Working with a mortgage broker in Mandurah is one of the smartest moves you can make to secure finance, especially in a market this competitive. A local expert doesn’t just process paperwork; they bring insider knowledge of the Peel region's property landscape and connections to specialised lenders, giving you a serious advantage over going it alone with the banks.

Why a Mandurah Broker Is Your Best Bet in a Hot Market

Trying to buy property right now can feel like an uphill battle, particularly when demand is high and every decision matters. Mandurah is no exception—it’s become a genuine hotspot for buyers. The latest figures show the median house price has jumped to $508,250, a massive 21.3% increase in just twelve months. That kind of growth paints a clear picture of the intense competition you’re facing. You can learn more about these local Mandurah market trends to see for yourself.

This is exactly where a local mortgage broker becomes your most valuable player. They offer much more than just a list of home loans; they give you a strategic edge built on years of local experience.

Unlocking Local Market Intelligence

A broker who actually lives and breathes the Mandurah market understands its unique quirks. They know the subtle differences between suburbs like Halls Head, Falcon, and Dudley Park—and more importantly, how lenders view them. This kind of local insight is priceless.

Let’s say you’re a first-home buyer with your heart set on a place in Dudley Park. A good local broker might know which lenders have faster turnaround times or are more favourable to properties in that specific postcode, helping you put forward a more compelling offer that beats the competition.

Access to a Wider Lender Panel

The big banks can only offer you their own limited menu of products. A mortgage broker, on the other hand, partners with a diverse panel of lenders—from the major banks to smaller credit unions and non-bank lenders you’ve probably never heard of. This variety is crucial.

Think about an investor wanting to buy a holiday rental near the coast. Many traditional banks get nervous about financing properties like that. A skilled Mandurah broker will know exactly which specialised lenders are comfortable with that type of investment, saving you from a string of rejections and weeks of wasted time.

A great local broker doesn't just find you a loan; they find you the right loan for the right Mandurah property. Their expertise translates directly into a smoother process and a stronger financial outcome.

This tailored approach is what really sets them apart. They aren’t just processing an application; they’re building a financial strategy that lines up perfectly with your goals and the specific property you want to buy. Their job is to champion your application, negotiate on your behalf, and handle the mountain of paperwork, leaving you free to focus on finding your dream home.

How to Vet and Choose the Right Mandurah Broker

Finding a great mortgage broker in Mandurah goes beyond a quick Google search. It’s about doing a bit of detective work to find a true professional who has your back, not just someone looking to close a deal.

Your goal is to find a partner with both the technical qualifications and the local, on-the-ground experience to navigate your specific financial situation.

Checking the Essentials

Before you even pick up the phone, a quick background check is non-negotiable. It’s the easiest way to weed out anyone who isn’t properly qualified to give credit advice in Australia.

Here’s what you need to confirm:

- Australian Credit Licence (ACL): This is a legal must-have. A broker must either hold their own ACL or be an Authorised Credit Representative under another company's licence.

- Industry Association Membership: Look for memberships with either the Mortgage & Finance Association of Australia (MFAA) or the Finance Brokers Association of Australia (FBAA). These bodies hold their members to a strict code of conduct.

- Lender Panel Diversity: Ask how many lenders they work with. A solid broker should have access to at least 20-30 lenders, which gives you genuine choice beyond just the big four banks.

You can usually find this info on their website or by asking them directly. If they're hesitant to share it, that's a red flag.

Gauging Their Local Experience and Communication

Once you’ve ticked off the basics, it’s time to dig into what really makes a great mortgage broker Mandurah buyers can trust. Credentials are one thing, but proven experience in the Peel region is a whole different ball game.

Don't be afraid to ask for specifics. A question like, "Can you share an example of a tricky loan you secured for a first-home buyer in Falcon?" or "How have you helped a self-employed client get finance in this area?" will tell you more than a generic sales pitch.

A broker's communication style is just as important as their lender panel. You need an advisor who is responsive, clear, and proactive—someone who actually calls you back and explains complex terms without drowning you in jargon.

A quick reference guide can make this process easier. Use this checklist to evaluate and compare different brokers you're considering.

Broker Vetting Checklist

| Checklist Item | What to Look For | Why It Matters |

|---|---|---|

| Licensing & Membership | ACL/ACR Number, MFAA/FBAA membership. | Confirms they are legally qualified and adhere to professional standards. |

| Local Mandurah Experience | Specific examples of successful loans in your target suburb. | Local knowledge can help navigate lender preferences and property nuances in the area. |

| Lender Panel Size | Access to 20+ lenders, including non-bank and specialist options. | More lenders mean more competitive options and a higher chance of approval. |

| Fee Structure | Clear, upfront explanation of how they are paid (usually by the lender). | You need to know if there are any hidden or direct costs to you. |

| Communication Style | Responsiveness to calls/emails, clarity in explanations. | A good communicator reduces stress and ensures you're always informed. |

| Client Reviews | Genuine, recent testimonials on Google or their website. | Social proof offers unbiased insight into the experiences of past clients. |

This checklist isn't exhaustive, but it covers the core areas that will help you find a reliable partner for your property journey.

Mandurah has a strong network of mortgage professionals who specialise in everything from standard home loans to complex investment finance. This local expertise is vital in the region's fast-moving property market, where having the right guidance can make all the difference.

Finally, consider how their approach feels to you. The right partnership is built on trust, and you need to feel comfortable with the person guiding you through one of life's biggest financial decisions. For a deeper dive, our guide on what defines top mortgage brokers in Mandurah offers more valuable insights.

Critical Questions to Ask Your Prospective Broker

Your first meeting with a potential mortgage broker is much more than a simple chat about interest rates. Think of it as an interview. You’re hiring a crucial financial partner, and asking the right questions is the only way to see past a sales pitch and find a genuine advocate for your property goals.

These questions are designed to get under the hood, revealing a broker's real-world experience, problem-solving skills, and commitment to your unique situation.

Uncovering Real-World Experience

Anyone can say they’re experienced, so asking a generic question like "Are you experienced?" is a waste of time. You'll always get a "yes." You need to dig deeper. A great broker will have plenty of relevant stories and be able to walk you through their process with clarity.

A powerful question to start with is, "Can you walk me through a similar scenario to mine that you've handled recently?"

This one question forces them out of theory and into practice. A good answer will detail a client's goal, the specific challenges they faced (like a low deposit or complex income), and the concrete steps the broker took to get the loan approved. It gives you a direct look at their thought process in action.

Gauging Their Proactive Approach

A broker's job isn't just to submit paperwork—that’s what a postman does. Their real value lies in anticipating and solving problems. You need a fighter in your corner. This is where understanding their negotiation and troubleshooting skills becomes non-negotiable.

Ask them this directly: "How do you challenge a lender's decision if an issue arises with my application?"

A top-tier mortgage broker in Mandurah won't just accept a "no" and pass the bad news along. They should talk about escalating the issue, presenting new information, or leveraging their relationship with the bank's business development manager (BDM) to plead your case.

Listen for key phrases like:

- "First, I’d find out the lender's exact concern."

- "Then, I would work with you to gather extra evidence to counter their objection."

- "If that doesn't work, I'll use my network to speak directly with a decision-maker."

An answer like that shows they’re prepared to go the extra mile for you.

Your goal is to find a broker who sees your application as a unique puzzle to be solved, not just another file on their desk. Their answers should fill you with confidence, not leave you with more questions.

Understanding Their Communication and Service

Finally, you need to know what the day-to-day working relationship will actually look like. Misaligned expectations about communication can cause immense stress during an already tense process.

A straightforward question here is, "What does your communication process look like after my application is submitted?"

A vague answer like, "I'll keep you updated" simply isn't good enough. You want to hear about a structured process. This includes key milestones where they will proactively reach out, their average response time to calls or emails, and who your main point of contact will be.

The right mortgage broker Mandurah residents trust will have a system in place to make sure you’re never left in the dark, giving you clarity all the way from submission to settlement day.

Getting Your Paperwork in Order for a Smooth Application

Nothing slows down a home loan application faster than disorganised paperwork. Before you even sit down with a mortgage broker in Mandurah, getting your financial life in order is the single best thing you can do. It makes the whole process smoother and paints you as a strong, reliable borrower in the eyes of lenders.

Being prepared isn't just about saving time; it shows you're serious. Lenders appreciate an organised applicant, and trust me, it can make a real difference in how quickly your file moves through their system. The goal here is to present a crystal-clear snapshot of your financial health.

The Core Documents Every Lender Asks For

No matter who you are or what you do, every lender starts with the same foundational documents. Think of this as your application starter kit. Having these scanned and saved in a digital folder will make you your broker's favourite client.

- Proof of Identity: This is usually your driver's licence plus a passport or Medicare card. Lenders need to verify who you are to meet their legal obligations.

- Proof of Income: If you're a PAYG employee, this means your two most recent payslips and your latest PAYG payment summary (often called a group certificate).

- Living Expenses: Lenders are taking a much closer look at spending habits these days. Have three months of bank statements from your main transaction account ready to go so they can see your typical budget.

This first batch of documents gives your broker everything they need to start crunching the numbers on your borrowing power and figuring out which lenders are the right fit.

Proving Your Full Financial Position

Beyond the basics, you’ll need to give a complete overview of what you own and what you owe. Lenders need to see the whole picture to feel confident you can manage a new home loan. This is where you lay out all your savings, investments, and any existing debts.

Being completely upfront with your documentation is non-negotiable. A tiny detail, like a credit card you forgot about, can completely derail an application. Transparency from day one builds trust with your broker and the lender.

To paint that complete picture, you'll need statements for:

- Savings and Assets: Round up recent statements for every savings account, term deposit, and share portfolio. This shows the lender your deposit and any financial buffer you have.

- Liabilities: This includes statements for any existing mortgages, personal loans, car loans, and every single credit card—even the ones you never use.

- Self-Employed Applicants: If you're self-employed, the list is a bit longer. You’ll generally need two years of personal and business tax returns, along with your Notices of Assessment. For a full breakdown, check out our detailed guide on what you need for a mortgage loan.

The value of an experienced broker can't be overstated. Australia's top brokers collectively wrote an incredible $16.6 billion in home loans in the year to June 2024. This shows just how much experience they have packaging applications for success. That’s the kind of know-how brokers in Mandurah bring to the table. When you hand them a well-organised file, you make their job easier and get your approval faster. You can see more details about the performance of Australia's best brokers here.

Using Pre-Approval to Make a Winning Offer

In a hot market like Mandurah's, walking into a home open with a pre-approval letter is like holding a golden ticket. It completely changes the game. Suddenly, you're not just another person looking around; you're a serious, credible buyer who can actually make a move. This one piece of paper is often the decider between you getting the keys to your dream home or watching it sell to someone else.

So, what is it? A pre-approval, also known as conditional approval, is the bank’s way of saying, "Based on what we see so far, we're willing to lend you X amount." It shows the seller you've already done the hard yards with your finances and are just a few steps away from the finish line. Your mortgage broker in Mandurah is the one who quarterbacks this whole process, making sure your application is rock-solid and the pre-approved amount is realistic for your goals.

Why Pre-Approval Gives You a Strategic Edge

Having that pre-approval locked in gives you incredible confidence and, just as importantly, a crystal-clear budget. You can search for homes knowing exactly what you can afford, which saves you the heartache of falling for a place that's out of reach. It also means when you find the one, you can jump on it immediately.

For sellers and their agents, a buyer with pre-approval is a dream. It means there's a much lower risk of the sale collapsing because of finance issues. That security often makes them more open to negotiating with you, even over someone who might have offered a little more but has no finance organised.

When multiple offers are on the table, a clean offer from a pre-approved buyer can easily beat a slightly higher offer from someone without their ducks in a row. Certainty is gold in real estate.

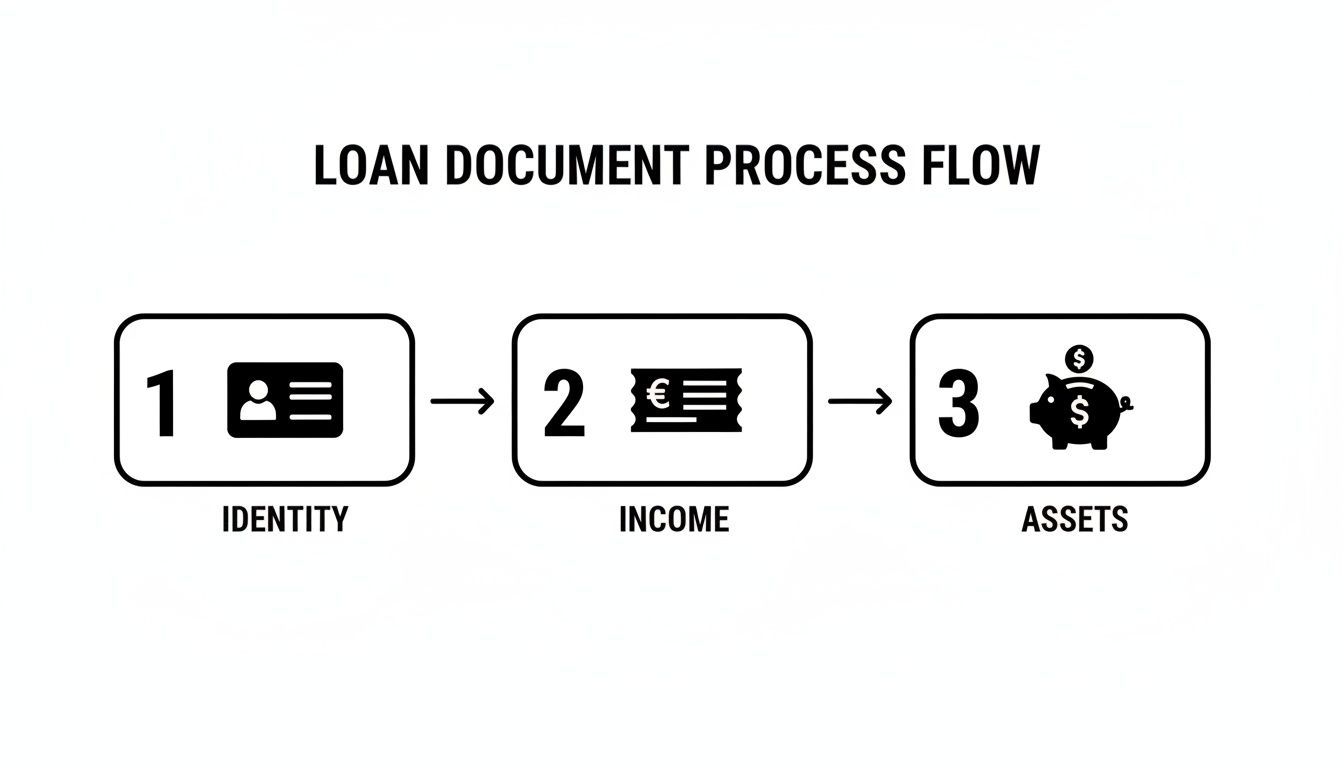

The chart below gives you a snapshot of the key documents your broker will ask for to get this crucial first step sorted.

As you can see, getting your ID, income, and asset documents organised from the start is the key to a fast and painless pre-approval.

From Pre-Approval to Unconditional Approval

Think of pre-approval as clearing the first major hurdle. Once your offer on a home is accepted, your broker kicks into overdrive to get you to unconditional (or formal) approval. This is where they really earn their keep, liaising with the lender, the real estate agent, and your settlement agent to tick off the bank's final conditions.

This final push usually involves a few key things:

- Submitting the Contract of Sale: The signed contract gets sent straight to the lender for their records.

- Arranging a Property Valuation: The lender will order an independent valuation to make sure the property is worth what you're borrowing against it.

- Final Verification Checks: Don't be surprised if the lender does one last check on your employment or recent bank statements before giving the final green light.

Understanding the distinction between these two approval stages is vital for planning your property purchase timeline.

| Feature | Pre-Approval (Conditional) | Unconditional Approval (Formal) |

|---|---|---|

| Purpose | To determine your borrowing capacity and show sellers you are a serious buyer. | The final, binding confirmation that the lender will fund your specific property purchase. |

| Property Specific? | No, it's based on your financial situation, not a specific property. | Yes, it is tied directly to the property you have an accepted offer on. |

| Key Conditions | Subject to finding a suitable property and a satisfactory valuation. | All conditions (like valuation and final checks) have been met and satisfied. |

| Legal Status | Not legally binding. The lender can withdraw the offer if circumstances change. | A formal, legally binding commitment from the lender to provide the loan funds. |

| What It Allows You To Do | Make offers with confidence and negotiate from a position of strength. | Proceed to settlement with the certainty that your finance is fully secured. |

This table highlights that while pre-approval is a powerful tool, it's the unconditional approval that signals you're truly on the home stretch.

Your mortgage broker in Mandurah is the one chasing the bank and making sure every piece of paper is where it needs to be, on time. Their experience is invaluable for handling any last-minute lender queries and ensuring a smooth run-up to settlement day. For a deeper dive into this part of the journey, check out our detailed guide on achieving home loan pre-approval and what it really means for your purchase.

Your Top Questions About Mandurah Mortgage Brokers Answered

Jumping into the home loan process always kicks up a lot of questions. It's completely normal. For anyone looking to buy or invest here in the Peel region, getting your head around what a local expert does—and what they're worth—is the first step.

Here are the straightforward, no-fluff answers to the questions we hear all the time about working with a mortgage broker in Mandurah.

So, How Much Does a Mortgage Broker Actually Cost?

This is usually the first thing people ask, and the answer tends to be a pleasant surprise. For the vast majority of standard home loans, you pay absolutely nothing to the broker for their service. It might sound too good to be true, but it's pretty simple.

The lender you end up going with pays the broker a commission after your loan settles. It’s a standard industry model. Your broker is also legally required to give you a credit guide that lays out all these commissions in plain English, so everything is transparent.

Now, in some very specific cases—think highly complex commercial deals or tricky construction loans—a fee-for-service might come into play. But this would be discussed and agreed upon with you long before you commit to anything.

Can a Broker Really Get Me a Better Interest Rate?

It's highly likely, yes—but it's about more than just the headline number. Brokers have a bird's-eye view of the entire market, with access to a massive range of lenders and dozens, sometimes hundreds, of different loan products. Many of these aren't the kind you can just walk into a bank branch and ask for.

Their real value is knowing the whole landscape, not just one bank’s menu. They use specialised software to compare products in minutes, pinpointing competitive rates and features that actually fit your life. Plus, they can often leverage their professional relationships to negotiate better terms on your behalf, potentially saving you thousands over the life of your loan.

A great broker doesn't just hunt for the lowest rate; they find the right loan structure. That means looking at things like offset accounts, redraw facilities, and fee waivers that create long-term value well beyond a slightly lower initial rate.

How Long Does This Whole Home Loan Process Take?

Every application is unique, but one thing is certain: working with a good broker almost always speeds things up. They're experts at putting together applications that tick all the lender's boxes right from the start, which cuts out a ton of the frustrating back-and-forth that causes delays.

As a general guide, here’s what the timeline can look like:

- Pre-approval: This can often be sorted within a few business days, as long as you have your documents organised.

- Full Application to Unconditional Approval: Typically, this stage takes somewhere between two and four weeks.

- Settlement: This is booked in after your loan is unconditionally approved, usually 30 to 60 days after you sign the sale contract.

The best part is your broker manages this entire timeline for you. They’re the ones on the phone chasing the bank, answering their queries, and giving you updates at every milestone so you don't have to.

What if I’m Self-Employed or Have a Complicated Income?

This is exactly where a skilled mortgage broker in Mandurah goes from being helpful to being indispensable. If you’re self-employed, a contractor, or have income streams that aren't a simple weekly payslip, walking into a bank can quickly end with a "computer says no" response.

Brokers live and breathe these complex scenarios. They know which lenders are more flexible with self-employed applicants (often using what are called ‘alt-doc’ or ‘low-doc’ loans) and they understand how to frame your financial story in the best possible light. They can translate your business financials into a language the banks understand, which dramatically boosts your chances of getting a 'yes'.

Ready to take the next step in your Mandurah property journey with clear, expert guidance? David Beshay Real Estate offers the local knowledge and professional support you need. Get your free property appraisal today!