the good news. Lenders will factor in the future rent you’ll receive from the investment property. They generally count about 70-80% of the estimated gross rental income, which builds in a buffer for vacancies and other costs.

- Living Expenses: Lenders will use a benchmark like the Household Expenditure Measure (HEM) or simply go through your bank statements to estimate your living costs. They need to be sure you can afford the loan repayments on top of your everyday life.

The Importance of Your Credit Score

Think of your credit score as your financial report card. Lenders will definitely be checking it. It gives them a quick snapshot of how you’ve managed debt in the past and whether you’re reliable with your payments. A higher score paints you as a lower-risk borrower, which can unlock better interest rates and boost your chances of approval.

You can give your score a healthy nudge in the right direction by:

- Paying all your bills on time, every single time.

- Lowering the limits on your credit cards if you aren't using the full amount.

- Avoiding too many loan applications in a short space of time. Each one leaves a mark on your file.

By getting these key areas in order—a strong deposit, stable income, manageable debts, and a clean credit history—you present yourself as a reliable investor who’s done their homework. This methodical approach is the single best way to earn a lender’s confidence and secure the financing for your next investment property loan in Australia.

Navigating the True Costs and Tax Benefits

A successful investment property journey is built on a clear financial picture that goes far beyond the initial sticker price. To really maximise your long-term returns and manage your asset properly, you need a solid grasp of the full spectrum of costs and the powerful tax benefits available. This means looking at the money you'll need upfront and the ongoing expenses required to keep your investment ticking over smoothly.

Getting this right from the start saves you from nasty surprises down the track. It also sets you up to take full advantage of the Australian tax system, which offers some pretty significant incentives for property investors. Let's break down the numbers you really need to know.

Calculating Your Upfront Purchase Costs

Before you even get the keys in your hand, you’ll face several one-off costs that absolutely must be factored into your budget. People often forget these in the excitement of the purchase, but they're substantial enough to impact the total funds you need for settlement.

- Stamp Duty: This is the big one. It's a state government tax on the property purchase, and in Western Australia, it can easily run into the tens of thousands of dollars. Using an online calculator to get an estimate is a non-negotiable first step.

- Legal and Conveyancing Fees: You’ll need a solicitor or conveyancer to handle the legal transfer of the property title into your name. This typically costs between $1,500 and $3,000.

- Loan Establishment Fees: Don't forget the bank wants its slice. Lenders often charge application fees, valuation fees, and other admin costs just to set up your investment loan.

- Building and Pest Inspections: This is your insurance against buying a lemon. It's an essential step to make sure you aren't buying a property with hidden structural problems or termite damage, costing around $500 – $800.

Budgeting for Ongoing Investment Expenses

Once the property is officially yours, the costs don't stop. These are the regular, ongoing expenses of holding the asset, and they are vital for calculating your true cash flow position. Smart investors budget for these meticulously.

Think of these as the 'running costs' of your investment business:

- Council and Water Rates: Unavoidable local government charges for services.

- Landlord and Building Insurance: Absolutely essential for protecting your asset against damage and liability.

- Property Management Fees: If you hire a professional agent to manage the tenancy (which is highly recommended!), expect to pay around 7-10% of the weekly rent.

- Repairs and Maintenance: Things break. A good rule of thumb is to set aside 1-2% of the property's value each year for unexpected repairs and general upkeep.

Understanding Tax Benefits and Gearing

This is where property investment really starts to shine in Australia. The Australian Taxation Office (ATO) allows you to claim deductions for most expenses related to owning your rental property, which can make a huge difference to your financial outcome.

Negative gearing is a common strategy where your total expenses (including the interest on your loan) are greater than your rental income. This creates a net rental loss, which you can then use to reduce your taxable income from your day job or other sources. The result? A potentially larger tax refund at the end of the financial year.

This strategy is particularly popular in a market with strong investor activity. Recent data shows investor lending for homes in Australia has seen remarkable growth, jumping to $39,776.50 million in a single quarter. This 17.6% increase highlights a strong appetite for using investment property loans Australia wide to build wealth, a trend you can explore further with insights on Australian investment lending from Trading Economics.

Some of the key tax-deductible expenses you can claim include:

- Loan interest payments

- Council rates and land tax

- Property management fees

- Insurance premiums

- Repairs and maintenance costs

Finally, when you eventually sell the property for a profit, you'll likely face Capital Gains Tax (CGT). But here's the good news: if you hold the property for more than 12 months, you may be eligible for a 50% discount on the tax you owe. To get the most out of your returns, it's vital to unlock all the investment property tax benefits available by keeping meticulous records and speaking with a qualified accountant.

How to Compare Lenders and Find the Right Loan for You

Choosing a lender for your investment property loan is about more than just chasing the lowest advertised interest rate. Think of it as picking a long-term business partner. The right financial partner will offer a loan that actually supports your investment strategy, while the wrong one can create unnecessary headaches and cost you thousands.

To properly compare the investment property loans Australia has on offer, you need to look beyond the headline number. A slightly higher rate with features that save you money elsewhere can often be the smarter move. It's about evaluating the complete package—fees, features, and flexibility.

Looking Beyond the Advertised Interest Rate

The interest rate is just one piece of the puzzle. The real cost of a loan is hidden in the comparison rate, a figure all lenders are legally required to show you. This rate bundles the main interest rate with most of the known upfront and ongoing fees, giving you a much more honest, apples-to-apples way to compare different loans.

The comparison rate is your best tool for uncovering a loan's real cost. A loan with a low headline rate but high fees can have a much higher comparison rate, revealing it to be the more expensive option over time.

Always make the comparison rate your first point of reference. You should also keep an eye out for other costs that might not be included, such as:

- Application or establishment fees: A one-off charge for setting up the loan.

- Valuation fees: The cost for the lender to value the property.

- Ongoing annual or monthly fees: Account-keeping charges that really add up over the life of the loan.

- Discharge fees: A cost you'll pay when you eventually pay off or refinance the loan.

Evaluating Crucial Loan Features

The features attached to a loan can be just as important as the rate itself, offering flexibility that can lead to significant savings. For investors, two of the most powerful features are offset accounts and redraw facilities.

- Offset Account: This is basically a transaction account linked to your loan. Any money you keep in it is ‘offset’ against your loan balance, meaning you only pay interest on the difference. For example, with a $500,000 loan and $50,000 sitting in your offset, you’ll only pay interest on $450,000. This can save you thousands and help you pay off the loan much faster.

- Redraw Facility: This feature lets you access any extra repayments you’ve made on your loan. It’s a great safety net, giving you access to cash if you need it for renovations, repairs, or other emergencies.

These features give you liquidity and can seriously reduce the total interest you pay. When you’re comparing lenders, always ask if these are available and whether any extra fees apply.

Bank vs Broker: Which Path Is Right for You?

When you’re looking for a loan, you have two main options: go directly to a bank or work with a mortgage broker. A bank can only offer its own products, which might be a good fit, but your options are limited to what they have on the shelf.

On the other hand, a mortgage broker works as a middleman, giving you access to a huge panel of lenders and dozens of different loan products.

A good broker does all the heavy lifting for you, comparing different investment property loans in Australia to find one that aligns with your financial situation and investment goals. They often have access to special deals and know how to navigate the trickiest parts of an application. If you're weighing your options, understanding the differences between a mortgage broker vs a bank can make the decision much clearer. Ultimately, it comes down to whether you feel confident going it alone or prefer having an expert guide in your corner.

Your Action Plan for Securing an Investment Loan

Knowing the theory behind investment finance is one thing, but actually turning that knowledge into a successful property purchase is another ball game entirely. It’s time to switch from learning to doing. This final section breaks down a straightforward, step-by-step game plan to get you on your way to securing the right investment property loan in Australia.

Think of these steps as a launch sequence. Each stage builds on the one before it, setting you up for a smooth and confident entry into the property market. Following this process will not only give you a crystal-clear picture of your financial position but also make you look like a serious, well-prepared buyer to real estate agents and lenders alike.

Start With the Numbers

Before you even dream of chatting with a lender, your first port of call should be an online mortgage calculator. This isn't about getting a final loan offer; it's about figuring out a realistic ballpark for what you can actually afford. A calculator helps translate your income, expenses, and deposit into a real borrowing estimate.

These tools instantly answer two massive questions:

- What’s my borrowing power? This gives you a rough idea of the maximum loan you might get the green light for.

- What will my repayments look like? Seeing the potential weekly or monthly figures makes the commitment real and is a huge help for budgeting.

This first step grounds your property search in reality, making sure you’re only looking at investments that are genuinely within your reach.

Get Expert Advice Tailored to You

Once you've got a handle on your numbers, the next crucial move is to talk to a professional. An experienced mortgage broker or a financial advisor brings insights to the table that a calculator just can't offer. They live and breathe the nuances of the various investment property loans Australia has on offer and can match the right products to your specific goals.

A great broker doesn’t just find you a loan; they help you build a financial strategy. They can assess your complete financial picture and recommend loan structures—like using an offset account or an interest-only period—that align with your long-term wealth creation plans.

This professional guidance is priceless. They do the heavy lifting of comparing lenders, navigating tricky application criteria, and structuring your finances to give you the best shot at approval. This step saves you time, stress, and potentially a huge amount of money over the life of your loan.

Secure Your Pre-Approval

With professional advice in your corner, the final action is to get pre-approved for a loan. Pre-approval is basically a conditional 'yes' from a lender, confirming they’re willing to lend you a specific amount of money. It is the single most powerful tool you can have as a buyer.

It takes you from a window shopper to a serious contender. With pre-approval in hand, you can make offers on properties with confidence, knowing your finance is already sorted. This not only gives you a firm budget to stick to but also makes your offer far more appealing to sellers, giving you a real advantage in a competitive market like Mandurah.

Frequently Asked Questions

Diving into investment property loans can feel like you're learning a new language. Let's clear up some of the most common questions we hear from aspiring investors in Mandurah and across WA, so you can move forward with confidence.

How Much Deposit Do I Really Need for an Investment Property?

The textbook answer is a 20% deposit, and for good reason—it helps you sidestep Lenders Mortgage Insurance (LMI). But let's be realistic, that's not always achievable, and it's certainly not the only way to get your foot in the door.

Many lenders will consider applications for investment property loans in Australia with a 10% or even a 5% deposit. Just know that if you go down this path, the lender will likely scrutinise your application a bit more closely, and you'll need to factor in the cost of LMI. A really popular strategy, especially for existing homeowners, is to use the equity you've built up in your own home. This can be a brilliant way to fund your deposit and grow your portfolio without needing a huge pile of cash sitting in the bank.

Will Banks Count My Future Rental Income for the Loan?

Yes, they absolutely will, and this is one of the biggest advantages of investing in property. Lenders will typically factor in about 70-80% of the potential gross rental income when they're working out how much you can borrow.

Why not the full 100%? They build in a buffer to account for those times the property might be vacant or when an unexpected repair bill pops up. To prove this income, you'll almost always need to provide a formal rental appraisal from a licensed real estate agent as part of your application.

Lenders see that potential rent cheque as a key part of your ability to make repayments. A solid rental appraisal from a reputable local agent can give your borrowing power a serious boost and make your whole application look much stronger.

Is Getting an Investment Loan Harder Than a Regular Home Loan?

It can definitely feel a bit more rigorous. From a lender's perspective, an investment loan carries a slightly higher risk than a loan for a home you're going to live in yourself.

This means they might ask for a larger deposit or want to see a more robust financial picture, including solid evidence of genuine savings. You might also notice that the interest rates for investors are sometimes a touch higher. That said, if you have a stable income, your existing debts are under control, and you've got a clean credit history, getting an investment loan is very achievable. It all comes down to presenting a well-prepared and convincing financial case to the bank.

Ready to explore your investment potential in the Mandurah property market? David Beshay Real Estate offers expert guidance and local insights to help you make your next move. Start your property journey today.