Picture this: you've found the perfect home, but the deposit is just out of reach. What if you had a silent partner who could chip in for a big chunk of the purchase price, helping you get your foot in the door without actually moving in with you?

That’s pretty much how a shared equity scheme in WA works. It’s a partnership, usually with a government body, designed to slash the upfront cost of buying a home and get you onto the property ladder much sooner than you thought possible.

What Is a Shared Equity Scheme and How Does It Work?

At its core, a shared equity scheme is a way to co-buy a property with an equity partner. This partner—typically a government agency—contributes a percentage of the home's purchase price. In return, they hold a corresponding share in your property's future value.

Let's break it down with a real-world Mandurah example. Say you've got your eye on a home for $500,000. On your own, you might need a massive $100,000 deposit to get a loan without paying extra for Lenders Mortgage Insurance (LMI).

But with a shared equity scheme, the government might step in and contribute, say, 30% of the price ($150,000). Suddenly, you only need to get a home loan for the remaining 70% ($350,000). This drastically lowers the deposit you need to save and makes your monthly mortgage repayments much more manageable. You get to live in and own the home, while the government quietly holds its stake.

To make it even clearer, here’s a simple table.

Shared Equity at a Glance

| Component | How It Works |

|---|---|

| Your Contribution | You provide a small deposit (as low as 2%) and secure a home loan for your portion of the property value. |

| Partner's Contribution | A government body (like Keystart) contributes up to 30% of the purchase price, reducing your loan amount. |

| Ownership | You are the legal owner and live in the property. The partner has a silent, financial stake only. |

| Repayments | You make repayments only on the loan you took out, not on the partner's share. |

| Future Sale | When you sell, the partner gets their percentage back from the sale price. If the property value went up, so did their share. |

This setup is purely a financial arrangement to help you bridge the affordability gap.

The Role of Your Silent Partner

Don't worry, your government partner won't be dropping by for dinner. Their involvement is entirely financial. You are responsible for all the usual costs of homeownership—council rates, strata fees, insurance, and all the upkeep.

The "shared" part of the deal is all about the shared equity, not sharing your living space. When the time comes to sell, the partner receives their percentage of the sale price. If your home's value has grown, their share has grown with it. That’s why it’s so important to get your head around what equity is in property before jumping into one of these agreements.

Key Shared Equity Programs in WA

Here in Western Australia, there are a couple of main government-backed programs you’ll come across:

- Keystart: This is the big one. It's a long-running state government initiative created specifically to help West Aussies buy their own home with a tiny deposit and no LMI.

- Help to Buy Scheme: This is a newer federal government program rolling out across the country. It works on a similar model, aiming to make homeownership more accessible for more Australians.

These aren't just small-time programs; they have serious government backing. The Cook Labor Government, for instance, recently injected a massive $210 million into expanding Keystart. The goal? To fund 1,000 new loans for apartments and townhouses. You can read more about this major initiative to see just how committed the government is to helping people own their own homes. This shows just how vital these schemes are in WA’s current property market.

Comparing WA's Key Shared Equity Programs

When you start digging into shared equity schemes in WA, you’ll quickly find two main players on the field: the state-based Keystart program and the newer federal Help to Buy Scheme. They both aim to get you into your own home sooner, but they go about it in slightly different ways. Figuring out which one is the right fit for your situation is a crucial first step.

Keystart has been a familiar name in the WA property scene for years. It's a tried-and-tested program specifically designed by the state government to help West Aussies clear two of the biggest hurdles in homeownership: saving up a massive deposit and avoiding costly Lenders Mortgage Insurance (LMI).

Then you have the federal government's Help to Buy Scheme, which is a more recent arrival offering a different flavour of support. While both are designed to lower the upfront financial pressure on buyers, the mechanics of how they help you are distinct.

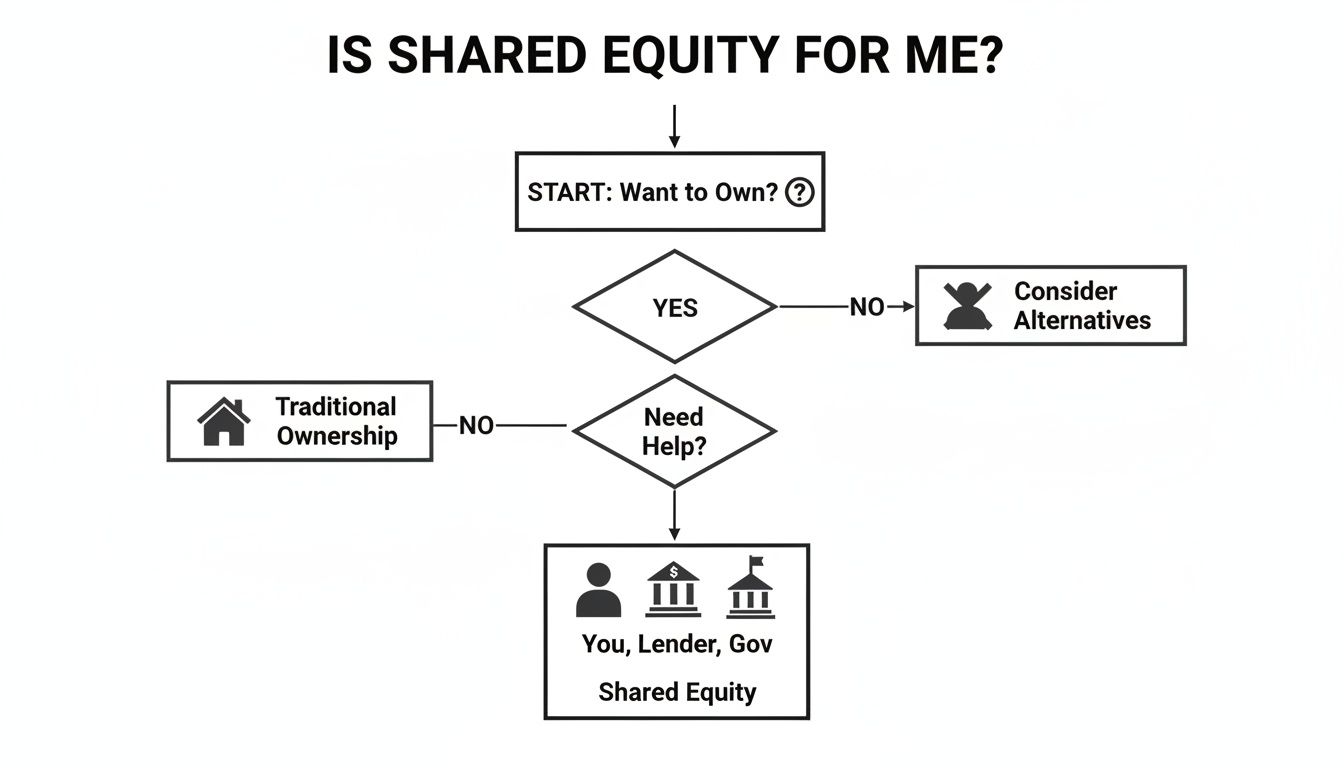

This flowchart gives you a quick visual rundown of how a shared equity arrangement works, bringing you, a lender, and a government partner together.

As you can see, if you're keen to buy but need a hand getting there, a shared equity partnership is a solid path worth exploring.

Keystart Your Journey in WA

Think of Keystart as a 'transitional lender'. Its biggest drawcard is the incredibly low deposit requirement, which can be as little as 2%. Even better, you don't have to pay any LMI, a saving that can easily run into the thousands.

Keystart isn't just a loan; it's a stepping stone. The idea is to get you into your own home now, let you build up some equity, and then eventually refinance to a traditional bank loan once your financial position is stronger.

This makes it a fantastic option for buyers who have a good, stable income but just haven't been able to sock away that huge 20% deposit.

The Federal Help to Buy Scheme

The Help to Buy Scheme works on a more classic shared equity model. Instead of giving you the whole loan, the government chips in for a slice of the property itself, taking an equity stake. This directly shrinks the size of the mortgage you need to get from a participating bank.

With the Australian Government's Help to Buy Scheme, eligible buyers can get into the market with a deposit as low as 2%. The government co-invests by contributing up to 40% for new builds or 30% for existing homes. Commonwealth Bank is one of the major lenders on board, and you can discover more about this federal initiative and its partners to see the finer details.

This approach can be especially powerful if you're looking to build, thanks to that higher equity contribution. By stacking these two programs side-by-side, you can get a clear picture of which shared equity scheme in WA aligns best with your financial situation and your property goals, whether you're eyeing an established home in Mandurah or planning a brand-new build.

Do You Qualify for a Shared Equity Scheme in WA?

So, you're interested in a shared equity scheme. The big question is: do you actually qualify? Think of it as a checklist to make sure these programs are helping the right people get a foot on the property ladder. Let's break down what you'll need to tick off.

In WA, schemes like Keystart and the federal Help to Buy Scheme look at a few key things: your income, whether you’re a resident, and if you’ve owned property before. The rules for each can be slightly different, so it's all about finding the one that fits your situation.

Generally, you'll need to be an Aussie citizen or permanent resident, be over 18, and not own any other property or land—anywhere. The goal is to help new buyers, not investors. You’ll also need to have a bit of a deposit saved up, but it can be as little as 2% of the purchase price.

Income and Property Price Caps

This is where the fine print really comes into play. Both schemes have strict income limits to ensure they're supporting low-to-middle income earners. These caps change depending on whether you're single, a couple, or a family with kids.

The real game-changer for WA buyers has been the recent massive jump in property price caps, making these schemes a realistic option in places like Mandurah where prices have been climbing.

This change has been huge for Western Australia. The property price cap for homes in Perth and regional WA shot up to $850,000—a massive leap from the old $600,000 limit. That $250,000 increase means a much wider range of homes are now within reach, which is a massive relief for buyers in a rising market.

A Practical Eligibility Checklist

Want to see if you're in the running? Here’s a quick rundown of the usual requirements:

- Citizenship: Are you an Australian Citizen or Permanent Resident?

- Age: Are you 18 or older?

- Property Ownership: Do you currently own any property or land, either here or overseas? (The answer generally needs to be no).

- Residency: Is this going to be the home you actually live in? (It has to be your main residence).

- Income Level: Is your annual income below the threshold for your household (single, couple, or family)?

- Deposit: Have you managed to save at least a 2% deposit?

If you can say yes to these, you're on the right track. Even better, these schemes can often be stacked with other government support. You might be able to combine a shared equity loan with other benefits, which you can read more about in our guide to the First Home Owner Grant in WA.

Just remember, things can change. It’s always a smart move to double-check the latest rules directly on the official Keystart and Help to Buy websites before you get too far down the road.

Understanding the Financials of a Shared Equity Home

Diving into a shared equity scheme can feel like learning a new language, but once you break it down, the numbers are much simpler than they first appear. The whole point is to shrink the size of your home loan, which in turn makes both your upfront costs and your ongoing repayments much easier to handle. For a first-home buyer, this completely changes the financial picture.

Let's walk through a real-world example right here in Mandurah to see how a shared equity scheme in WA really works. Say you've found the perfect place for $600,000.

Normally, you'd be looking at getting a loan for that full amount, minus whatever deposit you've managed to save. But with a shared equity partner like the government contributing 30% ($180,000), your side of the deal changes dramatically. All of a sudden, you only need to secure a home loan for the remaining 70%, which is $420,000.

That reduction is the key. A smaller loan means you need a smaller deposit, and your monthly mortgage repayments will be significantly lower. It's a game-changer.

How Your Loan and Repayments Work

Your home loan is based only on your share of the property. You're not borrowing the government's portion, so you don't pay a cent of interest on it. This has a massive positive knock-on effect on your Loan to Value Ratio (LVR), a number that lenders look at very closely.

A lower LVR often means you can dodge paying thousands in costly Lenders Mortgage Insurance (LMI) and you might even snag a better interest rate from the bank. Getting your head around this is vital, and you can learn more about the importance of what a Loan to Value Ratio is in our detailed guide.

The most powerful aspect of shared equity is that you only make repayments on the money you've borrowed. The government's contribution sits silently in the background, with no monthly payments due on their share.

This structure is specifically designed to take the financial pressure off homeowners in those crucial early years, giving you the breathing room to build financial stability.

To see the difference in black and white, let's compare the two scenarios using our $600,000 home example.

Shared Equity vs Traditional Loan (Example for a $600,000 Home)

| Financial Aspect | Traditional 20% Deposit Loan | Shared Equity (30% Government Share) |

|---|---|---|

| Purchase Price | $600,000 | $600,000 |

| Buyer's Share | 100% ($600,000) | 70% ($420,000) |

| Govt. Equity Share | N/A | 30% ($180,000) |

| Buyer's Loan Amount | $480,000 (assuming 20% deposit of $120k) | $408,000 (assuming 2% deposit of $12k) |

| Monthly Repayments | Higher (based on a larger loan) | Significantly Lower (based on a smaller loan) |

| LMI Payable | No (with 20% deposit) | Potentially avoided or reduced |

As you can see, the shared equity pathway dramatically lowers the amount you need to borrow and, consequently, your monthly outgoing costs, making homeownership far more attainable.

Paying Back the Government's Share

Of course, the government's share does eventually need to be repaid. This typically happens in one of two ways:

- When you sell the property: The government gets its percentage back from the final sale price. If your home's value has gone up, their share has grown with it—just like yours.

- Through voluntary repayments: Most schemes encourage you to start buying back the government's equity over time. You can usually make lump-sum payments, often in chunks of 5% or more, based on the property's current market value at the time.

This flexibility is great because it lets you gradually work your way towards 100% homeownership as your financial situation gets stronger, until you've fully transitioned to a traditional mortgage.

Weighing Up the Pros and Cons of Shared Equity

A shared equity scheme can feel like a complete game-changer, but it's a serious financial commitment. You've got to go in with your eyes wide open, looking at both the good and the not-so-good. This isn't just about getting onto the property ladder right now; it's about making sure the climb is right for your long-term goals.

On one side, the benefits are real and they kick in straight away. On the other, you're entering a long-term partnership that has its own set of rules. Let's break it down so you can weigh it up properly.

The Major Upsides of Shared Equity

For most people in WA, the biggest win is simply getting into the market, period. A shared equity scheme can slash the time you'd otherwise spend saving, turning a distant dream into a near-term reality.

- Lower Upfront Costs: Forget scraping together a massive 20% deposit. With schemes like Keystart, you could get in with as little as 2%, and you won't get stung with Lenders Mortgage Insurance (LMI). That alone can save you tens of thousands of dollars right out of the gate.

- Less Mortgage Stress: Because the government is covering a chunk of the purchase price, your home loan is smaller. This means your monthly repayments are lower, which frees up cash and takes a huge amount of financial pressure off, especially in those first few years.

- More Properties to Choose From: When you don't need a huge deposit and your borrowing power gets a boost, suddenly more doors open. This is a big deal in competitive areas like Mandurah, where it can give you the edge you need to secure a great home.

At its core, a shared equity scheme completely changes the affordability conversation. It’s not just about buying a home; it's about buying one without stretching your budget to its absolute limit, making homeownership a much more sustainable reality.

That bit of financial breathing room is often the single most valuable advantage for first-home buyers.

The Potential Downsides to Keep in Mind

As great as the benefits are, you have to remember the "shared" part of the deal. This partnership applies to everything – including the profits.

The biggest thing to get your head around is the shared capital growth. When your property goes up in value, so does the government's share. If you sell down the track, they get their percentage of the current market value, not just the money they originally put in. This means you'll be handing over a portion of your profits.

On top of that, things like selling or renovating can get a bit more complicated. You’ll need to follow the specific steps laid out in your agreement, which might mean getting official valuations or seeking approval before you start knocking down walls.

Finally, remember this is a long-term arrangement. You're linked to the scheme until you either sell the property or manage to buy out the government's share entirely, which takes some serious financial planning. A smart decision means balancing the immediate relief these schemes offer against these important future considerations.

Your Step-by-Step Application Guide

Ready to take the next step with a shared equity scheme in WA? The application process can look a bit intimidating from the outside, but once you break it down into simple, manageable tasks, it's actually quite straightforward. This is your roadmap to getting started on your homeownership journey.

First things first, let's do a thorough financial health check. Before you even think about looking at properties on realestate.com.au, you need a crystal-clear picture of your income, expenses, and savings. This isn't just box-ticking; it's the foundation for figuring out your borrowing power and overall readiness.

Preparing Your Documentation

Once you've got a handle on your financial position, it's time to gather your paperwork. Both the lender and the scheme provider will need to see detailed evidence to confirm you meet the criteria. Getting organised now will save you a world of headaches later on.

Typically, you'll need to pull together:

- Proof of Income: Recent payslips, your employment contract, or the last couple of tax returns.

- Identification: Your driver’s licence, passport, and Medicare card will usually do the trick.

- Bank Statements: A few months' worth of statements for all your accounts. They want to see your savings history and spending habits.

- Liability Details: Information on any other debts you have, like a car loan or credit card balances.

Tip: Make your life easier by creating a dedicated folder on your computer for these documents. Scan everything and have it ready to go – it makes the submission process so much smoother.

Finding Your Support Team and Property

With your finances sorted, the next phase is about getting the right professionals on your side and kicking off the property hunt. This is where having expert guidance is priceless, especially for a specialised product like a shared equity scheme in WA.

-

Engage a Mortgage Broker: Find a broker who has experience with Keystart and other government schemes. They know the ins and outs of the specific lender requirements and can help you get that all-important pre-approval, which shows sellers you're a serious buyer.

-

Partner with a Local Real Estate Agent: An agent who lives and breathes the Mandurah market is your best asset. They can pinpoint properties that fit the scheme's price caps and other criteria, and their local knowledge is crucial for making a smart buy.

-

Find an Eligible Property: With pre-approval in hand, you can start your property search with real confidence. Just make sure any home you fall in love with is within the scheme's price limits for the Mandurah area.

From there, once you find the one, you'll move through the formal loan application, property valuation, and settlement. Your broker and agent will be there to guide you all the way to the finish line.

Your Questions About WA Shared Equity, Answered

Even after you've wrapped your head around the basics, it's completely normal to have a few lingering questions. A shared equity agreement is a long-term financial partnership, so getting clarity on the finer details isn't just smart—it's essential.

Let's walk through some of the most common questions that pop up once people start picturing the day-to-day realities of owning a home this way. Knowing the rules around renovations, what happens in a down market, and the path to full ownership is key.

Can I Renovate a Shared Equity Property?

Yes, absolutely. This is your home, and you can definitely make improvements. The crucial thing to understand is how this impacts your agreement. In short, the value you add through your own hard work and investment is yours to keep. The government doesn't get a cut of your renovation profits.

How it works is that the government's share is typically calculated on the property's value before your upgrades. To make this work, you'll need to keep meticulous records of all your costs and likely get a formal valuation before and after the renovation. Just be sure to check the specific terms of your agreement before you start knocking down any walls.

The bottom line is this: while you share the natural capital growth with your equity partner, the value you personally create through renovations is 100% yours. This ensures you're the one who benefits from improving your home.

What Happens If My Property Value Goes Down?

This is a very common worry, but one of the core ideas of shared equity is shared risk. If your property's value drops, the government shares that loss with you in exactly the same way it would have shared in a gain. It truly is a two-way street.

When you eventually decide to sell, the government's payout will be based on its percentage share of the current, lower market price. This means they would get back less than their initial contribution, which shields you from carrying the entire financial burden of a market downturn.

How Do I Buy Out the Government's Share?

The whole point of these schemes is to help you get to full homeownership. You can buy out the government's share over time in a process sometimes called "staircasing." This is usually done in chunks, like making lump-sum payments of 5% or more at a time.

These buy-outs are based on the property's current market value, which means you'll need a fresh valuation each time you decide to purchase another slice of equity. As their financial situation improves, many homeowners eventually refinance their original mortgage to cover these payments. You can gradually increase your ownership stake this way until you transition to a standard mortgage and own the home outright.

Navigating the ins and outs of a shared equity scheme in the Mandurah area can feel a bit complex, but you don't have to figure it all out on your own. For expert advice that's tailored to our local market, get in touch with David Beshay Real Estate. Let's explore your path to getting the keys to your own home.

https://realestate-david-beshay.com.au