A mortgage repayment calculator for Australia is an essential tool for anyone even thinking about buying a home. In simple terms, it takes your loan amount, interest rate, and loan term and gives you a clear estimate of your regular repayments. It instantly cuts through the bank jargon and tells you what your fortnightly or monthly commitment will actually look like.

This lets you budget properly before you sign on the dotted line for a home loan.

Why This Calculator Is Your Strongest Financial Ally

The interface is usually straightforward, as you can see from this CommBank calculator screenshot. You just plug in your numbers to get an instant repayment estimate.

Think of a mortgage calculator less like a number-cruncher and more like a strategic partner. It’s your financial sandbox, a place where you can play with different scenarios without any real-world risk. This is where you can test the waters before you take on what is likely the biggest financial commitment of your life.

By tweaking the numbers—the interest rate, the loan term, or even the repayment frequency—you get a powerful, firsthand look at how every little decision impacts your financial future. It puts you in the driver's seat.

Before you start using one, it helps to have your key numbers ready. This table breaks down what you'll need and why it matters.

Key Inputs for Your Mortgage Repayment Calculator

| Input Field | What It Means | Why It's Important |

|---|---|---|

| Loan Amount | The total amount of money you need to borrow after your deposit. | This is the foundation of the calculation. A higher loan amount means higher repayments. |

| Interest Rate (%) | The annual percentage rate the lender charges on your loan. | Even a small change here can drastically alter your total interest paid over the life of the loan. |

| Loan Term (Years) | The length of time you have to pay back the loan, typically 25 or 30 years. | A longer term means lower monthly payments but more interest paid overall. A shorter term is the opposite. |

| Repayment Frequency | How often you make payments (e.g., weekly, fortnightly, or monthly). | Paying fortnightly can help you pay off your loan faster because you make 26 payments a year instead of 12. |

| Extra Repayments | Any additional amount you plan to pay on top of your required repayment. | This is a powerful way to reduce your loan principal faster and save a significant amount on interest. |

Having these details handy will make the process much smoother and give you a far more accurate picture of your potential mortgage.

Gaining Clarity in a Complex Market

Let’s be honest, the Australian property market can feel overwhelming. Trying to figure out what you can realistically afford is a massive challenge. A calculator provides a solid, tangible starting point, turning huge loan amounts into simple weekly or monthly figures you can actually measure against your budget.

This clarity is vital before you even start scrolling through property listings or finalising your savings. On that note, our guide on using a house deposit calculator in Australia can also help you get ready for that first big hurdle.

With nearly 45% of Australians holding a mortgage, understanding these numbers has never been more critical. The average weekly repayment was around $493 in 2025, which shows just how much of our income goes towards housing. Tools that give you financial foresight are no longer a 'nice-to-have'—they're indispensable.

A mortgage calculator is what allows you to shift from pure guesswork to a data-driven strategy. It shows you the long-term impact of your choices today, like whether to go for a 25-year term over a 30-year one.

Building Confidence Through Scenarios

One of the biggest wins of using a repayment calculator is the freedom to model "what-if" scenarios. What happens if interest rates jump by 1%? How much faster could I own my home outright if I added an extra $200 a month? These aren't just hypotheticals; they're strategic questions that help you build a more resilient mortgage plan.

By running these simulations, you can:

- Stress-test affordability: Figure out a comfortable borrowing limit that can withstand potential rate hikes.

- See the savings: Get an exact dollar figure on how much interest you’d save by making extra repayments or shortening your loan term.

- Plan ahead: Prepare for life’s changes, ensuring your mortgage remains manageable no matter what comes your way.

This proactive approach gives you the confidence to not just get a mortgage, but to actively manage it from day one.

Translating Calculator Results into Real-World Insights

So, you’ve punched your numbers into a mortgage repayment calculator and now you’re staring at a screen full of figures. It’s easy to feel a bit overwhelmed, but this is actually where the magic happens. The real skill is translating those numbers into a plan that works for your life and budget.

The results give you a powerful, unfiltered look at your potential mortgage, breaking down what can feel like an impossibly large number into something you can actually wrap your head around. Let's dig into what those figures really mean for you.

Decoding Your Core Repayment Figures

The first number that jumps out is your estimated repayment amount—whether it's weekly, fortnightly, or monthly. This is your immediate reality check. It tells you exactly how much cash needs to be set aside from your bank account on a regular basis, forming the new cornerstone of your household budget.

But the real story is in the details. Any good calculator will split your repayment into two crucial parts:

- Principal: This is the good stuff. It's the part of your payment that actively chips away at your loan balance.

- Interest: This is the cost of the loan—the money that goes directly to the lender for the privilege of borrowing.

In the early years of a loan, it can be a bit of a shock to see just how much of your hard-earned money is going towards interest. It’s completely normal, but seeing it laid out in black and white is often the kick-start people need to think about paying their loan off faster.

The True Cost of Borrowing Revealed

Perhaps the most eye-opening number a calculator spits out is the total interest payable over the life of the loan. This single figure represents the genuine cost of borrowing that money. Seeing that a $650,000 loan could end up costing you over $500,000 in interest over 30 years really puts things into perspective.

It’s a stark reminder of why strategies like making extra repayments or opting for a shorter loan term can save you an absolute fortune. Every extra dollar you tip into the principal is a dollar that won't be racking up interest for the next 20 or 30 years. Getting the right loan from the start is paramount, and understanding your position with a home loan pre-approval brings critical clarity before you sign on the dotted line.

A great feature to look for is an amortisation schedule. This is a table that shows the principal and interest breakdown over time. You can actually pinpoint the 'tipping point'—that fantastic moment, often years down the track, when more of your repayment finally starts hitting the principal instead of the interest.

Applying It to a Real Australian Scenario

Let’s ground this with a realistic example. The average Australian mortgage was sitting around $631,000 as of June 2025. With property prices and home loan commitments on the rise, being able to accurately interpret your potential costs has never been more important.

Imagine you're looking at a $650,000 loan in Victoria. With an interest rate of 6.0% over a 30-year term, a calculator will estimate your monthly repayment to be around $3,897.

Here’s where the insight comes in:

- In your very first month, a staggering $3,250 of that payment is pure interest.

- A mere $647 actually goes towards reducing what you owe.

This kind of breakdown transforms an abstract loan into a concrete financial picture. It helps you grasp the long journey ahead and, more importantly, inspires you to find ways to shorten it.

Modelling Scenarios to Build a Resilient Mortgage Strategy

This is where a mortgage repayment calculator really shines, transforming from a simple estimator into your own personal financial lab. By running a few 'what-if' scenarios, you can build a mortgage strategy that’s not just affordable today but tough enough to handle whatever comes next. It’s all about preparing for the future instead of just reacting to it.

A proactive approach starts with knowing which variables you can control and which you can't. This lets you see the real-dollar impact of different choices, helping you craft a plan that fits your life, not the other way around.

Preparing for Interest Rate Fluctuations

For anyone on a variable rate loan, the biggest unknown is the future of interest rates. Decisions from the Reserve Bank of Australia (RBA) can directly hit your household budget. Instead of waiting for the news, you can model potential changes right now.

Let's run through a quick example. Say you have a $600,000 loan at an interest rate of 6.0%. Your monthly repayment comes out to $3,597. But what happens if rates move?

- Rate Rise Scenario: Punch 6.5% into the calculator. Your repayment jumps to $3,792. That's an extra $195 you'd suddenly need to find each month.

- Rate Cut Scenario: Now, drop the rate to 5.75%. The repayment falls to $3,496, saving you $101 monthly.

Running these simple tests gives you a clear financial picture. It helps you see if you have a comfortable buffer to absorb potential increases, which is a crucial step in making sure your mortgage stays manageable for the long haul.

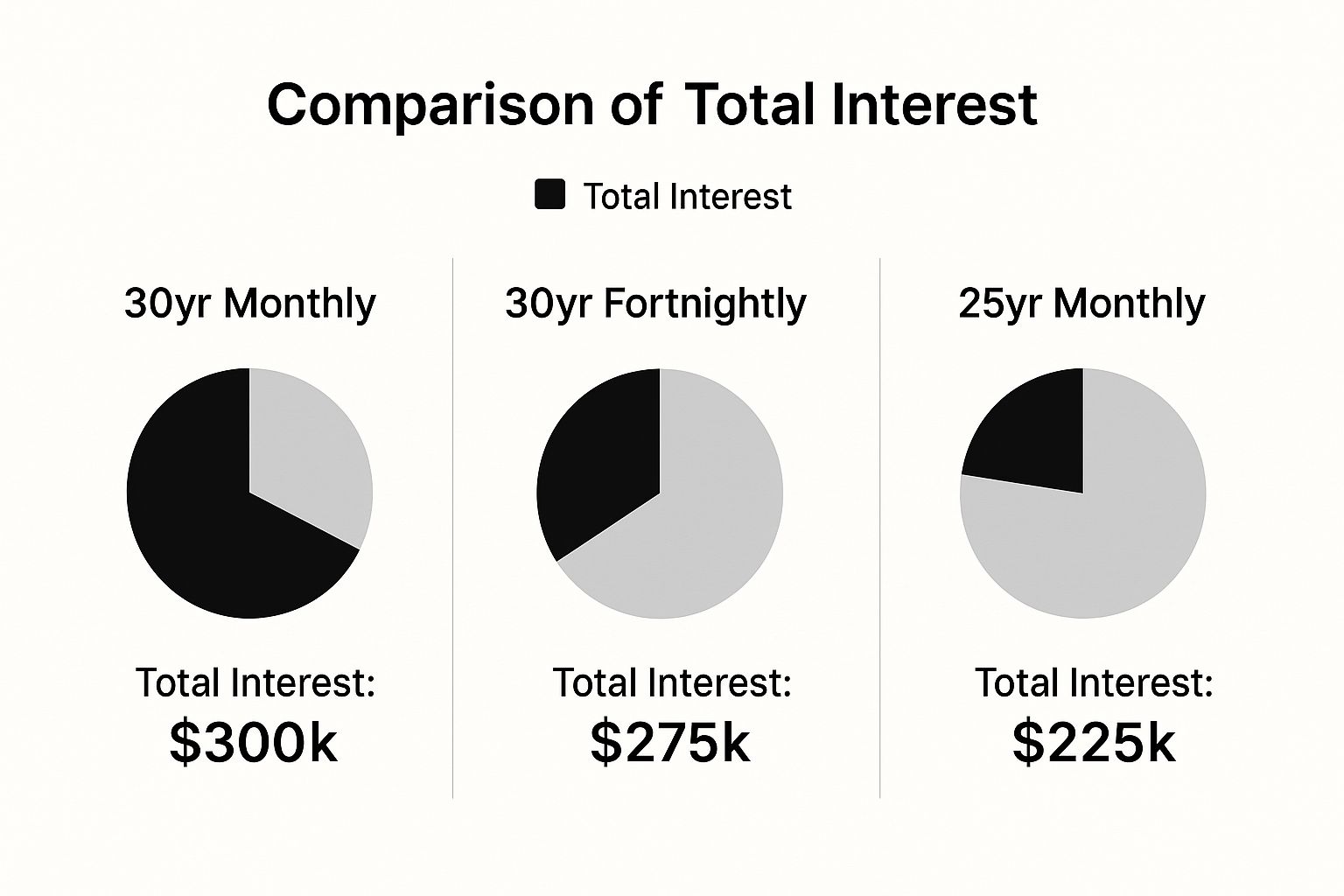

The Power of Shorter Loan Terms and Faster Payments

Another powerful strategy is to play around with your loan term or how often you make payments. While a 30-year term is pretty standard, shortening it or paying more frequently can lead to massive interest savings. This is where you can see the direct benefits of being disciplined.

The goal isn't just to pay the mortgage; it's to pay it off as efficiently as possible. A calculator reveals that small, consistent changes in your repayment habits compound into huge savings over time.

This is where you can really see the magic happen. Tweaking your repayment frequency can shave years and tens of thousands of dollars off your loan.

Impact of Repayment Frequency on a $600,000 Loan

Let's break down the numbers from the infographic with a clear comparison. On a $600,000 loan over 30 years at 6.0%, switching from monthly payments can have a dramatic effect.

| Repayment Frequency | Repayment Amount | Total Interest Paid | Loan Paid Off Faster By |

|---|---|---|---|

| Monthly | $3,597 | $695,027 | N/A |

| Fortnightly | $1,799 | $622,763 | 4 years and 7 months |

| Weekly | $899 | $621,992 | 4 years and 8 months |

The difference is staggering. Just by paying half the monthly amount every two weeks (fortnightly), you end up making one extra full monthly payment each year without really feeling it. This simple change on our example loan saves you over $72,000 in interest and gets you mortgage-free nearly five years sooner.

These kinds of strategies also have a positive impact on your financial standing, which can be important when considering factors like your loan to value ratio for future investments or refinancing. By experimenting with these scenarios, you're not just crunching numbers—you're building a smarter, more flexible mortgage plan.

Unlocking Savings with Extra Repayments and Offset Accounts

If modelling different rates and repayment frequencies shows you what’s possible, then exploring extra repayments is where you truly take control of your mortgage. This is, hands down, the most powerful way to chip away at your loan term and slash the total interest you'll end up paying.

Using a mortgage repayment calculator for Australia is the perfect way to see the massive long-term reward for this kind of financial discipline. You can pop different amounts into the "extra repayments" field to see the impact. Start small—you'll be surprised what a difference even a modest amount makes.

The Real-World Impact of Extra Contributions

Let’s put this into practice with a real-world scenario. Imagine you have a $500,000 home loan with an interest rate of 6.0% p.a. over a 30-year term. Your minimum monthly repayment works out to be $2,998.

Now, what if you decided to kick in an extra $100 a fortnight? That’s about the cost of a couple of takeaway meals. The calculator will show you something pretty amazing:

- You’d pay off your entire loan 4 years and 11 months earlier.

- You’d save a staggering $82,347 in interest.

This is the magic of compounding working for you, not against you. Every extra dollar goes straight off your principal balance, which means there's less debt for the bank to charge interest on for the rest of the loan's life.

Recent data shows that Aussies are incredibly proactive with their mortgages. In fact, a whopping 85% of home loan customers were ahead on their repayments in the 2025 financial year, holding an average buffer of 32 monthly payments. This disciplined approach, especially strong among first home buyers, shows a real commitment to getting ahead. You can explore more about these home loan repayment trends to get the full picture.

Factoring in an Offset Account

An offset account is another brilliant tool that works in a similar way to making extra repayments. It's basically a transaction account linked to your mortgage, where every dollar in it is 'offset' against your loan principal. This means you’re only charged interest on the net amount (your loan balance minus your offset balance).

While many calculators don't have a specific field for an offset account, you can easily simulate its effect.

Pro Tip: Figure out the average balance you expect to consistently keep in your offset account. Then, simply subtract this amount from your total loan principal in the calculator. This will give you a very close estimate of the interest savings and show you how much faster you could be mortgage-free.

For instance, if you have that $500,000 loan but plan to maintain $50,000 in your offset, just run the numbers with a $450,000 loan amount. The results will highlight the huge reduction in interest paid over the life of the loan, proving just how valuable it is to make your savings work harder for you.

Common Calculator Mistakes and How to Avoid Them

A calculator is only as reliable as the numbers you put into it. It's a fantastic tool, no doubt, but a few common mistakes can give you a dangerously optimistic view of what you can afford. This can lead to some serious budget stress down the track.

Getting the inputs right from the get-go is the key to building a financial plan based on reality, not just a best-case scenario. Let's walk through the most frequent errors I see and how you can easily sidestep them.

Forgetting About Lenders Mortgage Insurance

This is probably the biggest oversight for first-time buyers: completely forgetting about Lenders Mortgage Insurance (LMI).

If your deposit is less than 20% of the property's value, you’ll almost certainly have to pay this one-off insurance premium. It can be a hefty cost, often running into thousands of dollars, and it’s usually just tacked onto your total loan amount.

Imagine you add a $15,000 LMI premium to a $500,000 loan. Your actual borrowing amount is now $515,000. If you don't include this in your calculation, your repayment estimate will be lower than what you'll really be facing. Always try to get an LMI quote and add it to your loan principal for an accurate figure.

Using the Headline Rate Instead of the Comparison Rate

Lenders love to advertise a flashy, low "headline" interest rate to catch your eye. The thing is, this number doesn't tell the whole story. The comparison rate is the figure you should be paying attention to for a more realistic calculation.

By law, Australian lenders have to display a comparison rate. This rate includes the interest rate plus most of the upfront and ongoing fees. Using this gives you a much truer reflection of the loan's actual cost and a more accurate repayment estimate.

This simple switch can make a noticeable difference in your estimated repayments and, more importantly, the total interest you'll pay over the life of the loan.

Ignoring Other Upfront and Ongoing Costs

A standard calculator is great for repayments, but it won’t factor in all the other costs that come with getting a mortgage. If you haven't accounted for these elsewhere, they can seriously skew your budget.

Make sure you've set money aside for costs that a calculator won't show you, including things like:

- Establishment Fees: A one-time charge from the lender just to set up your loan.

- Annual Package Fees: Many loans with handy features like offset accounts come with an annual fee, often around the $395 mark.

- Valuation Fees: The cost for the bank to send someone out to assess the property's value before they approve your loan.

- Conveyancing and Legal Fees: These are the costs for all the legal work involved in transferring the property ownership over to you.

These expenses won't change your regular repayment amount, but they are significant upfront costs that need a place in your overall budget. Overlooking them can create a lot of financial strain right at the beginning of your home ownership journey.

By being aware of these common pitfalls, you can make sure your calculations are spot-on and your financial planning is built on solid ground.

Got Questions About Your Mortgage Calculator?

It's completely normal to have a few questions pop up, even when using the best tools. After all, we're talking about some of the biggest financial decisions you'll ever make. This section is here to clear up the most common queries people have when using a mortgage repayment calculator in Australia.

Think of it as a final check-in, a place to get straight answers so you can move forward with total confidence.

How Accurate Is a Mortgage Repayment Calculator?

These calculators are remarkably good at giving you a close estimate, but it's crucial to remember they're a guide, not a final quote. The figures are fantastic for budgeting, comparing different loan scenarios, and getting a feel for what you can afford.

The final repayment amount from your lender might be slightly different. Why? It could be due to small things like the exact settlement date changing the first interest calculation, or specific fees attached to your loan product. For your financial planning, treat the result as a very reliable approximation.

Should I Use the Interest Rate or Comparison Rate?

For the most realistic picture of what you'll actually pay, always use the comparison rate when you can. It’s a non-negotiable for smart planning.

The standard interest rate only tells part of the story – it's just the interest on the money you borrow. The comparison rate, on the other hand, is a legal requirement in Australia for a very good reason. It bundles in the interest rate plus most of the upfront and ongoing fees, giving you a much truer sense of the loan's cost. This translates to a more honest repayment figure.

Using the comparison rate helps you avoid nasty surprises down the track. It shifts your calculation from a simple interest estimate to a genuine cost projection, which is exactly what you need for a household budget that's built to last.

Can I Use This Calculator to Compare Fixed vs Variable Loans?

Absolutely. This is one of the most powerful ways to use a mortgage repayment calculator in Australia. You can easily run two separate calculations to see a side-by-side comparison of your initial repayments.

Here’s a practical way to do it:

- Fixed-Rate Loan: Pop in the advertised fixed rate and the fixed term (e.g., 2 years at 5.5%). This will show you your exact repayment amount for that initial period.

- Variable-Rate Loan: Use the current variable rate. This shows you what your repayments would look like today.

- Stress-Test It: To see how you'd cope with potential RBA cash rate changes, try rerunning the variable calculation with the rate bumped up by 1-2%. This is a great way to see if you could still comfortably manage the repayments if rates were to rise.

What if the Calculator Lacks an Extra Repayments Feature?

No problem. If a more basic calculator doesn't have a specific field for extra repayments, you can still get a feel for the impact of paying more. It just takes one simple step.

First, work out your standard minimum repayment based on the loan amount, term, and interest rate. Then, just add your desired extra amount on top. For instance, if your minimum monthly repayment is $3,000 and you want to chip in an extra $200, your new target repayment is $3,200.

While a basic tool won't show you the long-term interest savings, you can use this higher figure to confirm your budget can handle the commitment.

Planning your next move in the Mandurah property market takes more than just numbers; it demands local expertise and a solid strategy. At David Beshay Real Estate, we combine powerful tools with in-depth market knowledge to help you achieve your property goals. Whether you're buying your first home or selling a cherished property, get in touch for a personalised consultation and a free, accurate property appraisal today at https://realestate-david-beshay.com.au.