If you're a homeowner in Australia, you've probably heard the term 'property equity' thrown around. But what does it actually mean for you and your finances?

Put simply, property equity is the slice of your home that you truly own. It’s the current market value of your property minus whatever you still owe on your mortgage. Think of it as your genuine financial stake in the bricks and mortar.

Unlocking Your Property's Hidden Value

Imagine your home is a bit like a savings account. Every single mortgage repayment you make is a deposit, slowly but surely increasing your ownership stake. At the same time, the broader property market is doing its own thing in the background, hopefully increasing the total value of your home.

Your equity is the portion of that total value that belongs entirely to you—no strings attached to the bank. It's one of the most important concepts in Australian homeownership and a fantastic indicator of your financial health.

Getting your head around property equity is the first real step toward building long-term wealth through real estate. This guide is here to cut through the jargon and make this powerful concept crystal clear. We'll start with the basics and build up to practical strategies you can use.

What You Will Learn

This article will walk you through everything you need to know about property equity, so you can feel confident and in control. You’ll discover:

- How to Calculate Your Equity: A straightforward formula to figure out your exact ownership stake.

- Why Equity Matters: It's more than just a number; it's a critical financial tool you can use.

- What Makes It Grow: The key market forces and personal actions that can increase (or decrease) your equity.

- Strategies to Build Equity Faster: Practical tips to help you build wealth through your property more quickly.

Before you can do anything else, you need a realistic idea of your home's current market value. The best way to get an accurate figure is to get some expert advice on what is a property appraisal from a qualified professional.

By the time you finish this guide, you won't just understand what your equity is—you'll know exactly how to manage it and make it grow.

How to Calculate Your Home Equity

Figuring out your home equity doesn't require complex financial wizardry; it all comes down to a simple, powerful formula. Getting this number right is the first step to understanding your financial position and unlocking the wealth tied up in your property.

At its core, the principle is just subtracting what you owe on the mortgage from what your home is currently worth. That final figure is your equity—the slice of the property you genuinely own.

The Home Equity Formula:

Current Market Value of Your Property – Outstanding Mortgage Balance = Your Home Equity

This straightforward equation gives you a clear snapshot of your ownership stake. Let’s break down how to find each of these numbers so you can get an accurate picture.

Finding Your Property's Current Market Value

Working out what your property could realistically sell for in today's market is the most important part of this whole calculation. A wild guess just won't cut it; you need a solid figure based on current conditions.

Here are a few reliable ways to pin down your property's value:

- Professional Appraisal: This is the gold standard. A licensed valuer will give you the most accurate and legally recognised valuation by looking at your home's condition, unique features, and recent comparable sales in the area.

- Real Estate Agent Estimate: An experienced local agent can put together a comparative market analysis (CMA). They have their finger on the pulse of what buyers are willing to pay in your suburb right now.

- Online Valuation Tools: Websites like CoreLogic and Domain offer quick, automated estimates. These are great for a ballpark figure, but remember, they can't see the new kitchen you installed or the specific condition of your home.

Identifying Your Outstanding Mortgage Balance

This part is much simpler. Your outstanding mortgage balance is the total amount you still owe the bank. It’s not just the principal amount you borrowed; it also includes any interest or fees that have been added to the loan along the way.

You can usually find this exact figure by:

- Logging into your online banking portal.

- Checking your most recent mortgage statement.

- Giving your lender a call and asking for a payout figure.

It’s crucial to use the most up-to-date balance for an accurate equity calculation. This number is directly tied to your lender's stake in the property, which is often measured by something called the Loan to Value Ratio. To get a better handle on this, you can learn more about what the Loan to Value Ratio is and how it affects your finances.

The incredible growth in property values across Australia is giving homeowners a massive equity boost. The total value of residential homes recently smashed records, hitting $11.564 trillion, with the average home price climbing to $1,016,700. As property values rise, so does your equity—especially if you're chipping away at your mortgage at the same time. You can dig into these trends in the latest national property value data.

Why Your Equity Is a Powerful Financial Tool

Once you get your head around how to calculate your equity, you can start seeing it for what it really is. It’s not just a number on a page; it’s one of the most powerful financial tools you’ll ever own.

This is the hidden wealth in your home, acting as both a financial safety net and a launchpad for your next big move. It’s the point where your property stops being just a place to live and starts working for you as an active financial asset.

Instead of just letting that value sit there, you can put it to work to improve your financial situation. Many Aussies use their home equity to fund renovations, pay off higher-interest debts, or even stump up the deposit for an investment property. It’s an incredibly versatile resource that can help you hit some major life goals.

The concept of using your equity is often called leveraging. Think of it like this: you’re strategically borrowing against the portion of the home you already own, unlocking its cash value without having to sell up. This gives you access to funds at a much friendlier interest rate than you'd ever get with a personal loan or credit card.

Unlocking Your Equity with Financial Products

So, how do you actually get your hands on this value? Lenders have specific products designed for this exact purpose, allowing you to tap into the wealth you've built over time. While the details can vary, they all work on the same basic principle: lending you money that’s secured against your home's equity.

Two of the most common options you’ll come across in Australia are:

- Home Equity Loans: This is a lump-sum loan you get upfront. You then pay it back in regular instalments over a set period. It's a great fit for big, one-off expenses like a major kitchen renovation or the deposit on an investment unit.

- Home Equity Line of Credit (HELOC): This works more like a credit card. You get approved for a certain credit limit and can draw on those funds as you need them, only paying interest on the amount you’ve actually used. It offers far more flexibility for ongoing projects or as a handy emergency fund.

It’s crucial to remember that leveraging your equity means taking on more debt. While it's a fantastic tool for building wealth, you absolutely need a clear repayment plan and a solid understanding of the risks before you dive in.

Equity Growth in the Australian Market

A healthy property market is the engine that drives equity growth, creating significant wealth for homeowners right across the country.

Recent data really brings this connection to life. Nearly 722,000 properties were settled across Australia’s mainland states, a 3.2% jump in activity from the previous year. Even more telling, the total value of these settlements skyrocketed to $726.6 billion—a massive 9.4% increase.

This surge in property values gives a huge boost to the equity of existing homeowners, cementing real estate as one of the main drivers of household wealth. You can dig deeper into these trends in the latest PEXA property market report.

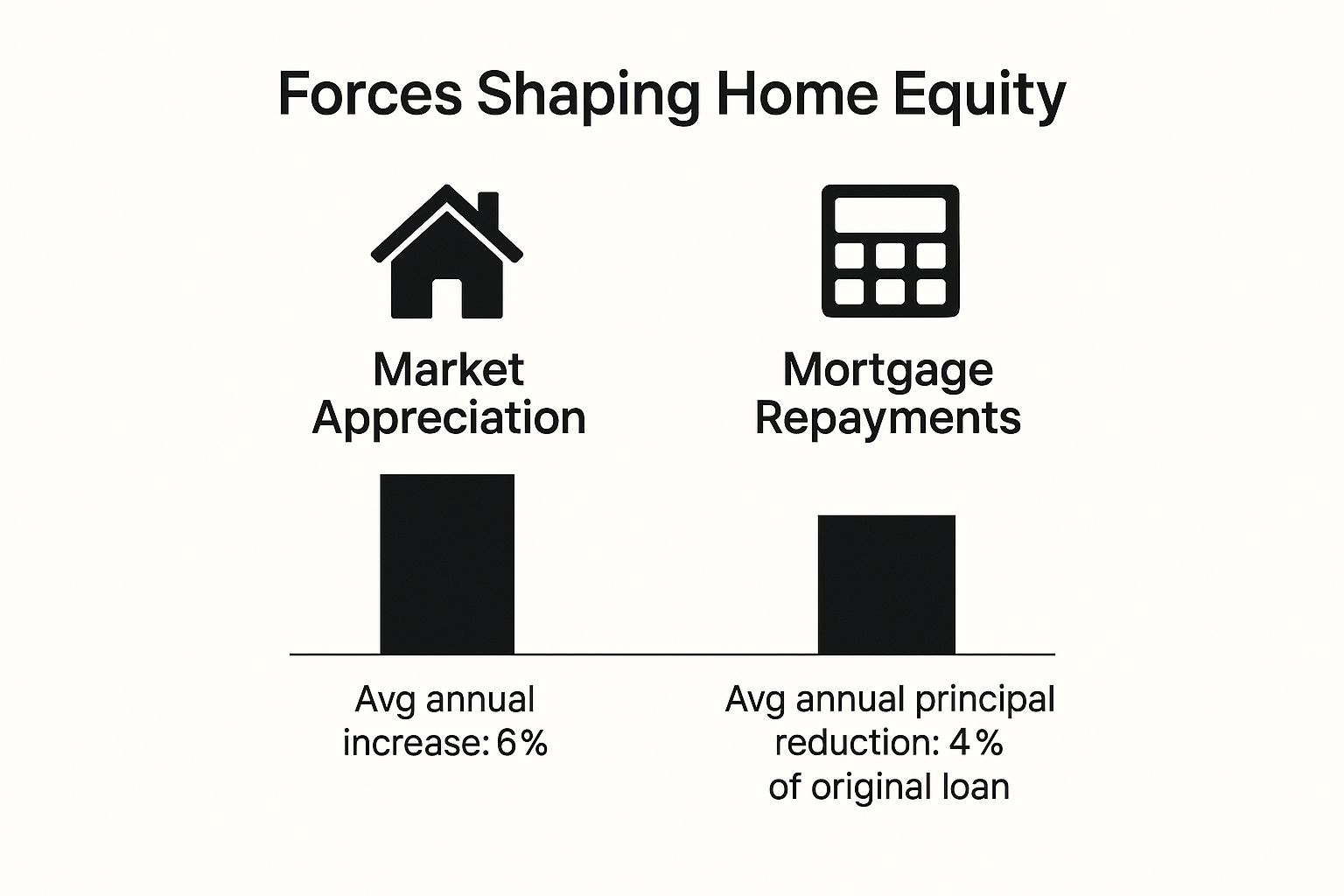

The Forces That Shape Your Home Equity

Think of your property equity not as a fixed number, but as something dynamic, constantly shaped by two powerful forces. One is the wider property market, which you can’t control. The other is entirely in your hands: your mortgage repayments.

Getting your head around how these two elements work together is the key to understanding your equity and, more importantly, how to make it grow. They act like two separate currents—one pushing your property’s value up and the other pulling your debt down. The ever-widening gap between them is your wealth.

On one side, you have market appreciation. This is the passive growth you get from things like supply and demand, interest rate changes, new local infrastructure, or your suburb simply becoming a more desirable place to live. A rising market can boost your equity significantly without you lifting a finger.

The Two Sides of the Equity Coin

The other, more direct influence is your mortgage. With every single repayment you make, a portion goes towards paying down the principal amount you borrowed from the bank. This is the active, hands-on way you build your ownership stake, directly chipping away at the bank's share of your home.

This infographic neatly shows how both market appreciation and your own mortgage repayments work in tandem to build your home equity over time.

As you can see, the combination of a rising property market and consistent mortgage payments creates a powerful wealth-building engine for homeowners.

The Australian property market gives us a perfect real-world example. With total outstanding housing loans recently hitting a staggering AUD 2.45 trillion, the debt side of the equation is massive. At the same time, however, median dwelling values rose by 6.55% year-on-year, showing just how effectively market appreciation can work to offset this debt and build wealth for homeowners. You can dive deeper into these Australian property market price trends to see these dynamics in action.

When Equity Goes the Wrong Way

It's also crucial to remember that equity isn't guaranteed to always go up. If property values take a significant dive, you could find yourself in a situation known as negative equity.

Negative equity, sometimes called being "underwater," happens when your outstanding mortgage balance is higher than the current market value of your property.

This scenario might occur if you buy at the very peak of a market just before a sharp downturn, or if you borrow a very high percentage of the property’s value. While it’s not common in Australia, it highlights the risks involved and really drives home why building a healthy equity buffer is so important for your long-term financial security. That buffer acts as your shield against market swings you simply can't control.

Proven Strategies to Build Your Equity Faster

Knowing what equity is is the first step, but actively growing it is where you start building real wealth. The good news is, you’ve got two powerful levers you can pull to make it happen faster. You can either shrink the amount you owe the bank or you can boost the value of your home.

Both paths are effective, but they’re suited to different goals and financial situations. Let’s dive into the most reliable strategies so you can figure out which one is the right fit for you.

Pay Down Your Mortgage Sooner

The most straightforward way to build equity is to get ahead on your mortgage. Every extra dollar you pay over your minimum repayment goes straight towards cutting down your principal. Think of it as a guaranteed, risk-free return on your investment.

There are a few clever ways to do this:

- Make Extra Repayments: Even small, one-off payments from a tax refund or a work bonus can shave years off your loan and save you thousands in interest.

- Switch to Fortnightly Payments: This is a simple but effective trick. By paying half your monthly amount every two weeks, you’ll sneak in one extra full month’s repayment each year without really feeling the pinch.

- Use an Offset Account: An offset account is a transaction account linked directly to your mortgage. The money sitting in that account reduces the loan principal you’re charged interest on, helping you pay the loan down much faster.

Each of these methods steadily chips away at the bank’s share of your property, giving you a bigger slice of the pie with every payment.

Increase Your Property’s Market Value

The other main strategy is to take matters into your own hands and increase what your home is actually worth. While you can't control the broader property market, you can make smart improvements that add real, tangible value and catch the eye of future buyers. It’s all about investing in your asset to get a return.

The goal isn’t just to renovate; it’s to renovate for profit. A successful project should add more to your home’s sale price than it cost you to complete, creating instant equity.

But not all renovations are created equal. Some give you a much better bang for your buck than others. Simple cosmetic updates—like a fresh coat of paint, new flooring, or modern light fixtures—offer a fantastic return. Bigger upgrades to kitchens and bathrooms are also classic value-adders, as they’re the rooms that buyers focus on most. For a full rundown on which projects deliver the best results, you can learn more about how to increase home value with strategic upgrades.

To help you weigh your options, here’s a quick comparison of the two main approaches.

Comparing Equity-Building Strategies

| Strategy | How It Works | Pros | Cons |

|---|---|---|---|

| Pay Down Mortgage | Making extra or more frequent repayments to reduce the principal loan amount faster. | Guaranteed, risk-free return. Reduces interest paid over the life of the loan. Builds disciplined financial habits. | Requires available cash flow. Returns are steady but can be slow. Doesn't increase the property's market value. |

| Increase Property Value | Making strategic renovations and improvements to boost the home's market price. | Potential for high, fast returns. Can improve your lifestyle while you live there. Creates instant equity if done right. | Involves risk—no guarantee of profit. Requires significant upfront investment. Can be time-consuming and stressful. |

Ultimately, choosing the right strategy comes down to your personal financial situation. Paying down your debt offers certainty and peace of mind. Renovating, on the other hand, carries the potential for much higher returns, but also comes with risk.

Many savvy homeowners find a sweet spot by using a combination of both. They consistently pay down their loan while making strategic improvements over time, maximising their equity growth from every angle.

Clearing Up Common Home Equity Misconceptions

It’s easy to think of home equity as a kind of magic piggy bank, but a few common myths can lead to some pretty costly financial mistakes. These misunderstandings often oversimplify how equity actually works in the real world.

Let's clear the air and debunk a few of the most persistent fallacies so you can make smarter decisions with your biggest asset.

Myth 1: Your Equity Is the Same as Cash

This is probably the biggest trap homeowners fall into. While your equity represents real value, it's not liquid. You can't just wander down to an ATM and withdraw it like you would from a savings account.

Accessing that value means going through a formal financial process, like selling the property, refinancing your mortgage, or taking out a home equity loan. Each of these steps involves applications, credit checks, and approvals.

Your home equity is a powerful asset, but it is fundamentally illiquid. It represents potential value tied up in a physical asset, not cash you can spend freely on a whim.

Understanding this distinction is crucial for sound financial planning. Relying on your equity for an emergency fund without a clear and quick way to access it could leave you in a very tight spot when you need cash fast.

Myth 2: Every Renovation Adds Value

Another popular belief is that any money you pour into home improvements will automatically boost your equity by the same amount, or even more. If only it were that simple.

While a slick new kitchen or a modern bathroom renovation often provides a great return on investment, not all upgrades are created equal. Some projects just don't add the dollar-for-dollar value you might expect.

Here are a few common ways people get it wrong:

- Over-capitalising on your suburb: Installing ultra-luxury Italian marble benchtops in a neighbourhood of modest brick-and-tile homes is unlikely to pay off.

- Highly personalised changes: That bright purple feature wall might be your dream, but it could be a nightmare for potential buyers who just see a project they have to fix.

- Invisible upgrades: A brand-new plumbing system is essential for a home's health, but it won’t add the same "wow" factor or perceived value as a cosmetic update that buyers can actually see.

Myth 3: You Can Borrow Against 100% of Your Equity

Finally, many homeowners assume they can borrow against their entire equity stake. Lenders will almost never let this happen.

Banks typically cap borrowing at 80% of your property’s total value, a figure known as the Loan to Value Ratio (LVR). This 20% buffer protects both you and the lender from a sudden drop in property prices. It means that, for lending purposes, the last 20% of your equity is effectively locked away and can't be borrowed against.

Your Property Equity Questions Answered

Getting your head around homeownership means you’ll inevitably bump into questions about property equity. It’s a term that gets thrown around a lot, but what does it actually mean for you? Here are some straightforward answers to the questions we hear most often from homeowners right here in Australia.

What’s the Difference Between Total and Usable Equity?

Think of total equity as the big picture – it’s your entire ownership stake in your home. You simply take the current market value of your property and subtract whatever you still owe on your mortgage. That final number is your total equity, representing your wealth on paper.

But then there's usable equity. This is the slice of your total equity that a lender will actually let you borrow against. In Australia, banks typically want you to keep a 20% buffer of equity in your home. This means you can usually access up to 80% of your property's value, less what you still owe. It's the practical, real-world amount you can tap into for things like renovations or buying an investment property.

How Long Does It Take to Build Meaningful Equity?

Building a solid chunk of equity doesn’t happen overnight; it’s more of a marathon than a sprint. For most homeowners, it takes roughly five to seven years to build up a meaningful stake. This happens through a mix of consistently paying down your mortgage and, hopefully, the property market giving you a helping hand through appreciation.

Of course, this timeline isn't set in stone. If you're in a booming property market or you're aggressively making extra repayments on your loan, you can definitely speed things up.

Can My Home Equity Go Down?

Yes, absolutely. Your equity isn’t a one-way street. If the property market takes a significant dip and your home's value falls, your equity will decrease right along with it. If the value drops to a point where it's less than what you owe the bank, you find yourself in a tricky situation known as negative equity.

This is precisely why building a healthy equity buffer over time is so important. It acts as a financial cushion, protecting you from those market ups and downs that are completely out of your control.

Ready to figure out your own property's value and equity potential? As a dedicated real estate professional in Mandurah, David Beshay Real Estate offers free, no-obligation property appraisals to give you the clarity you need. Visit us at https://realestate-david-beshay.com.au to book yours today.