When you apply for a mortgage, a lender really only needs to know two things: who you are, and that you're good for the money. That's it. Your job is to provide the documents that paint a clear and convincing picture of your identity, income, existing finances, and the details of the property you want to buy. Getting this sorted out upfront makes everything else fall into place so much more smoothly.

Your Mortgage Application Starter Kit

Think of applying for a home loan as building a business case for the biggest investment of your life. Lenders need to see the whole story to feel comfortable lending you a significant amount of money. Putting together this "starter kit" of documents ahead of time shows you’re an organised and serious buyer, which can seriously speed up the approval process. This preparation really comes down to four core pillars.

The Four Pillars of Preparation

A strong application is built on solid proof across four key areas. These are the fundamentals every single lender will look at:

- Your Identity: This is the easy part. We’re talking about basic identification like your driver’s licence or passport to confirm you are who you say you are.

- Income and Employment Stability: Lenders want to see a consistent, reliable income stream. You’ll need recent payslips, your employment contract, or if you’re self-employed, a couple of years' worth of tax returns.

- Your Complete Financial Picture: This means laying all your cards on the table. You’ll need statements for all your assets (like savings and investment accounts) and all your liabilities (think credit cards, personal loans, or that car loan).

- Property Details: The lender will need a copy of the signed contract of sale for the home you’re planning to purchase.

Organising this information early is one of the best things you can do for yourself in the home-buying journey. For a deeper dive into getting your finances in order first, you can learn more about securing a home loan pre-approval to put yourself in a much stronger position as a buyer.

To help you keep track of everything, here's a quick checklist of the essential items you'll need to gather for your home loan application.

Quick Checklist for Your Mortgage Loan Application

| Requirement Category | What Lenders Need to See | Why It's Critical |

|---|---|---|

| Identity Verification | Driver's Licence, Passport, Birth Certificate | Confirms you are a legitimate applicant and prevents fraud. |

| Income & Employment | Recent Payslips (3-6 months), Tax Returns (2 years for self-employed) | Proves you have a stable and sufficient income to service the loan. |

| Assets | Bank Statements (Savings, Chequing), Investment Statements | Shows you have the funds for a deposit and other costs, and demonstrates financial stability. |

| Liabilities | Credit Card Statements, Personal Loan Details, Car Loan Information | Gives a full picture of your existing debts and financial commitments. |

| Property Information | Signed Contract of Sale | Confirms the details of the property you intend to purchase and the agreed-upon price. |

Having these documents ready to go before you even speak to a lender will make you look like a top-tier applicant and can help you get that "yes" much faster.

The Three Pillars of Loan Approval

So, when you ask, "what do I need for a mortgage loan?", what a lender is really trying to figure out is pretty simple: are you a reliable borrower? They don't just glance at one part of your financial life; instead, they use a tried-and-true framework built on three core pillars to assess every application fairly.

Getting your head around these pillars is like seeing your application through their eyes. It’s your best tool for strengthening your position before you even think about submitting paperwork. This isn't just about having the right documents; it's about making sure the story they tell is a convincing one.

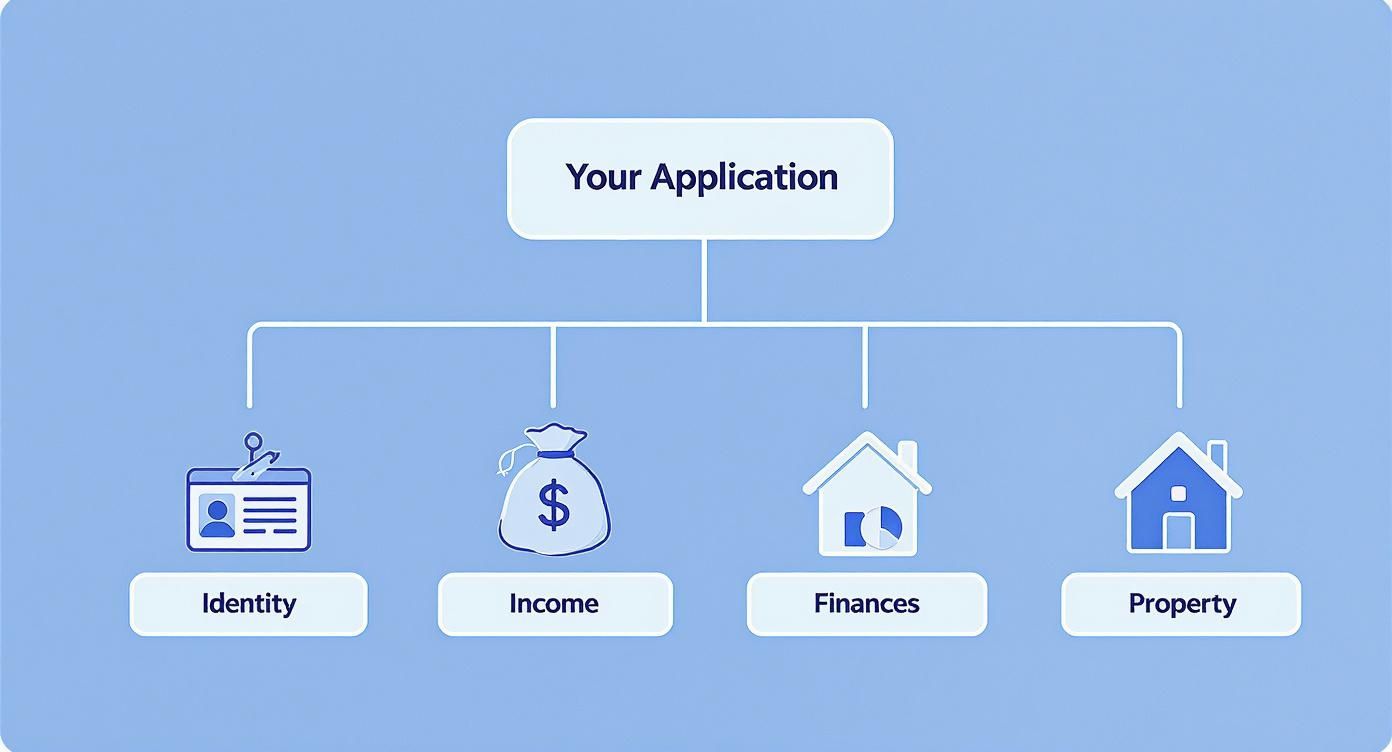

The infographic below breaks down the four key areas of information that feed into how a lender sees you.

This visual shows how your identity, income, finances, and the property details all come together to form the complete picture a lender needs. Each of these pieces plugs directly into one of the three main pillars they use for their assessment.

Your Character and Capacity

First up, lenders want to see your Character, which is basically your financial reputation. Your credit history and score tell the story of how well you've handled debt in the past. A solid track record of paying on time shows you're a responsible borrower they can trust.

Next, they look at your Capacity—your proven ability to actually repay the loan. To work this out, lenders calculate your Debt-to-Income (DTI) ratio. They need to be sure that adding a new mortgage payment won't stretch your budget to its breaking point. They want to see plenty of income left over after your existing expenses to comfortably handle the loan.

A healthy DTI ratio is absolutely crucial. Most lenders prefer a DTI below 43%, as it signals you have a manageable level of debt compared to your income, which lowers their risk.

The Collateral Securing the Loan

Finally, there’s the Collateral—the property itself. The home you’re hoping to buy acts as security for the loan. A professional valuer will assess its market worth to make sure it justifies the amount you want to borrow.

This valuation is what determines the Loan-to-Value Ratio (LVR), a key risk metric for the bank. If you can get these three pillars sorted and looking strong, you'll be well on your way to preparing an application that ticks all the right boxes for a lender.

Gathering Your Essential Paperwork

A successful mortgage application hinges on getting your paperwork in order. Think of it as the evidence that proves your financial story. Having everything ready to go before you even apply does more than just speed things up; it shows the lender you’re a serious and organised applicant.

Lenders need a crystal-clear, verified picture of your financial life before they can confidently give you the green light. Most delays pop up when people are scrambling to find a stray bank statement or an old tax return. By getting all your documents together upfront, you'll clear away any potential roadblocks and make the whole process a lot smoother for everyone.

Your Personal Identification

This is the easy part—proving you are who you say you are. Lenders need to verify your identity to prevent fraud and tick all the regulatory boxes. Generally, you’ll need to provide copies of one or two forms of photo ID.

- Primary ID: A current driver’s licence or passport is the standard go-to.

- Secondary ID: A birth certificate or Medicare card usually works as a solid backup.

Proving Your Income and Employment

This is where you show the lender you have the means to pay back the loan. They want to see a stable and reliable income. The exact documents you'll need for a mortgage loan here will depend on how you earn your money.

For PAYG (Pay As You Go) employees, it's pretty straightforward:

- Recent Payslips: Usually the last two to four consecutive payslips.

- PAYG Payment Summary: Your latest end-of-financial-year summary (what we used to call a group certificate).

- Employment Letter: A letter from your employer confirming your role, salary, and how long you've been there can also be a big help.

Self-employed applicants face a bit more scrutiny because their income can fluctuate. Lenders will typically ask for two full years of financial records to get a solid understanding of your business's stability and profitability.

For the self-employed, the list is a bit longer:

- Tax Returns: Your last two years of personal and business tax returns.

- Financial Statements: Profit and loss statements and balance sheets covering the same two-year period.

- Business Activity Statements (BAS): Your last four quarters of BAS can demonstrate consistent business turnover.

Documenting Your Financial Position

Lastly, you’ll need to give a complete snapshot of your assets and liabilities. This means showing proof of your deposit and any debts you currently have.

- Savings Statements: Three to six months of statements for all the accounts where your deposit is sitting.

- Debt Statements: Recent statements for any credit cards, car loans, or personal loans. This helps the lender get an accurate picture of your true borrowing power.

Why Your Credit Score Is a Game Changer

When you're pulling together what you need for a mortgage, your credit score is one of the most powerful tools in your arsenal. Think of it as your financial resume. It gives lenders a quick, reliable snapshot of how you’ve handled debt and whether you’ve been consistent with repayments.

A strong credit score tells a lender you're a low-risk borrower, which is exactly what they want to see. This single number can be the difference between getting approved with a fantastic interest rate or being stuck with less favourable terms that could cost you thousands over the life of the loan. In Australia, credit scores typically range from 0 to 1,200, with a higher number signalling you're a more reliable borrower.

What Lenders See in Your Score

While every lender has its own magic number, a score above 700 is generally considered good, and anything over 800 is seen as excellent. Lenders use this to gauge your reliability and, ultimately, decide how much they're comfortable lending you. A higher score often unlocks better interest rates and more flexible loan conditions.

So, what actually goes into this number? A few key things:

- Payment History: Your track record for paying bills, loans, and credit cards on time.

- Credit Utilisation: How much of your available credit you’re actually using.

- Number of Enquiries: Applying for too much credit in a short space of time can look like a red flag.

- Length of Credit History: A longer history of responsible credit use is always a good thing.

Your credit report is the detailed story behind your score. It’s absolutely crucial to check your report for free from one of the major credit reporting agencies in Australia to make sure everything is accurate before you even think about applying for a loan.

Finding and fixing errors or taking steps to improve your score can put you in a much stronger position when it's time to negotiate. Simple moves like paying down high-interest credit card debt, making sure every bill is paid on time, and holding off on new credit applications in the months before you apply for a mortgage can make a huge difference. At the end of the day, a better score means a better deal.

Calculating Your Deposit and Upfront Costs

While your deposit is the headline act, it’s really just one piece of the home-buying puzzle. Focusing only on the deposit is a bit like budgeting for a plane ticket but forgetting about accommodation and food—sure, you’ll get there, but you’re in for a few nasty surprises. Getting a clear picture of the total upfront cost is essential before you even think about applying for a home loan.

The magic number everyone talks about is a 20% deposit. This has long been the gold standard because it lets you sidestep Lenders Mortgage Insurance (LMI). LMI is a one-off insurance premium that protects the lender, not you, if you can't keep up with your repayments. It’s usually required when your deposit is less than 20% of the property’s price. Our guide on understanding the Loan-to-Value Ratio explains this concept in more detail.

But don’t panic if a 20% deposit feels like a mountain you can’t climb. There are a number of government schemes, like the First Home Guarantee, designed to help eligible buyers get into the market with a smaller deposit, often without needing to pay for LMI.

Beyond the Deposit: The Other Expenses You Can't Forget

Your savings goal needs to cover several other major costs that pop up during the buying process. These aren’t optional extras; they need to be paid upfront, so it’s crucial to factor them in from day one.

- Stamp Duty: This is a state government tax on the property purchase, and it’s often the biggest extra cost you’ll face.

- Legal and Conveyancing Fees: You need a professional to handle the legal transfer of the property title, which can set you back a few thousand dollars.

- Building and Pest Inspections: These checks are absolutely vital. They ensure you’re not about to buy a home with hidden structural issues or a termite problem.

It’s a good rule of thumb to budget an extra 5% of the property’s purchase price to cover all these additional expenses. This buffer ensures you’re not caught short when the invoices start rolling in.

This kind of detailed financial planning is especially important right now. As of mid-2024, a staggering 98.2% of new home loans are on variable rates, meaning borrowers have to be ready for their repayments to change. You can find out more about the current Australian home loan statistics on Mozo to get a better handle on the market landscape.

Local Market Factors in Mandurah and WA

While the core documents you need for a mortgage are pretty much the same across Australia, your local property market plays a massive role in shaping your home-buying journey. For anyone looking to buy in Mandurah and the wider Western Australia region, getting your head around these specific factors is the key to setting realistic goals and making a competitive offer.

It’s simple, really: the value of properties in the Peel region directly impacts the size of the loan you’ll need to secure. A higher median house price naturally means you'll need a larger deposit and a bigger mortgage. This local context is crucial when you're figuring out how much you can comfortably borrow.

WA Specific Advantages and Trends

Fortunately, there are state-specific programs designed to give local buyers a leg up. The WA First Home Owner Grant (FHOG) can provide a serious boost to your deposit if you’re building or buying a new home, making it that much easier to get your foot on the property ladder. Staying informed about how to get a home loan in WA can uncover other local opportunities you might not know about.

It’s also smart to keep an eye on the bigger picture. Across Australia, the average mortgage for an owner-occupier was sitting around $631,000 in mid-2025, but this number swings wildly from state to state. For instance, New South Wales has the highest average at a whopping $816,000, while Tasmania’s is the lowest at $481,000. These differences really drive home how much local prices affect what you’ll need for a mortgage. You can find more insights on these national trends over at loans.com.au.

By digging into recent sales in Mandurah and getting a feel for current buyer demand, you can build a much more strategic and realistic budget. This local knowledge ensures you're not just ready on paper—you’re prepared for the reality of the market you're actually buying into.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following the style of the provided examples.

A Few Last-Minute Mortgage Questions

As you get closer to applying for a home loan, a few final questions always seem to pop up. It’s completely normal. Here are some quick, straightforward answers to help you tie up any loose ends and step forward with confidence.

How Long Does Mortgage Pre-Approval Take?

This one can be surprisingly quick. Generally, you’re looking at anywhere from a few days to a couple of weeks for pre-approval to come through. The biggest variable is how organised you are. If you have all your documents ready to go from day one, it can really speed things up on the lender's end.

Can I Get a Mortgage With a Small Deposit?

Absolutely. It’s definitely possible to secure a mortgage with less than the standard 20% deposit. The main thing to be aware of is that you'll almost certainly have to pay for Lenders Mortgage Insurance (LMI). It's also well worth checking out government programs like the First Home Guarantee. For eligible buyers, these schemes can be a game-changer, allowing you to buy a home with as little as a 5% deposit without the added cost of LMI.

Does Applying for Multiple Mortgages Hurt My Credit Score?

Yes, it can, so it pays to be strategic. Every time you submit a formal mortgage application, the lender performs a 'hard inquiry' on your credit report. A few of these in a short space of time can temporarily dip your score. The smarter approach is to do your homework upfront, narrow down your choices, and then only apply to one or two lenders you’re genuinely serious about.

Ready to take the next step in your Mandurah property journey? David Beshay Real Estate offers expert guidance and free property appraisals to help you make informed decisions. Visit us online to use our free mortgage calculators and see how we can help you achieve your goals.