So, you're thinking about buying a land and house package in Mandurah? It's a fantastic move. Finding the right spot in one of WA's most loved coastal cities is the first real step towards the lifestyle you’ve been dreaming of. This guide is your roadmap—no jargon, just practical advice to see you through from that first online search to the day you get the keys.

Your Guide to Buying in Mandurah

Mandurah is so much more than just a pretty face. It's a buzzing property market packed with opportunities, whether you're a first-home buyer, a family needing more space, or a savvy investor. The mix of relaxed canal living, quiet suburban streets, and solid infrastructure makes it a real gem in the Peel region.

Maybe it's the waterfront lifestyle calling your name, or perhaps the potential for great capital growth. Whatever your reason, this guide will give you the essential know-how for a smart, successful purchase.

We’re going to get straight to the point with clear, actionable steps. It's about moving past endless scrolling and getting into the nitty-gritty of making a confident property decision.

What This Guide Covers

We'll walk through the whole process together, breaking it down into easy-to-manage stages. You’ll learn exactly how to:

- Find and Assess Properties: We’ll cover the best ways to search and what to look for that isn’t in the glossy photos. Think land orientation, council rules, and all the small details that matter.

- Get Your Finances in Order: You need to understand loan pre-approval inside and out, uncover those sneaky hidden costs like stamp duty, and create a budget that actually works.

- Negotiate Like a Pro: Learn how to put forward a strong offer, get your head around the WA Offer and Acceptance contract, and make sure your interests are always protected.

- Nail the Settlement Process: We'll clear up any confusion about the final stretch, from that crucial pre-settlement inspection to finally popping the champagne in your new home.

A great property purchase isn't about getting lucky—it's about being prepared. When you understand the local market and every step of the buying journey, you can jump on the perfect opportunity without hesitation.

Whether you're eyeing an established home or thinking about building from scratch on a fresh block, this guide lays the foundation you need. And if you're still weighing up your options, you might find our detailed look at land for sale in Mandurah WA versus buying an existing house really helpful.

How to Find and Evaluate Your Ideal Mandurah Property

Finding the perfect land and house for sale in Mandurah isn't just about scrolling through the big property websites. Sure, they're a great place to start, but the real gems are often uncovered when you dig a little deeper and start thinking like a local.

The secret? Building relationships with local real estate agents who are truly plugged into the community. An agent with their ear to the ground often gets wind of properties before they even hit the market. Getting access to these "off-market" or "pre-market" listings gives you a huge advantage, letting you view and make an offer without the usual rush of competition.

Expanding Your Property Search

To get a real feel for what's out there, you need to cast a wide net. Don't put all your eggs in one basket; a multi-channel approach is always best.

- Tap into Local Agent Networks: Get in touch with a Mandurah-based agent and ask to be added to their buyer database. They’ll be able to flag properties that tick your boxes, including ones you won’t see advertised anywhere else.

- Explore on Foot (or by Car): Take a drive through the neighbourhoods that catch your eye, whether it's the family-friendly vibe of Lakelands or the coastal charm of Halls Head. You’d be surprised how many great finds are just sitting there with a simple "For Sale" sign out front, yet to be listed online.

- Set Up Smart Alerts: Get specific on the property portals. Create detailed alerts for must-haves like a certain block size, a north-facing backyard, or canal frontage. This cuts through the noise and delivers only the most relevant listings straight to your inbox.

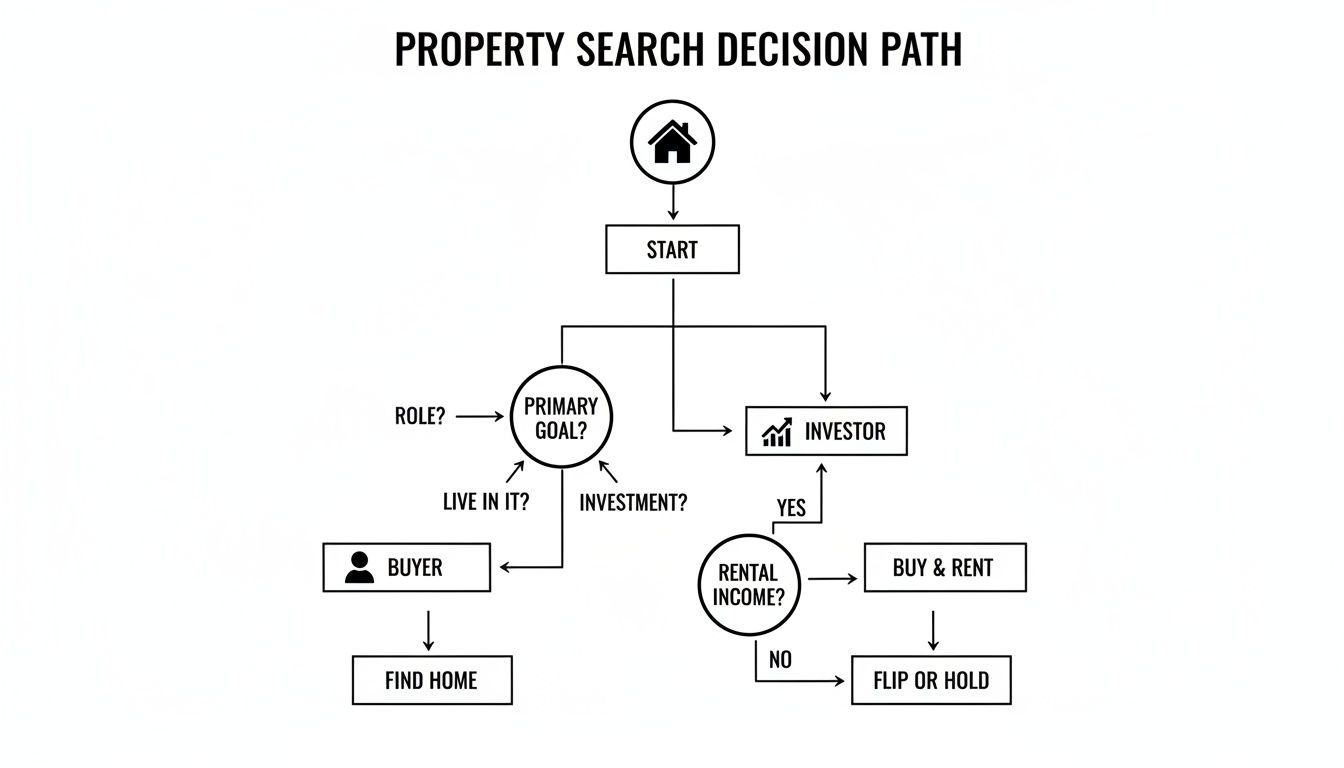

This decision tree shows how a homeowner's search path can differ from an investor's right from the get-go.

While both start by defining their goals, you can see how their evaluation criteria quickly split off, highlighting why a personalised search strategy is so important.

Your Essential Evaluation Checklist

Okay, you’ve shortlisted a few properties. Now it’s time to look past the glossy photos and clever staging. A thorough, hands-on evaluation is what separates a good buy from a potential money pit. You need to look at both the house and the land with a critical eye.

For the house, look beyond the fresh paint. Keep an eye out for the little things—subtle signs of wear and tear, especially issues common in coastal areas like corrosion on metal fittings or any hint of dampness. What about the structure itself? Are there any visible cracks in the walls? How old does the roof look? These are the kinds of problems that can balloon into very expensive repairs later on.

And don't forget the land. The orientation of the block, for instance, dramatically affects natural light and your future power bills. A north-facing rear is the gold standard in Australia, maximising that beautiful winter sun while keeping the harsh summer heat at bay.

Before you start your search, it helps to understand what each of Mandurah's popular suburbs has to offer. This table gives you a quick snapshot to see which area might be the best fit for your lifestyle.

| Suburb | Typical Property Type | Key Amenities | Best For |

|---|---|---|---|

| Halls Head | Coastal homes, family houses | Beaches, Halls Head Central, schools | Beach lovers and families |

| Lakelands | Modern family homes, new builds | Lakelands Shopping Centre, new schools, parks | Young families and first-home buyers |

| Dudley Park | Canal-front properties, older brick homes | Estuary access, Mandurah Forum, hospital | Boating enthusiasts and retirees |

| Falcon | Beach shacks, modern coastal homes | Falcon Bay Beach, Miami Plaza, estuary | A relaxed, holiday-feel lifestyle |

| Wannanup | Luxury canal homes, modern estates | The Cut Golf Course, Port Bouvard Marina | Upsizers and water sports lovers |

Each suburb has its own unique character and advantages. Figuring out which one aligns with your long-term goals is a crucial first step.

Digging into the Details

A proper assessment goes deeper than what you can see during a 20-minute home open.

- Council Regulations and Zoning: Get in touch with the City of Mandurah to check for any zoning restrictions or upcoming development plans. You'll want to know if the property is in a bushfire-prone zone or if there are any easements on the title that might limit what you can do with the land.

- Future Growth Potential: Do some research on the suburb's trajectory. Are there new infrastructure projects in the pipeline, like schools, shopping centres, or improved transport links? Buying in an area with solid growth indicators is key to seeing good capital appreciation over time.

- Land and Site Considerations: If you’re thinking about building or extending, take a hard look at the block’s topography. A sloping block can add significant costs to a build. It’s also worth looking into the soil type, as this can affect everything from the foundation to your landscaping dreams.

Making a smart decision means looking at a property from every angle—balancing what it is today with what it could be tomorrow. For anyone still weighing up their options, getting your head around the pros and cons of building a home vs buying an established one can bring some much-needed clarity. When you do this level of due diligence, you’re setting yourself up to choose a property that doesn't just meet your needs now but serves as a fantastic asset for years to come.

Getting Your Finances in Order and Understanding the True Costs

That heart-pounding moment when you find the perfect property is incredible. But it's also the starting gun for the financial leg of the race. Getting this part right isn't about luck; it's all about solid preparation. And the best tool you have in your arsenal? Loan pre-approval.

Getting pre-approved before you even think about making an offer changes the game completely. It takes you from being a casual window shopper to a serious, qualified buyer. You’ll know exactly what your budget is, which stops you from falling for a place that's just out of financial reach.

More than that, it shows sellers you mean business. When they see you have your finances sorted, your offer carries far more weight, especially if you’re up against other buyers.

The Power of Pre-Approval

Think of pre-approval as your financial green light. A lender will comb through your income, expenses, and credit history to work out the maximum amount they’re prepared to lend you. While it's not a final, unconditional thumbs-up, it’s a very strong signal of your borrowing capacity.

Having this sorted early means you can move fast and with confidence when the right land and house for sale comes along. In a hot market, that speed can be the difference between locking in your dream home and watching someone else get the keys. For a deeper look at this vital step, check out our guide on securing home loan pre-approval and what it means for your property search.

Uncovering the Hidden Costs

The price you see on the listing is just the sticker price—it’s not the total amount you’ll pay. I’ve seen many first-time buyers get caught out by the extra expenses that pop up along the way. To avoid any last-minute stress, you need to budget for these from day one.

Understanding the full financial picture is non-negotiable. A detailed budget that accounts for every fee and tax ensures you have the funds ready when you need them, making the whole process from offer to settlement much smoother.

Here are some of the biggest costs you need to plan for:

- Stamp Duty: This is the big one. Known officially as Transfer Duty in Western Australia, it's a state government tax on property purchases and often the largest additional expense.

- Legal and Conveyancing Fees: You'll need a settlement agent or conveyancer to handle the legal paperwork for transferring the property title into your name.

- Building and Pest Inspections: Absolutely critical. These inspections can uncover hidden structural problems or pest issues before you’re locked in.

- Lender Fees: Your bank or mortgage broker might have loan application fees or property valuation fees.

- Moving Costs: Don't forget the practical side of things—budget for removalists and connecting your utilities.

Budgeting with Real Numbers

A good budget relies on real figures, not just guesses. This is where online tools become your best friend. A stamp duty calculator, for example, can give you a precise figure based on the purchase price and whether you’re eligible for any first-home buyer concessions.

In the same way, a mortgage calculator helps you see what your monthly repayments will look like. This lets you properly assess how the loan will fit into your day-to-day household budget, preventing any nasty shocks later on.

Tapping into Government Incentives

The government has several schemes designed to give people a leg up into the property market, and they can seriously cut down your upfront costs. It’s well worth your time to investigate if you qualify for any of these programs.

Government initiatives have been a real boost for market activity. For instance, the Australian Government expanded the First Home Guarantee scheme, lifting property price caps and making it easier for first-time buyers with a 5% deposit to get into the market. For those looking in Western Australia and Mandurah specifically, this has made home ownership a more achievable goal.

These incentives can change, so keeping up-to-date with the latest grants and concessions is a smart move. Getting your finances prepared and having a clear picture of all the costs involved will set you up for a confident and successful purchase.

Crafting Your Offer and Navigating the Contract

You’ve found it. The one. After all the viewings and checklists, you’re finally ready to make a move. This is where the real strategy begins, turning your interest from just another land and house for sale into a compelling offer the seller simply can’t ignore.

First things first, let's talk numbers. The asking price is a starting point, not the finish line. Your job is to figure out what the property is really worth in today's Mandurah market. This isn't about guesswork; it's about digging into "comps"—comparable sales. Look for similar homes in the same suburb that have sold in the last three to six months to get a feel for a realistic price bracket.

A good local agent is worth their weight in gold here. They can pull a detailed market analysis that accounts for the little things you might miss, like the home's specific condition or which side of the street it's on. This data-driven approach stops you from making an emotional offer and keeps your bid competitive.

Structuring an Offer That Gets Noticed

With your price in mind, it's time to put it all together. In Western Australia, this happens through a formal document called the Offer and Acceptance contract. It’s far more than just a number; it’s a whole package of terms designed to win over the seller.

The key pieces of your offer will be:

- The Price: The dollar amount you're offering to pay.

- The Deposit: Shows you’re serious and is typically paid once your offer is accepted.

- Settlement Date: This is the day you officially take ownership, usually 30 to 90 days out. A bit of flexibility here can be a surprisingly powerful negotiating tool.

- Conditions: These are your safety nets—clauses that must be met for the sale to go ahead.

The conditions you add are absolutely critical. They’re there to protect you and give you a way out if things aren’t as they seem.

Subject To Finance vs. Going in Unconditional

The most common condition by a country mile is the 'subject to finance' clause. This gives you a specific window, often 21 or 28 days, to get the final, unconditional thumbs-up from your lender for your home loan. It’s an essential safeguard. If for some reason the bank says no, you can walk away from the deal without losing your deposit.

On the flip side, in a hot market, a seller might be swayed by an unconditional or 'cash' offer, which has no finance clause. While this definitely makes your offer look stronger, it’s a high-stakes move. You should only ever consider making an unconditional offer if you are 100% certain your money is locked in. Backing out without that protection could see you forfeit your deposit and even face legal trouble.

A killer offer isn't always about the highest price. It’s about balancing your own protection with what the seller wants. Sometimes, favourable terms like a quick settlement can be more persuasive than a few extra thousand dollars.

It's helpful to know what's happening on a bigger scale. Nationally, residential sales recently hit 526,747, holding steady year-on-year and sitting 1.9% above the five-year average. But while those numbers show a solid market, places like Perth and Mandurah have been outperforming the pack, pointing to strong local demand that you'll feel during negotiations. You can get a sense of the broader market by exploring these national housing market trends.

Decoding the Contract and Adding Special Conditions

The standard WA Offer and Acceptance contract covers all the usual bases, but 'special conditions' are where you tailor the agreement to your specific purchase. This is your chance to address any unique concerns you have about the property.

For example, you could make the sale conditional on:

- A clean building inspection report: This lets you get a professional to check for any major structural problems.

- A clear timber pest inspection: Absolutely essential for sniffing out termites or other nasty pests.

- The sale of your current property: A must-have if you need the funds from your old home to buy the new one.

Let’s play out a real-world scenario. Imagine your building inspection on a beautiful property in Halls Head finds the hot water system is on its last legs. You don't have to walk away. Instead, you can use that report to negotiate. Your agent can go back to the seller and ask them to either replace the system before settlement or knock the cost of a new one off the purchase price. It’s a practical solution that turns a potential deal-breaker into a win-win.

Getting through the negotiation and contract phase is all about keeping a cool head and having a clear plan. If you understand the property's true value, structure your offer cleverly, and use special conditions to cover your bases, you’ll be well on your way to securing your new home in Mandurah.

Congratulations, your offer is accepted! It’s a massive moment, but don't pop the champagne just yet—you’re now entering the settlement period. This is where the real nitty-gritty happens, as all the legal and financial threads get tied up to officially transfer the property into your name.

This phase can feel a bit like a black box, with a lot of crucial work happening behind the scenes. But getting your head around the key steps will keep you in the driver's seat and ensure everything goes off without a hitch.

The most important person on your team now is your settlement agent or conveyancer. They are the pros who manage the entire legal transfer, from talking to your bank to making sure every 'i' is dotted and 't' is crossed on the contract.

The Role of Your Settlement Agent

Think of your settlement agent as the project manager of your purchase. They live and breathe the legalities of WA property transactions and will handle all the complex paperwork for you.

Here’s what they’re busy doing:

- Liaising with Financial Institutions: They'll work directly with your bank or broker to ensure the loan funds are ready to go on settlement day.

- Title Search and Checks: A crucial step. They perform a title search to confirm the seller is the legal owner and check for any nasty surprises like caveats, debts, or restrictions on the property.

- Adjusting Rates and Taxes: They meticulously calculate and adjust council and water rates, so you only pay from the day you take ownership.

- Preparing Legal Documents: They prepare the all-important Transfer of Land documents for you to sign.

- Orchestrating Settlement: They coordinate the final exchange of documents and funds between your bank and the seller's representatives on the big day.

This behind-the-scenes work is absolutely vital for a smooth handover, letting you focus on the fun stuff, like arguing over paint colours. In a fast-moving market like WA's—where Perth saw annual appreciation hit a staggering 17.2% due to tight supply—having an expert finalise your purchase efficiently is non-negotiable. You can learn more about what’s fuelling this boom and get more insights on WA's housing rebound on cotality.com.

Navigating Key Milestones

The settlement period is usually anywhere from 30 to 90 days, and a few key things need to happen along the way. The first big hurdle is getting your contract conditions sorted, especially the "subject to finance" clause. Once your lender gives you unconditional loan approval, you’re officially locked in.

The last big item on the agenda before settlement day is the pre-settlement inspection. This normally happens in the week before handover. It’s your final chance to walk through the property and make sure everything is exactly as it should be.

The final inspection is your last opportunity to ensure the property is in the same condition as when you made your offer. Don't rush this step—it’s your final check to prevent any unwelcome surprises after you move in.

Your Pre-Settlement Inspection Checklist

When you do your final inspection, you need to be thorough. The goal is simple: confirm the property is in the same condition you agreed to buy it in, and check that all the inclusions are still there and in working order.

Here’s a practical checklist to take with you:

- Test All Appliances: Turn on the oven, flick on the air conditioning, run the dishwasher, and check the hot water system.

- Check Fixtures and Fittings: Run every tap (hot and cold), flush the toilets, and test every single light switch.

- Inspect for New Damage: Look carefully for any new scuffs on walls, scratches on the floor, or cracks in windows that weren’t there before.

- Confirm Inclusions: Check that everything listed in the contract—like the curtains, specific light fittings, or that garden shed—is still in place.

- Ensure Vacant Possession: Confirm the seller has cleared out all their belongings (unless you've agreed otherwise).

If you spot an issue, call your settlement agent immediately. They can raise it with the seller’s agent and negotiate a solution before the money changes hands, ensuring you can finally get those keys without any last-minute drama.

Common Questions About Buying Property in Mandurah

Stepping into the property market can feel like you're learning a whole new language. There are so many unique terms and processes to get your head around. To cut through the noise, we've pulled together the most common questions we hear from buyers looking for a land and house for sale in Mandurah.

Here are the clear, no-nonsense answers you need to move forward with confidence.

What Are the First Steps Before Looking for a Property in Mandurah?

Before you even think about scrolling through online listings, your very first move needs to be sorting out your finances. Honestly, this is the bedrock of a smooth and successful property search.

The most critical step? Chat with a mortgage broker or your bank to get a handle on your borrowing power and, ideally, lock in a loan pre-approval. This gives you a rock-solid budget to work with, saving you the heartbreak of falling for a home that's just out of reach. It also shows sellers and agents that you’re a serious, ready-to-go buyer.

Next up, sit down and make a really clear list of what you're looking for in a property. A great way to do this is to split it into two columns: your absolute 'must-haves' and your 'nice-to-haves'.

- Must-Haves: These are your deal-breakers. Think about things like the number of bedrooms you need, a secure yard for the dog, or being in a particular school zone.

- Nice-to-Haves: These are the bonuses. The things you’d love but could compromise on, like a swimming pool, a separate theatre room, or a home office.

Getting this clarity from day one makes your search so much more focused and efficient. It saves a huge amount of time and energy.

How Is Stamp Duty Calculated in Western Australia?

Stamp duty, which is officially called transfer duty here in WA, is a state government tax that’s calculated on a sliding scale. The amount you’ll pay is based on the property's 'dutiable value'—which is almost always the purchase price. Put simply, the more the property is worth, the higher the rate of duty you'll pay.

The good news is that the WA government offers some pretty significant concessions for first-home buyers, which can slash this upfront cost.

If you're a first-home buyer, getting your head around stamp duty concessions is a must. The savings can make a massive difference to your budget, potentially freeing up thousands of dollars for furniture, moving costs, or those first few projects.

Here's a quick look at the current thresholds for first-home buyers:

| Property Type | Value for Zero Stamp Duty | Value for Concessional Rate |

|---|---|---|

| Established Home | Up to $430,000 | $430,001 – $530,000 |

| Vacant Land | Up to $300,000 | $300,001 – $400,000 |

For everyone else, the standard rates will apply. The easiest way to get a solid estimate for your specific purchase is to jump online and use a stamp duty calculator.

What Does Subject to Finance Mean?

Making an offer 'subject to finance' is an extremely common—and highly recommended—condition in a WA property contract. It basically means your offer is conditional on your bank or lender giving you the final, unconditional green light for your home loan on that specific property.

This clause always includes a timeframe, usually somewhere between 14 and 28 days, for you to get that final approval sorted. It’s a crucial safety net for you, the buyer.

If, for whatever reason, your lender pulls the pin—maybe the bank's valuation comes in lower than what you offered—this condition lets you legally walk away from the contract. Most importantly, it means you can do so without losing your deposit. It protects you from being locked into buying a property you can't actually fund.

What Should I Check During the Final Pre-Settlement Inspection?

The pre-settlement inspection is your last chance to walk through the property and make sure it’s in the same state as when you first agreed to buy it. This isn’t a time to be polite or rush through; you need to be thorough.

Your main job is to check that everything included in the contract is still there and, crucially, in good working order.

Here’s a practical checklist to run through:

- Fire Up the Systems: Turn on the air conditioning and the heating. Run the hot water for a minute to make sure it’s working.

- Test All Appliances: Switch on the oven, cooktop, rangehood, and dishwasher (if they're included) to see that they're all operational.

- Check Plumbing & Electrics: Flick every single light switch. Run every tap and have a peek under the sinks for leaks. Flush every toilet.

- Look for New Damage: Keep an eye out for any new scuffs on the walls or scratches on the floor that might have happened during the seller's move.

- Confirm the Inclusions: Grab your contract and double-check that everything listed—from the curtains to the garden shed—is still on the property.

- Make Sure It’s Empty: Check that the seller has cleared out all their belongings and rubbish from the house, garage, and yard.

If you spot any problems during this inspection, you need to tell your settlement agent straight away. They can then talk to the seller’s rep to sort it out before settlement happens, ensuring you get a smooth, stress-free handover.

Ready to start your property journey in Mandurah? Whether you're buying your first home or looking for your next investment, getting expert advice is the key to success. For a free, no-obligation appraisal or a chat about the local market, get in touch with David Beshay Real Estate at https://realestate-david-beshay.com.au.